The Executive's Guide to the Utah-Chartered Industrial Bank

Brian's Banking Blog

A Utah-chartered industrial bank—also known as an Industrial Loan Company (ILC)—is a state-chartered financial institution with a defining feature: it can be owned by a commercial, non-financial parent company. While these FDIC-insured banks operate almost identically to traditional banks, they possess a critical strategic advantage: the parent company is not subject to consolidated supervision by the Federal Reserve.

Understanding the Industrial Bank Charter

For bank executives and directors, understanding the Utah-chartered industrial bank is not an academic exercise; it is a competitive necessity. This charter serves as a purpose-built vehicle for major commercial firms—from automotive manufacturers to technology conglomerates—to integrate banking services directly into their core operations. The primary advantage is clear: the parent company avoids becoming a Bank Holding Company (BHC), affording it an operational freedom that traditional banking groups cannot match.

This exemption is the central value proposition. While the ILC subsidiary must adhere to the same stringent safety and soundness regulations as any other bank—overseen by both the FDIC and the Utah Department of Financial Institutions (DFI)—its non-bank parent is free to operate without the activity restrictions imposed on BHCs.

A Blueprint for Integrated Financial Services

The ILC model is a deliberate charter designed for seamless business integration, not a regulatory loophole. Consider a national retailer establishing an ILC. It can now offer point-of-sale financing for high-value consumer goods. If it originates 100,000 such loans annually at an average of $4,500 each, it has constructed a $450 million loan portfolio directly from its existing customer traffic.

This strategy enables the company to control the entire customer journey, drive incremental sales, and create a new, high-margin revenue stream from net interest income.

With this structure, a company can:

- Offer Consumer and Commercial Loans: Finance its customers' purchases or extend capital to business partners within its supply chain.

- Accept FDIC-Insured Deposits: Build a stable, low-cost funding base to support its lending activities.

- Issue Credit Cards: Launch branded cards to enhance customer loyalty and generate interchange fee revenue.

Key Takeaway for Bank Executives: An ILC is not merely another local competitor. It is a rival operating with a fundamentally different cost structure, customer acquisition model, and regulatory framework. Data intelligence is essential to accurately assess this competitive threat.

Why Utah is the ILC Hub

Utah is the undisputed center for the ILC charter due to its established and stable regulatory environment. In 2019, Utah-based industrial banks held $140.6 billion in assets, representing a commanding 93.5% of all industrial bank assets nationwide.

This concentration accelerated after the 1987 Competitive Equality Banking Act (CEBA) solidified the BHC exemption that makes the charter strategically compelling. You can learn more about the scale of Utah's industrial banking sector and its history.

For bank directors, monitoring these institutions is critical. Their unique structure can obscure a clear assessment of risk and performance through traditional analysis. To understand the competitive landscape, executives need unified data intelligence that can penetrate the corporate structure and evaluate the true financial health and strategic objectives of these powerful entities.

Navigating the Dual-Oversight Regulatory Framework

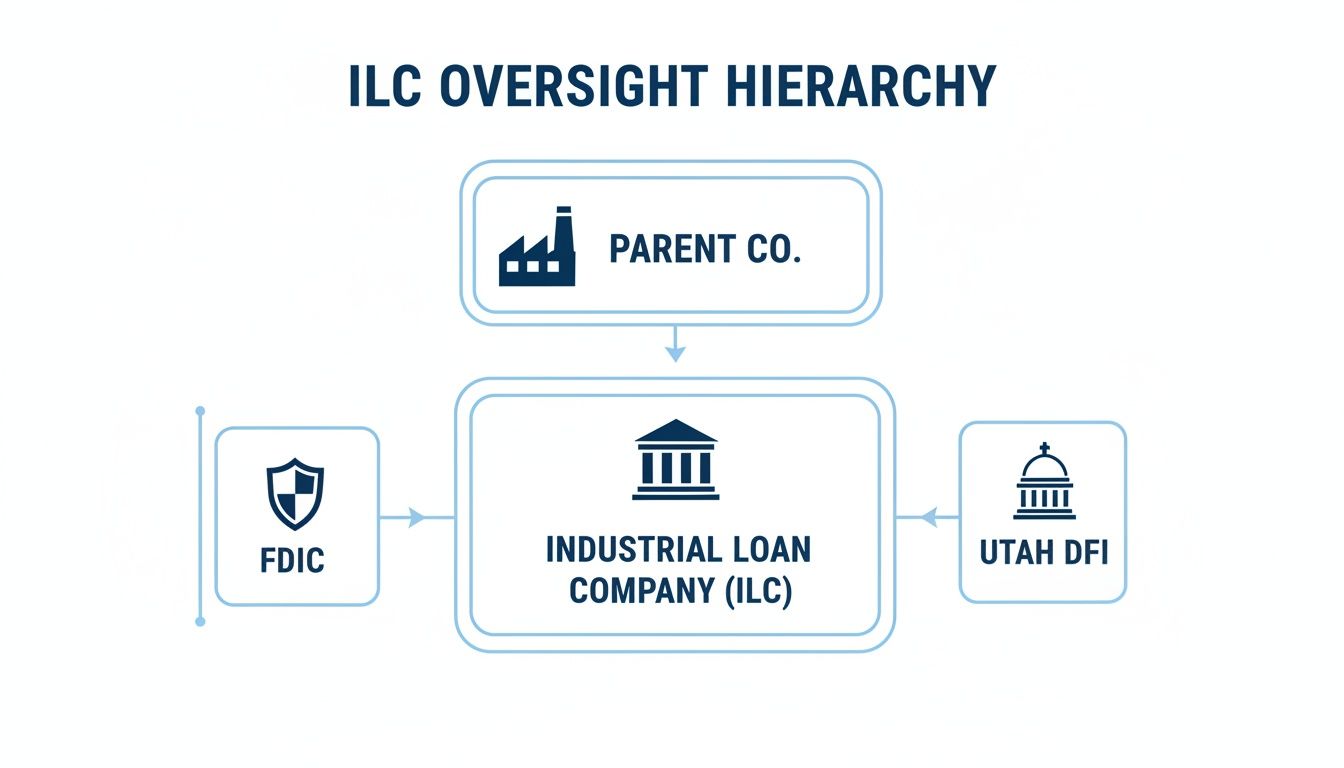

To effectively compete with or serve a Utah-chartered industrial bank, executives must first understand its distinct regulatory structure. These banks operate under a dual-oversight model, reporting to both state and federal authorities, but with a critical omission that provides their strategic advantage.

The Utah Department of Financial Institutions (DFI) serves as the primary chartering authority and state regulator, ensuring the bank adheres to Utah's laws and maintains operational soundness.

Simultaneously, because these banks hold federal deposit insurance, the Federal Deposit Insurance Corporation (FDIC) acts as the primary federal regulator. The FDIC conducts regular safety and soundness examinations to protect its Deposit Insurance Fund.

The Federal Reserve: A Conspicuous Absence

The defining feature of this structure is not who is present, but who is absent. The parent company of an industrial bank is not subject to consolidated supervision by the Federal Reserve. This exemption from the Bank Holding Company Act is the core of the ILC model, permitting a commercial enterprise to own an insured depository institution without being limited to activities "closely related to banking."

This creates a significant analytical challenge for traditional bank executives. Standard signals from the Fed—such as enforcement actions or capital plan reviews at the parent company level—are unavailable for assessing the consolidated entity's risk appetite or financial condition. This regulatory distinction requires a direct, data-driven analysis of the bank subsidiary, whether you are evaluating a competitor like PayPal Bank or a potential partner like Toyota Financial Savings Bank.

You can learn more about the specific roles of different regulatory agencies for banks in our detailed guide.

Practical Implications for the Marketplace

This unique structure has tangible consequences that shape the competitive landscape. For example, any Utah-chartered industrial bank with assets exceeding $100 million is statutorily prohibited from offering traditional demand deposit accounts (i.e., checking accounts).

Instead, they must utilize Negotiable Order of Withdrawal (NOW) accounts. While the end-user experience is similar, this is a critical operational distinction. A fintech ILC must engineer its small business deposit products as NOW accounts, a subtle but meaningful difference in product design and treasury management.

Key Takeaway for Bank Executives: A competitor's regulatory structure directly informs its business model and risk profile. Without Fed oversight of the parent, monitoring the ILC's FDIC and Utah DFI filings becomes paramount for understanding its true performance and stability. Actionable intelligence platforms like Visbanking transform raw regulatory filings into a clear competitive advantage.

Ultimately, this dual-oversight system—without the Fed—means that publicly available data from the FDIC and other regulatory bodies is the primary tool for analysis. To make incisive, informed decisions, your team must have the capability to benchmark performance, track asset quality, and monitor capital adequacy using unified regulatory data.

Dominant Business Models and Modern Applications

For bank executives, understanding the theory behind Utah-chartered industrial banks is only valuable when translated into real-world competitive intelligence. ILCs function as purpose-built vehicles designed to integrate financial services directly into large-scale commercial operations, creating a powerful synergy that is difficult for traditional banks to replicate.

The strategy is direct: a parent company with a substantial, captive customer base leverages its ILC to offer loans, accept deposits, and process payments. This model drastically reduces customer acquisition costs, converts cost centers into profit centers, and deepens customer loyalty.

This diagram illustrates the regulatory structure. The FDIC and the Utah DFI supervise the bank itself, while the parent company operates without direct oversight from the Federal Reserve.

The key takeaway is strategic freedom. The parent company can innovate and embed financial products into its core business without the typical constraints of a Bank Holding Company.

Automotive Finance Integration

The automotive industry provides a classic example. A global vehicle manufacturer can establish an industrial bank to finance its own product sales. This allows them to capture the entire customer value chain, from manufacturing to financing.

To quantify this, imagine an automaker's ILC originates 200,000 new auto loans in a single year. With an average loan size of $30,000, that represents a $6 billion loan portfolio generated annually from its existing sales channels. This interest income flows directly to the parent, ensures a consistent source of financing for its vehicles, smooths sales cycles, and builds a direct financial relationship with the end customer.

Fintech and Embedded Banking

The fintech sector is another arena where the ILC model is a transformative force. A company like Square can use a Utah-chartered industrial bank to embed FDIC-insured banking services directly into its payment platform, which is already used by millions of small businesses. With its own ILC charter, it can offer business loans and savings accounts directly, disintermediating the partner banks it previously relied upon.

Key Takeaway for Bank Executives: This is more than adding a feature; it is about owning the entire financial stack. This enhances margins and provides invaluable data on merchant cash flow—data that can be used to underwrite loans with a precision that traditional lenders find difficult to match.

The primary threat to community and regional banks stems from this data advantage. These tech-first ILCs compete not just on rates but on data-driven product design and a seamless user experience. You can see the diversity of industries leveraging this charter by exploring this complete list of every Utah industrial bank.

Turning Intelligence into Action

It is insufficient to simply acknowledge these specialized competitors; they must be analyzed with a data-centric approach. Since there is no Federal Reserve oversight at the parent level, publicly available regulatory filings are the primary source of intelligence.

A robust bank intelligence platform is essential for this task. It allows executives to:

- Benchmark Performance: How does an ILC's asset growth, profitability, or efficiency compare to your own institution? Conduct direct, apples-to-apples comparisons.

- Analyze Portfolio Composition: Deconstruct their loan and deposit books to understand their strategic focus and risk appetite.

- Identify Strategic Shifts: Monitor financial data over time to detect competitive threats or emerging market trends before they become critical.

With a data-driven strategy, these opaque competitors become addressable challenges. This intelligence provides the foundation to defend market share, identify potential partnerships, and execute strategic initiatives with confidence.

The Economic Impact of Utah's Banking Sector

Viewing Utah-chartered industrial banks as a mere regulatory anomaly is a strategic error. These institutions constitute a concentrated economic engine with national reach. For bank executives, dismissing this sector as a regional phenomenon means ignoring a significant competitive force. The capital, employment, and economic output originating from these banks command attention in major financial markets.

Quantifying the Economic Contribution

The economic impact of Utah's industrial banks extends far beyond state lines, funding innovation nationwide while generating significant local employment, GDP growth, and tax revenue.

A 2020 analysis by the Gardner Policy Institute quantified the impact for 2019 alone. These banks accounted for:

- 6,468 direct and indirect jobs within Utah.

- $443.8 million in worker earnings.

- $722 million in Utah's GDP, representing 0.4% of the state's entire economy.

- $32 million in state and local tax revenue.

The model has also demonstrated stability. When the parent company Conseco filed for bankruptcy in 2002, its profitable Utah ILC was sold to GE Capital at book value with no loss to the FDIC, a testament to the structure's resilience. These are not abstract statistics; they represent a deeply integrated financial ecosystem.

Key Takeaway for Bank Executives: This economic strength means you are competing against well-funded, deeply entrenched opponents. If evaluating a partnership, you are dealing with a major player possessing significant resources and market influence.

The scale of this contribution is best understood through data.

Utah Industrial Bank Economic Contribution (2019 Data)

| Metric | Value (USD) | Context |

|---|---|---|

| Total Jobs Supported | 6,468 (direct & indirect) | Represents significant employment in a specialized financial sector. |

| Total Worker Earnings | $443,800,000 | Highlights the high-value nature of the jobs created. |

| GDP Contribution | $722,000,000 | Equivalent to 0.4% of Utah's entire state GDP. |

| State & Local Tax Revenue | $32,000,000 | Direct fiscal benefit supporting public services and infrastructure. |

This data confirms the sector is a core pillar of the state's economy.

A Hub for Specialized Financial Talent

The concentration of industrial banks has made Utah a magnet for specialized talent. The state possesses a deep pool of professionals with expertise in the ILC model, from operations and regulation to compliance. This human capital creates a competitive advantage that is difficult to replicate, fostering a feedback loop of innovation and efficiency as best practices are shared across the sector.

Translating Economic Data into Strategy

For bank executives and relationship managers, this economic analysis is a map of threats and opportunities. The $722 million in GDP represents a network of businesses, vendors, and high-net-worth individuals connected to these powerful banks.

The next step is to use data intelligence to act on this reality. By analyzing performance metrics, asset mix, and growth trends, your team can become tactical.

- Identify Key Decision-Makers: Pinpoint the executives at both the Utah bank and its parent company who control strategy and capital allocation.

- Target the Ecosystem: Identify opportunities to offer treasury management, wealth services, or commercial loans to the network of companies that support the ILC sector.

- Benchmark Strategically: Measure your institution against these highly focused competitors to identify vulnerabilities and defend your market position.

The economic scale of Utah's ILC sector is undeniable. The critical question for your leadership team is how you will leverage precise, unified data to convert this market reality into strategic relationships and new business. Explore Visbanking to see how our intelligence platform can help you benchmark your institution and identify opportunities in this dynamic market.

A History of Growth and Adaptation

To understand the strategic durability of Utah's industrial banks, one must look to their history. The modern ILC was shaped by deliberate policy decisions in Washington D.C. and, critically, in Utah. This history is essential for anticipating future regulatory shifts and competitive threats.

The pivotal moment was the Competitive Equality Banking Act (CEBA) of 1987. This legislation created the specific exemption that allows an ILC's parent to avoid classification as a Bank Holding Company, thereby escaping supervision by the Federal Reserve. This single provision laid the groundwork for the modern ILC.

At the state level, the floodgates opened in 1997 when Utah lifted its moratorium on new ILC charters, signaling to commercial firms nationwide that the state was open for business.

From Niche Lenders to Financial Powerhouses

The subsequent growth was explosive. Before CEBA, Utah had only 11 ILCs, primarily small consumer lenders with average assets below $45 million. By 2006, following Utah's policy change, the state was home to 32 of the 62 ILCs in the country, controlling nearly 90% of the industry’s assets.

The sector’s total assets grew from $3 billion in 1987 to over $102 billion by 2011. By 2019, Utah’s ILCs held $140.6 billion in assets—93.5% of all industrial bank assets in the U.S. You can examine this growth story further at the Utah Department of Financial Institutions.

This expansion attracted major corporations and sparked intense debate, most notably Walmart's 2005 application for an ILC to process card payments. The fierce opposition from traditional banks ultimately led Walmart to withdraw its application, but the event solidified the ILC charter as a serious strategic option for America's largest companies.

The Next Wave: Fintech Integration

The long-standing debate over the separation of banking and commerce has shifted to a new arena. Today, the dominant trend is the influx of fintech companies seeking ILC charters. Firms like Square (now Block) and Nelnet have secured charters to embed FDIC-insured banking services directly into their technology platforms.

Key Takeaway for Bank Executives: This history is a direct indicator of future competition. The same regulatory framework that enabled industrial giants to enter banking is now being leveraged by technology companies armed with vast user bases and proprietary data.

This demonstrates that the ILC charter is not a historical artifact but a flexible tool that adapts to evolving business models. As more technology players pursue this path, the competitive pressure on the traditional banking perimeter will intensify.

For leadership teams, the lesson is clear. Understanding this history is about strategic foresight. By tracking the performance of these institutions over time, from their origins to the current fintech era, you can develop a strategy that anticipates what is next. A robust bank intelligence platform is indispensable for monitoring these shifts, benchmarking your institution, and preparing to compete in a rapidly changing market.

Formulating a Competitive and Collaborative Strategy

Understanding the Utah-chartered industrial bank is the first step. The decisive phase is converting that knowledge into an actionable plan. Whether you choose to compete directly or seek collaborative opportunities, your response must be data-driven and aligned with your institution's strategic objectives.

For business development teams, this requires a forensic approach. Analyzing an ILC’s portfolio through UCC filings and loan data reveals its areas of strength and, more importantly, can expose adjacent sectors it may be neglecting. This analysis can uncover opportunities for partnership, such as offering treasury management to the parent company or specialized credit products to its extensive supplier network.

Defending Market Share Through Data Intelligence

For relationship managers and market presidents, the focus is often defensive. The primary threat from an ILC is its highly focused and efficient business model. To maintain market share, you must surgically benchmark your institution's performance against theirs.

For example, a fintech-owned ILC may operate with a net interest margin (NIM) of 4.25% and an efficiency ratio of 45% due to its technology stack and low overhead. If your community bank operates at a 3.50% NIM and a 62% efficiency ratio, this data provides a clear directive. It signals the need to defend your deposit base by emphasizing personal service and community reinvestment—qualities that quantitative metrics do not fully capture.

Key Takeaway for Bank Executives: Data illuminates the competitive landscape. It reveals an ILC's strengths, exposes your own vulnerabilities, and provides the objective facts needed to build a defensive strategy centered on your bank's unique value proposition.

Actionable Intelligence for Credit Unions

Credit union leaders face a similar challenge but can leverage a distinct narrative. Competing with a commercial giant on scale is not a winning strategy. Instead, emphasize your unique structure. The member-owned, community-focused model is a significant competitive advantage.

Use performance data to demonstrate how your institution delivers value directly to members through lower fees and superior rates. Contrast this with the profit-maximization mandate of an ILC’s corporate parent. This is a powerful and defensible narrative.

Ultimately, whether you are a commercial bank, a credit union, or another financial services provider, data fuels execution. A superior intelligence platform transforms regulatory filings and market noise into a strategic weapon. It enables your team to act decisively, whether that means identifying a key executive at a parent company, winning a client from an underserved niche, or forging a strategic alliance. You can explore more about Industrial Loan Charters to deepen your understanding of this unique market segment.

To effectively compete and collaborate, you must measure your institution against these specialized players. See how Visbanking’s data intelligence can provide your team the confidence to execute the right moves.

Frequently Asked Questions for Bank Executives

For bank executives and directors, a clear understanding of the Utah-chartered industrial bank model is essential for strategic planning. The following are direct answers to the most common questions.

What is the primary difference between an ILC and a traditional bank?

The difference lies in ownership structure and parent company oversight.

A Utah ILC can be owned by a non-financial, commercial entity—such as a retailer or technology firm—without that parent being designated a Bank Holding Company (BHC). This is significant because it exempts the parent company from direct supervision by the Federal Reserve.

The ILC subsidiary itself is fully regulated for safety and soundness by both the FDIC and the Utah Department of Financial Institutions. However, its parent can continue its commercial activities, which are generally prohibited for traditional BHCs. If you own a conventional bank, your parent entity is a BHC and is subject to the Federal Reserve's comprehensive rules.

Are deposits in an industrial bank safe?

Yes, absolutely. From a depositor's standpoint, there is no difference.

Deposits at a Utah-chartered industrial bank are insured by the FDIC up to the standard maximum of $250,000 per depositor, per institution, for each account ownership category. This is the identical coverage provided by any other FDIC-insured bank. ILCs are subject to the same rigorous examinations, capital requirements, and consumer protection regulations. The structural difference is at the parent company level, not at the depository institution itself.

Why is the Utah ILC charter attractive to fintech companies?

The Utah ILC charter offers an optimal balance for established fintech firms.

The primary attraction is avoiding BHC status for the parent company. This allows a fintech to continue its core technology and commercial operations without the Federal Reserve's activity restrictions. For a company like PayPal, an ILC charter enables a direct-to-customer model for offering small business loans and savings accounts, moving beyond reliance on partner banks. This enhances operational efficiency and allows them to own the entire customer relationship.

Key Takeaway for Bank Executives: The ILC charter provides a direct path to offering FDIC-insured products and accessing federal payment systems without requiring a complete restructuring of the parent company or divestiture of its non-banking businesses.

This makes the ILC a more efficient and less disruptive route for a technology-first company to integrate banking services directly into its platform. They can leverage their vast customer datasets and existing technology to underwrite and offer financial products with a significant cost advantage over traditional banks.

Knowing your competition is one thing. Outmaneuvering them is another. With Visbanking, you can stop guessing and start acting on hard data. Benchmark your bank against any Utah-chartered industrial bank, dissect their loan portfolios, and even identify the key executives calling the shots. See how our bank intelligence platform gives you the edge you need to compete—and win.

Related Articles

Visbanking Blog

Major Banks in US by Asset Size

Visbanking Blog

Top Banks in Utah | Updated Quarterly

Visbanking Blog

List of Banks by Asset Size

Visbanking Blog

List of Banks in Arizona

Visbanking Blog

Unlocking Growth: A Comprehensive Guide to US Banks Contacts

Visbanking Blog