A Guide to Modern Banking and Treasury Management

Brian's Banking Blog

Banking and treasury management is the strategic function governing a bank's entire balance sheet. It is the command center responsible for managing liquidity, funding, capital, and the associated financial risks. Its core mandate is to ensure the institution can meet all obligations while navigating market volatility with precision and foresight.

The Strategic Core of Modern Banking and Treasury Management

The perception of treasury as a back-office function is not merely outdated; it is a critical vulnerability in the modern financial landscape. Today’s treasury department operates as the bank's strategic nerve center, guiding trillions of dollars through turbulent markets. It is the team responsible for interpreting complex market signals and translating them into decisive, profitable actions.

The stakes have never been higher. Spurred by rising interest rates and significant investment flows, global banks recently achieved record revenues of $5.5 trillion with $1.2 trillion in net income—an unprecedented performance for any industry. This high-velocity environment has thrust treasury management into the executive spotlight. As detailed in McKinsey's global banking review, intermediated funds have grown 7.0% annually, significantly outpacing the global GDP growth of 4.8%.

From Defense to Offense

A reactive treasury team aims for survival. A proactive, data-driven treasury team creates a distinct competitive advantage. It moves beyond risk mitigation to actively shape the bank's financial trajectory. Mastery of several core pillars is required to make this transition. The following table outlines these functions and their direct impact on business value.

Core Treasury Functions and Their Strategic Impact

| Function | Operational Goal | Strategic Business Impact |

|---|---|---|

| Liquidity & Cash Management | Ensure sufficient cash is available at an optimal price to meet all obligations without fail. | Prevents forced, discounted asset sales, protects franchise value, and maintains the capacity to seize market opportunities. |

| Funding & Capital Management | Secure stable, cost-effective funding and maintain optimal capital levels to support strategic objectives. | Lowers the cost of funds, expands Net Interest Margin (NIM), and enables strategic growth, including acquisitions. |

| Asset Liability Management (ALM) | Actively manage the balance sheet to mitigate interest rate risk and optimize earnings through various economic cycles. | Maximizes profitability across economic scenarios, defends against margin compression, and ensures long-term institutional stability. |

| Payments & Operations | Process all payments with maximum efficiency, security, and regulatory compliance. | Enhances customer loyalty, mitigates operational risk, and provides the foundation for innovative digital banking services. |

| Risk & Compliance | Protect the bank from market, credit, and operational risks while adhering to all regulatory mandates. | Safeguards the bank's assets, avoids costly penalties, and builds confidence among stakeholders and investors. |

This framework is not about administrative housekeeping; it is about building a more resilient and profitable institution.

A critical shift for bank leadership is the recognition that treasury does not just protect value—it actively creates it. Superior treasury management is the key differentiator between banks that merely survive and those that lead the market.

This guide provides a framework for elevating your treasury function into a profit center. Platforms like Visbanking deliver the clear peer benchmarks and market intelligence required to see how decisions on funding costs, asset mix, and risk truly compare to the competition. We invite you to start exploring our data to see where your institution stands.

Mastering Liquidity and Funding in a Dynamic Market

Liquidity and funding are the foundational pillars of treasury management. Liquidity is the capacity to meet obligations on demand without incurring unacceptable losses. Funding is the composition of liabilities—deposits, borrowings, capital—that supports the balance sheet. In a market defined by rapid change, the treasury's role is to orchestrate the interplay between these two forces flawlessly.

A well-structured balance sheet provides the strategic flexibility to turn a potential crisis into a manageable event. The decisions made during periods of stress have a direct and lasting impact on shareholder returns.

A Practical Liquidity Scenario

Consider the treasury team at a community bank facing a sudden outflow of $50 million from several large depositors. The immediate challenge is not just to find cash, but to source the right cash at the right price.

Two primary options are available:

- Sell Securities: Liquidate $50 million from the available-for-sale (AFS) portfolio, which is currently yielding 2.50%.

- Tap FHLB Advances: Draw a $50 million advance from the Federal Home Loan Bank at a cost of 4.75%.

Selling the securities permanently sacrifices the 2.50% yield. The FHLB advance provides immediate liquidity but introduces a new 4.75% cost that will compress the net interest margin. The optimal decision depends entirely on the bank’s specific interest rate position and overarching strategy. This is precisely why high-fidelity, real-time data is not a luxury, but a necessity for sound decision-making. Our guide to bank liquidity management provides a deeper analysis of these trade-offs.

Translating Regulation into Strategy

Many executives view regulatory metrics as compliance burdens. This is a missed opportunity. Astute leaders recognize that the Liquidity Coverage Ratio (LCR) and Net Stable Funding Ratio (NSFR) provide a strategic blueprint for constructing a fortress balance sheet.

- Liquidity Coverage Ratio (LCR): This metric stress-tests the ability to survive a 30-day period of severe cash outflows. The strategic question is not simply, "Did we meet the 100% minimum?" but, "What is the optimal cost of achieving this target?" Over-investing in low-yield high-quality liquid assets (HQLA) erodes NIM. Under-investing creates unacceptable risk.

- Net Stable Funding Ratio (NSFR): This ratio enforces a one-year view of funding stability, ensuring that long-duration assets are supported by stable funding sources. It prevents the funding of long-term commercial real estate loans with volatile, short-term wholesale deposits, imposing critical balance sheet discipline.

When viewed as strategic instruments, these ratios cease to be regulatory hurdles. They become the guardrails that guide the institution toward greater resilience and profitability.

The Decisive Edge of Peer Benchmarking

How can you objectively assess your funding strategy? Internal reports provide an incomplete picture. The critical context is performance relative to the market. This is where data intelligence platforms like Visbanking deliver a significant competitive edge.

Suppose your bank's cost of funds is 1.75%. In isolation, this figure is meaningless. However, if a curated peer group is averaging 1.60%, that 15-basis-point gap is no longer just a number—it is a direct challenge to your entire deposit-gathering strategy.

This single data point triggers a series of essential questions:

- Are our deposit rates misaligned with the market, forcing reliance on more expensive funding?

- Is our product mix deficient in valuable, low-cost non-interest-bearing accounts?

- Are certain branches underperforming in attracting core deposits?

Armed with comparative data, you transition from conjecture to action. You can recalibrate rates, launch targeted marketing campaigns, or implement focused team training. This is the essence of modern treasury: using data to identify performance gaps and drive measurable financial results. You can explore our data today and see precisely how your institution compares.

The Art and Science of Asset Liability Management

Asset Liability Management (ALM) is not an academic exercise in duration gaps and convexity. At its core, it is the practice of proactively steering the bank's financial future. The fundamental question ALM answers for the executive team is: How do we protect and grow earnings, regardless of interest rate movements?

The global commercial banking industry recently saw revenues climb to an estimated $3.9 trillion, representing a 4.3% compound annual growth rate over five years, according to IBISWorld. This growth occurred despite central banks driving interest rates to historic lows to counter economic headwinds. Such resilience is not accidental; it is the direct outcome of effective ALM—structuring the balance sheet to perform across multiple economic scenarios.

Modeling a Realistic Interest Rate Scenario

Consider a community bank with $1 billion in assets. The bank is "liability-sensitive," meaning its liabilities, primarily deposits, will reprice faster than its assets, such as fixed-rate commercial loans, in a rising-rate environment.

The Federal Reserve signals a 75-basis-point (0.75%) rate hike over the upcoming quarter. The bank's Asset Liability Committee (ALCO) must immediately quantify the impact on Net Interest Income (NII).

A preliminary analysis reveals the following exposure:

- Assets Repricing: $400 million in floating-rate loans will reprice upward, adding $3 million to annual interest income ($400M * 0.0075).

- Liabilities Repricing: $650 million in interest-bearing deposits and other funding will also reprice, increasing annual interest expense by $4.875 million ($650M * 0.0075).

The net result is a projected annualized NII decline of $1.875 million. This is a quantifiable risk that demands a strategic response, not a passive "wait and see" approach.

From Data Insight to Strategic Action

The data does not just identify the problem; it illuminates the potential solutions.

The purpose of ALM is not merely to generate a report forecasting an NII decline. It is to provide the data-driven intelligence required to prevent that decline from materializing.

The ALCO has several strategic levers at its disposal, each with distinct trade-offs:

- Execute an Interest Rate Swap: The bank could enter a pay-fixed, receive-floating swap on a notional amount of $250 million. This derivative synthetically converts a portion of the fixed-rate loan portfolio to floating-rate, immediately hedging the liability sensitivity and protecting NII.

- Adjust the Loan Origination Mix: The committee could direct the lending team to prioritize floating-rate commercial and industrial (C&I) loans over fixed-rate mortgages, organically shifting the balance sheet's risk profile over several quarters.

- Restructure the Investment Portfolio: The bank could sell shorter-duration bonds and reinvest the proceeds into longer-duration assets to better match the liability structure.

The optimal path is not determined by intuition but by rigorous data analysis. For a deeper examination of these strategies, see our guide on bank asset liability management.

This is where a data intelligence platform like Visbanking becomes indispensable. Your ALCO can simulate these scenarios with high precision, testing assumptions against real-world data. Crucially, it can also benchmark your interest rate risk against your peers. Discovering that your NII sensitivity is 5% higher than the peer average provides objective, compelling evidence to execute a decisive hedging strategy before an adverse market move. Benchmark your bank's performance today to see where you stand.

Navigating Global Risk and Cross-Border Complexity

When banking operations cross international borders, the risk landscape transforms. Managing a global balance sheet is no longer the exclusive domain of money-center banks; it is a core competency for any institution participating in the global economy. The treasury team is the first line of defense against the market, credit, and operational risks that now originate from any corner of the world.

The scale of this interconnectedness is immense. Cross-border bank credit has expanded to $37 trillion worldwide, increasing by $917 billion in a single recent quarter. This 10% year-over-year growth underscores the central role of treasury management in global liquidity, with $773 billion of that quarterly flow directed to financial sector borrowers. You can explore the full scope of these international banking statistics to appreciate the sheer scale.

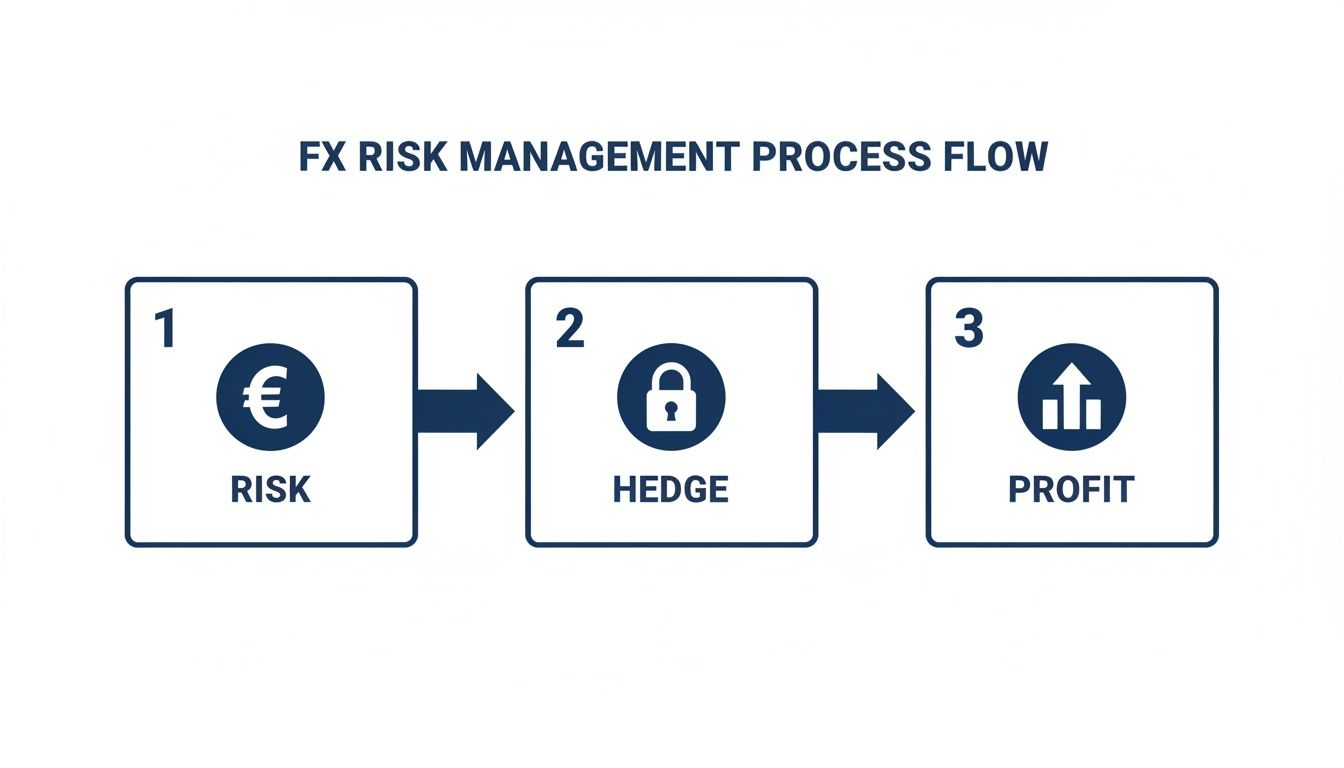

Quantifying Foreign Exchange Risk: A Case Study

Consider a U.S. regional bank with a loan portfolio denominated in €200 million. At an exchange rate of 1.08 USD/EUR, this portfolio is valued at $216 million on its U.S. dollar balance sheet. The primary threat is foreign exchange (FX) risk.

If the U.S. dollar strengthens to 1.03 USD/EUR, the value of the €200 million portfolio falls to $206 million. Without an effective hedge, the bank faces an immediate $10 million unrealized loss, directly impacting its P&L and capital ratios.

In today's interconnected financial system, ignoring foreign exchange risk is not a strategy—it is a high-stakes gamble. The decision to hedge is a conscious act to insulate shareholder value from market volatility.

Treasury must act decisively. By executing a simple forward contract, the bank can lock in the 1.08 exchange rate for a future date, neutralizing the FX risk and guaranteeing the portfolio’s value remains $216 million. The cost of the hedge, typically a few basis points, is the price of certainty.

The Data-Driven Approach to Hedging

Effective hedging decisions are built on superior data analytics. A top-tier treasury function integrates multiple data streams to protect the bank, including insights from global hubs on practices like smart forex risk management for Hong Kong businesses.

This data-driven approach includes:

- Macroeconomic Analysis: Monitoring leading economic indicators—GDP growth, inflation, central bank policy—in key foreign markets provides early warnings of potential currency shifts.

- Counterparty Risk Assessment: Rigorously analyzing the creditworthiness of hedging counterparties is essential to ensure they can meet their obligations.

- Peer Benchmarking: Comparing international exposures to peer institutions provides critical context. Discovering that your unhedged foreign loan portfolio is 25% larger than the peer average is a clear signal to re-evaluate your risk appetite.

A platform like Visbanking provides a decisive advantage by integrating macroeconomic data with detailed peer analytics. This enables treasury teams to shift from a reactive to a proactive risk framework—one that anticipates market shifts, accurately quantifies potential impacts, and informs smarter capital allocation. The ability to benchmark your international exposures provides the objective data needed to act with confidence.

The Technology Stack Powering Modern Treasury

Modern treasury runs on a seamlessly integrated technology stack. As an executive, your role is not to be an IT expert, but to ensure your bank's technology ecosystem breaks down data silos, not reinforces them. The objective is to create a single source of truth that transforms raw data into a competitive advantage.

Spreadsheets and fragmented legacy systems are no longer viable. They create dangerous operational blind spots and impede decision-making, directly impacting profitability. A modern stack ensures data flows from its point of origin to its point of strategic action, providing leadership with a consolidated, real-time view of the entire balance sheet.

Following the Data: A Single Deposit's Journey

To illustrate this integration, consider the journey of a new $10 million corporate deposit. This is not just a transaction; it is a piece of intelligence that must inform multiple functions nearly instantaneously.

- Core Banking System: The deposit is recorded, updating the customer's balance and the bank’s aggregate liability position. This is the data's point of entry.

- Treasury Management System (TMS): The data flows directly to the TMS, where the treasury team sees the $10 million appear in their daily cash position report. They can immediately decide how to deploy this liquidity—for instance, paying down a higher-cost FHLB advance or purchasing short-term securities. Increasingly, teams rely on advanced treasury management systems to accelerate these workflows.

- ALM Modeling Software: Simultaneously, the deposit data is fed into the Asset Liability Management model. The ALM team runs simulations to assess how this new, potentially rate-sensitive deposit alters the bank's interest rate risk profile and its impact on NII projections.

- Business Intelligence (BI) Platform: All data streams converge in a BI platform like Visbanking. Here, the $10 million deposit is no longer an isolated line item. It is contextualized within a larger strategic picture.

This data flow is about connecting interdependent functions. The diagram below illustrates a similar process for managing foreign exchange risk, where the principle is identical: connecting a risk trigger to a protective action.

This illustrates how technology links risk identification directly to hedging activities and, ultimately, to the protection of profit margins.

From Siloed Reports to Integrated Intelligence

The journey of that $10 million deposit highlights the most critical imperative for bank executives: an integrated technology stack eliminates the delays and errors inherent in manual, spreadsheet-based processes. It creates a unified data environment where every decision is informed by the same complete, real-time information.

In an integrated system, a deposit is not just a liability. It is an input for cash management, a variable in risk models, and a data point for performance benchmarking. This holistic view is the source of strategic advantage.

This shift empowers your team to move beyond reporting historical events to asking smarter, forward-looking questions. With a platform like Visbanking, you can instantly benchmark that new deposit type against your peers. Are you acquiring these funds at a competitive rate? How does this new capital impact your deposit mix relative to top-performing banks in your asset class?

The right technology provides not just reports, but answers. It surfaces the critical insights required to make faster, better decisions about funding, risk, and overall strategy. For bank executives, this is the goal: a technology stack that drives action, not just analysis.

Turning Treasury Intelligence into a Competitive Edge

Treasury management must be repositioned from a risk-mitigation function to a value-creation engine. For executives and directors, the objective is to transform the treasury department from a cost center into a direct driver of profitability. This requires translating theory into action, ensuring every decision is linked to a measurable improvement in performance.

The connection between a data-driven treasury and the bottom line is direct and powerful. Excellence in balance sheet management manifests immediately in core metrics: Return on Equity (ROE), Net Interest Margin (NIM), and the efficiency ratio. These are not abstract figures for board presentations; they are the tangible results of strategic treasury execution.

The Financial Power of Marginal Gains

Consider the impact of a seemingly minor adjustment. For a $2 billion bank, a 5-basis-point (0.05%) improvement in its overall cost of funds translates directly to $1 million in pre-tax income annually. This is not a hypothetical exercise. It is precisely the type of opportunity uncovered by peer benchmarking, which can reveal a suboptimal funding mix or mispriced deposit products relative to competitors.

Banks that consistently outperform their peers are not playing a different game. They are playing with superior information—data that allows them to identify and capture these marginal gains with speed and precision.

This is the essence of treasury intelligence: converting data points into dollars. An optimized securities portfolio can add 10 basis points in yield. A proactive hedging strategy can shield NIM from a 25-basis-point adverse move in interest rates. Each of these data-backed decisions compounds to create a significant competitive advantage. Our deeper analysis of business intelligence for banks details how to build this capability.

The Deciding Factor in a Competitive Market

The market does not reward complacency. Institutions operating on stale reports and legacy processes will be outmaneuvered by those adopting a more dynamic, data-centric approach. The winners will be those who equip their treasury teams with the tools to anticipate market shifts, challenge assumptions with objective data, and execute with conviction.

In a crowded field, the banks that win are those using superior data intelligence to out-think and outperform the competition. They make smarter funding decisions, manage risk with greater foresight, and deploy capital more effectively. They do not merely react to the market; they position themselves ahead of it.

The defining question for every bank executive is this: Does your treasury team possess the intelligence required not just to compete, but to lead? Benchmark your performance against your peers and uncover your greatest opportunities.

Questions We Hear All the Time

We frequently address questions from bank executives seeking to enhance their treasury functions. Here are some of the most common inquiries, with direct answers.

We Want to Improve Our Treasury Management. Where Do We Even Start?

The essential first step, before any other initiative, is to establish a single source of truth for your data. A sound strategy cannot be built on a fragmented data foundation.

Your data is likely dispersed across lending, deposit operations, and finance departments. These silos must be dismantled. This means integrating your core banking system, ALM models, and investment portfolio data into a unified platform.

With a clean, consolidated view, you can accurately assess your true liquidity position, interest rate risk, and actual cost of funds. This provides the essential baseline upon which all subsequent strategic decisions will be built.

We're a Mid-Sized Bank. How Can We Afford an Advanced Treasury Tech Stack?

The belief that advanced technology is exclusive to the largest institutions is a misconception. The landscape has fundamentally changed. Large, upfront capital expenditures for on-premise systems with lengthy implementation times are no longer necessary.

Today's leading solutions are cloud-based platforms offered as a service (SaaS). This model provides a lower total cost of ownership, rapid implementation, and predictable subscription-based pricing. The playing field has been leveled.

Consider the return on investment. A modest investment in technology that enables you to increase NIM by a few basis points or avoid a single liquidity event pays for itself many times over. It is not an expense; it is an investment in resilience and profitability.

A best-in-class Asset Liability Committee (ALCO) meeting spends less than 20% of its time reviewing historical data and 80% on forward-looking strategy. They are stress-testing economic scenarios, benchmarking against peers, and making decisive policy adjustments.

How Often Should Our ALCO Meet, and What's the Right Focus?

At a minimum, your Asset Liability Committee (ALCO) should meet quarterly. However, in today's volatile environment, high-performing institutions convene monthly to stay ahead of market developments.

The critical change, however, is not the frequency but the focus of these meetings. The objective must shift from reviewing static, backward-looking reports to engaging in dynamic, forward-looking strategy.

This pivot requires superior data. When your ALCO is equipped with tools that deliver real-time peer comparisons and market intelligence, the conversation transforms. You move beyond reviewing a report packet to actively debating strategic positioning. You can pressure-test assumptions against hard data and make faster, more confident decisions that directly enhance the bank's performance.

At Visbanking, we believe the best decisions are driven by the clearest data. Our Bank Intelligence and Action System is designed to unify your complex financial, regulatory, and market data into analytics that demand action. It’s time to move from viewing dashboards to making decisive moves. See how your institution stacks up against the competition. Learn more at https://www.visbanking.com.

Related Articles

Visbanking Blog

Capital Banking in the USA: An Overview of Investment Services, Financial Instruments, and Regulations

Visbanking Blog

Bank Capital Requirements: The Ultimate Survival Guide

Visbanking Blog

Bank Failure: Understanding the Risks and Protections for Consumers

Visbanking Blog

Major Banks in US by Asset Size

Visbanking Blog

Net Interest Margin Secrets: How Top Banks Maximize Profits

Visbanking Blog