How to Sell Merchant Services: A Data-Driven Playbook for Bank Growth

Brian's Banking Blog

Selling merchant services is no longer a relationship game; it has evolved into a discipline of data-driven strategy. Winning in this market requires a precise methodology: pinpointing high-value opportunities, crafting solutions that solve specific business problems, and demonstrating a clear financial upside.

Top-performing institutions have moved past the old playbook. They leverage market intelligence to identify the most profitable prospects before initiating contact, turning a volume game into a surgical strike.

The Mandate for Data-Driven Merchant Sales

The approach to selling merchant services has fundamentally shifted. Gut feelings and a firm handshake have been replaced by a precise methodology that uncovers prime opportunities before competitors are even aware they exist. For bank executives, this is not a trend; it is a modern imperative for driving crucial non-interest income.

A Market Poised for Growth

The global merchant services market is expanding rapidly. Valued at USD 66.71 billion in 2025, it is projected to reach USD 201.41 billion by 2032, reflecting a compound annual growth rate of 17.1%.

North America commands a 29% market share, making it prime territory for U.S. banks to secure a significant portion of this growth.

This is a clear directive. Banks adhering to outdated, unsystematic sales processes will be left behind. The baseline for competition is no longer just a good product; it is the intelligence used to deploy it. This reinforces a core truth: the intrinsic value of customer data is worth far more than any physical equipment.

Data intelligence is the difference between asking, "Can we offer you a better rate?" and stating, "Based on your recent equipment financing, we’ve identified a payment processing solution that can reduce your transaction costs by 18%."

From Reaction to Proactive Strategy

Shifting to a data-driven framework means moving from reacting to customer inquiries to proactively anticipating their needs. This different mindset is built on core pillars that deliver measurable results.

The following table contrasts the traditional model with a modern, data-driven approach.

The Data-Driven Merchant Sales Framework

| Pillar | Traditional Approach (Relationship-Based) | Modern Approach (Data-Driven) |

|---|---|---|

| Prospecting | Cold calling, networking, waiting for referrals. | Using signals like SBA loans and UCC filings to find businesses actively seeking capital. |

| Value Proposition | Generic pitch focused on "better rates" and service. | Customized business case based on industry, transaction volume, and operational needs. |

| Execution | Measured by call volume and new accounts opened. | Measured by portfolio profitability, client retention, and cross-sell opportunities. |

This modern approach is a practical strategy that yields deeper client relationships and a healthier bottom line.

To execute this strategic shift, the right tools are non-negotiable. Platforms that synthesize financial, regulatory, and market data are essential for transforming raw information into actionable insights.

For a deeper dive into this concept, review our guide on what business intelligence analytics means for banking. By leveraging this power, your institution can build a modern sales engine equipped for today’s market.

Pinpointing High-Value Prospects with Precision

Effective sales begin long before the first call. The foundational work lies in identifying the right merchants—those who are growing, need your offering, and represent profitable partners. Casting a wide, generic net is inefficient. Winning requires a laser-focused, data-driven approach.

This means shifting from outdated lead lists to surgical precision, using specific data signals to define an ideal market segment and pinpoint businesses in a growth phase. Generic outreach is a misallocation of resources; a targeted strategy delivers qualified leads prepared for a substantive conversation.

Spotting the Right Growth Signals

Instead of relying on intuition, top-performing bankers look for specific triggers that indicate a company is ready for change. These are not gut feelings; they are hard data points derived from publicly available financial information.

Key signals include:

- SBA 7(a) and 504 Loan Data: A business securing an SBA loan for new equipment or inventory is a prime indicator. They have fresh capital and are anticipating a sales increase, necessitating a payment system that can scale with their growth.

- UCC Filings: A new Uniform Commercial Code filing for equipment financing or a line of credit is a major tell. It signifies investment in future capacity and a likely need to upgrade their financial technology stack—an ideal time to introduce an integrated payment solution.

- Peer Bank Performance: Monitor your competitors. If a rival's deposit growth is flat in a booming commercial sector, their clients may be underserved and receptive to a new banking partner.

Using these signals transforms the nature of the conversation. It is no longer a cold call but a strategic, well-timed discussion about their specific growth plans.

A data-savvy bank can identify a client’s need for a new POS system the moment their SBA loan is approved. A competitor relying on traditional methods may not discover this opportunity for months—long after the deal is closed.

Putting Data-Driven Prospecting into Practice

Consider a real-world example. A regional bank aimed to expand its merchant services portfolio by targeting mid-market commercial clients. Their hypothesis: businesses with $5 million to $20 million in annual revenue using a non-bank fintech for payment processing were underserved. These companies are large enough to require treasury management but often begin with a simpler fintech solution for convenience.

Using a prospecting tool like Visbanking, the bank's team filtered their local market for businesses matching this exact profile. The platform cross-referenced revenue data with signals indicating relationships with standalone payment processors.

The result was a list of 75 high-propensity targets. Instead of a generic pitch, their relationship managers presented a powerful value proposition: "Let us integrate your payment processing with a full suite of treasury services to simplify your entire financial operations."

The outcome was a 20% conversion rate from that targeted list in two quarters, far surpassing previous campaign results. This demonstrates the power of a data-informed strategy. For any bank leader seeking similar outcomes, understanding modern lead generation for banks is non-negotiable.

Focusing efforts on the right segments eliminates time wasted on low-yield leads and facilitates meaningful conversations with high-value prospects. The next step is to convert this sharp targeting into a compelling offer.

Crafting Value Propositions That Compel Action

Once a high-potential prospect is identified, a generic sales pitch is ineffective. The modern market demands a solid business case, not a brochure.

To win in merchant services, you must translate prospect data into a compelling value proposition that directly addresses their operational and financial challenges.

A conversation that begins with interchange rates is a losing proposition. It commoditizes your offering and initiates a race to the bottom on price. The superior strategy is to lead with a solution to a business problem you have already identified. This elevates your role from vendor to strategic partner.

Building a Quantifiable Business Case

Data is not just for lead generation; it is for constructing an undeniable argument for change. By analyzing a prospect’s industry, estimated transaction volume, and recent growth signals, you can build a case that captures a CEO’s attention because it is grounded in their reality and focused on their bottom line.

For example: you identify a restaurant group that recently secured financing for a new location. You also know their industry faces high chargeback rates.

- The generic pitch: "We can offer you a more competitive processing rate."

- The data-driven value proposition: "Congratulations on your expansion. We understand that for restaurant groups, chargebacks can erode 10-15% of net profit. Our payment gateway features advanced fraud detection that has reduced chargeback volume by 30% for clients in your sector. For your business, this could translate to an additional $45,000 in annual profit."

The second pitch immediately shifts the conversation from a minor rate cut to significant operational savings. It demonstrates thorough preparation and presents a clear, quantifiable ROI.

Articulating the Integrated Banking Advantage

Community and regional banks possess a strategic advantage that standalone fintechs cannot replicate: a seamless financial ecosystem. Fintechs offer a product; you offer an integrated partnership.

A merchant services sale should not be a standalone transaction. It is the critical entry point for deepening the entire commercial banking relationship, creating a stickiness that insulates clients from competitor poaching.

The conversation must center on the unique benefits of integrating merchant services with business checking, treasury management, and loans. You are selling efficiency and a consolidated view of their finances. Understanding related products, such as a What Is Merchant Cash Advance, can further position your bank as the comprehensive financial partner they require.

Tying It All to Market Realities

Promoting value-added services is a market necessity. The merchant services landscape is defined by regional dominance and transaction volumes. North America generates 30-40% of global payment processor revenues, estimated between $19 billion and $45 billion in 2025.

However, while global digital payments are projected to reach $157 trillion in transaction value that year, core processor revenues will be closer to $64 billion. This gap reveals a critical insight: the real profit lies not in the transaction itself, but in the services surrounding it.

Tools like Visbanking provide the market and peer data needed to frame these value propositions effectively. When you can benchmark a prospect's potential against industry averages, you can build a powerful, data-backed narrative that moves beyond simple product features to show a clear path to enhanced profitability.

Getting The Deal Across The Finish Line

You have built the relationship and presented a solid value proposition. The next phase is converting potential into revenue, moving from abstract benefits to concrete financial terms.

Vague promises of "better rates" are insufficient. To close the deal, your case must be built on clear, undeniable numbers. This requires a deep understanding of different pricing structures and the ability to demonstrate exactly how your offer impacts a prospect's bottom line.

Finding the Right Pricing Fit

Selecting a pricing model is a strategic decision designed to align with the merchant's business while protecting the bank's margin. The three primary models each have a specific application.

- Interchange-Plus: This model emphasizes transparency. You pass the direct interchange cost from Visa/Mastercard to the merchant and add your markup. It is ideal for high-volume businesses where trust is paramount.

- Tiered Pricing: This model groups rates into simple categories like "Qualified" or "Non-Qualified." While easier for some merchants to understand, its lack of transparency can lead to frustration when transactions are downgraded to more expensive tiers. It can be effective for segments that prioritize simplicity.

- Flat-Rate Pricing: Popularized by companies like Square, this model charges a single percentage plus a per-transaction fee. It is an excellent fit for small businesses with low average ticket sizes due to its predictability, but businesses with significant volume often overpay compared to an interchange-plus structure.

Mastering these models allows you to frame the conversation and propose the structure that offers the most genuine value, thereby building your credibility.

Merchant Services Pricing Model Comparison

Choosing the right model is a critical part of the negotiation. It is about aligning your offer with the merchant’s operational style and business needs.

| Pricing Model | Best For | Bank's Strategic Advantage | Key Negotiation Point |

|---|---|---|---|

| Interchange-Plus | High-volume merchants; businesses that value transparency (e.g., B2B, professional services). | Builds trust and long-term relationships; defensible against low-cost competitors. | Focus on the total "effective rate" and the clarity of having no hidden fees. |

| Tiered Pricing | Merchants who prioritize simplicity over savings; businesses with very consistent transaction types. | Can be more profitable if managed correctly; simple to explain and sell. | Highlight the ease of reconciliation, but be prepared to defend downgrade costs. |

| Flat-Rate Pricing | Micro-merchants, startups, and businesses with low average transaction values. | Easy entry point for new business relationships; competes directly with fintech offerings. | Emphasize predictability and the all-in-one nature of the cost. |

The optimal model creates a win-win scenario, providing tangible value to the merchant while ensuring a profitable, sustainable relationship for the bank.

Use Their Own Data to Make Your Case

Effective negotiation is not about arguing over basis points; it is about presenting a data-backed case that is irrefutable. Your most powerful tool is their own processing statement. A thorough analysis will reveal their true effective rate, hidden fees, and the weaknesses in their current agreement.

Consider a prospect processing $1,000,000 annually on a complex tiered plan. Your analysis shows that while their "qualified" rate appears low, 40% of their transactions are downgraded, resulting in an all-in effective rate of 2.85%.

This is your opening. You present a clear interchange-plus proposal that reduces their effective rate to 2.70%. This 15 basis point reduction yields $1,500 in annual savings. The conversation shifts from a subjective price discussion to a factual analysis of their financial health. A banking sales intelligence platform can amplify this by showing how their costs compare to similar local businesses.

When you use a merchant's own data to demonstrate a clear path to savings, the conversation shifts from opinion to logic. Your proposal becomes the obvious choice.

A Seamless Switch Seals the Deal

Securing a signature is only the beginning. A disorganized onboarding process can damage a new relationship and create immediate buyer's remorse. For many business owners, the fear of operational disruption is the primary reason for staying with an unsatisfactory provider.

A smooth, well-communicated implementation plan is a significant competitive advantage.

A robust onboarding plan includes:

- A dedicated single point of contact for the entire process.

- A clear 30-day timeline with specific dates and milestones.

- Pre-scheduled terminal installation and staff training.

- A follow-up call one week post-launch to ensure smooth operation.

Presenting this plan during final negotiations demonstrates your commitment as a true partner, not just a vendor. This provides the confidence they need to sign the agreement.

Measuring Success and Deepening Relationships

The signed contract is not the finish line; it is the starting point for building a deeper, more profitable client relationship. The initial merchant services account is step one. The strategic victory lies in tracking performance and using that data to drive intelligent cross-selling.

Bank executives must move beyond simple transaction counts to a rigorous analysis of true portfolio profitability.

This requires tracking the right KPIs. Many banks focus solely on processing volume, which can be misleading. A high-volume, low-margin client may appear valuable in a top-level report but contribute less to the bottom line than a smaller, more profitable merchant. A more disciplined approach is required.

The KPIs That Actually Matter

To accurately assess the health and profitability of your merchant services program, you must track a specific set of metrics. This data informs resource allocation, sales strategy adjustments, and relationship management efforts.

Key metrics to monitor:

- Revenue Per Merchant: The ultimate measure of a client's value, calculated after all direct and indirect costs are factored in. It reveals which client segments are driving true profitability.

- Portfolio Processing Volume: While not the only metric, it remains a crucial indicator of market share and program scale.

- Client Attrition Rate: Do not just track how many clients are lost; analyze why they are leaving. This feedback is invaluable for improving your offering.

- Cross-Sell Ratio: This tracks the percentage of merchant clients using at least one other major bank product, such as a commercial loan or treasury management services. It is the clearest indicator of relationship depth.

A low cross-sell ratio is a significant red flag. It indicates that your team is selling a commodity in a silo rather than integrating it into a comprehensive banking relationship, leaving the portfolio vulnerable to competitors.

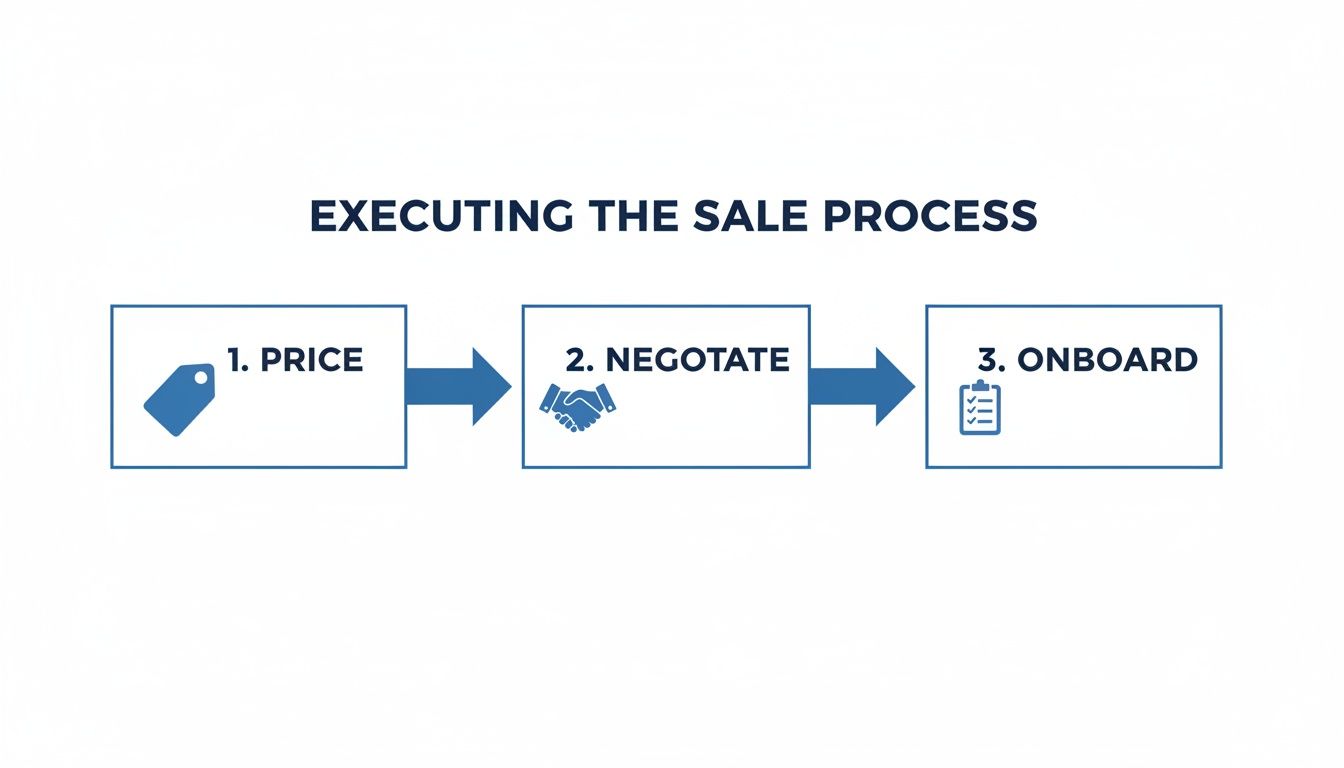

This flowchart illustrates the core process from pricing to onboarding, which marks the beginning of the relationship.

Once a client is onboarded, the critical work of monitoring performance and deepening the relationship begins.

Turning Performance Data into Actionable Intelligence

The real power of these metrics is unlocked when a system automatically surfaces new opportunities from your performance data. This proactive, data-driven approach transforms merchant services from a standalone product into the sticky core of a commercial banking relationship. The right platform connects these dots and creates a trigger system for your relationship managers.

Consider this scenario: A mid-sized retail client typically processes $150,000 per month. Your system flags a sustained spike to $250,000 per month for two consecutive months. This is not just a data point; it is a significant business signal.

This alert should trigger a workflow for the relationship manager. The subsequent call is not a sales pitch but a strategic consultation to understand what is driving the growth. A substantial increase in sales volume might signal a need for:

- An increased commercial line of credit to manage higher inventory costs.

- Treasury management services to optimize cash flow.

- A discussion about financing for future expansion.

This is how data drives smarter banking. Instead of waiting for the client to contact you—or a competitor—you proactively identify their needs based on their own activity. By monitoring these signals, your bank evolves from a reactive service provider into an essential financial partner, building a formidable moat around your most valuable clients.

Visbanking is designed to connect these dots. By integrating client transaction data with broader market and peer benchmarks, our platform helps bank executives not only measure past performance but also anticipate future needs. To see how your institution's cross-sell ratios and client profitability compare, benchmark your performance against the competition.

Burning Questions from Bank Executives

Successfully launching and scaling a merchant services strategy requires clarity and conviction. Here are direct answers to common executive questions.

What’s the Biggest Hurdle We’ll Face Selling Merchant Services?

The primary challenge is the race to the bottom on price. Many merchants view payment processing as a utility, focusing solely on the discount rate. Success requires shifting the conversation from basis points to tangible business value.

Lead with operational leverage, not rates. For example, demonstrate how your automated reporting and dispute management can free up their accounting team for 10 hours a month. Quantifying the value of that saved time almost always outweighs minor rate differences. This reframes your role from vendor to a partner invested in their efficiency.

How Can We Possibly Compete with Fintechs like Square or Stripe?

You compete by leveraging your core strength: the integrated financial ecosystem. A fintech offers a standalone product; you offer a comprehensive financial partnership. This is a battle of solution versus product—and the solution consistently wins.

Emphasize the value of a single point of contact for deposits, lending, treasury, and payments. For a growing business, the simplicity and security of having their merchant settlement account, operating line of credit, and payment gateway under one trusted, regulated institution is a powerful defense. Intelligence from a platform like Visbanking can pinpoint which clients will value this consolidation most.

What are the Most Important Metrics to Track?

Executive teams must look beyond vanity metrics like total processing volume. The critical story is told by profitability and relationship depth. The KPIs that should drive your decisions are:

- Net Revenue per Merchant: Your true north metric. It reveals the precise profitability of each relationship after all costs are accounted for.

- Client Attrition Rate: It is essential to understand not just who is leaving, but why. This feedback is critical for strengthening your value proposition.

- Cross-Sell Ratio: The percentage of your merchant clients utilizing other core banking products. A low ratio indicates a transactional, vulnerable portfolio.

- Average Transaction Size and Volume: These metrics help segment your client base and can serve as an early warning system for changes in their business health, creating proactive outreach opportunities.

Tracking these KPIs provides a complete picture, revealing not only the program's contribution to the bank's bottom line but also its strategic value in forging durable, long-term client relationships.

A modern merchant services strategy is built on superior data and decisive action. Visbanking provides the intelligence to unify market signals with your internal data, empowering your team to find high-value prospects, build compelling offers, and deepen client relationships.

Explore our data and analysis tools to see how you stack up and find your next growth opportunity.

Related Articles

Visbanking Blog

What was the last financial service you bought?<br>Why did you buy it?

Visbanking Blog

Small Business Banking: Finding the Right Financial Partner

Visbanking Blog

Banking Data Analytics: Turning Information Into Profit

Visbanking Blog

Net Interest Margin Secrets: How Top Banks Maximize Profits

Visbanking Blog

Ever wonder how companies sell for 10X Book Value?

Visbanking Blog