A Bank Executive's Guide to Predictive Analytics

Brian's Banking Blog

In banking, predictive analytics is the discipline of using institutional and market data to anticipate future outcomes. It represents a strategic shift from retrospective reporting to forward-looking intelligence. This allows executives to preemptively manage credit risk, detect fraud, and identify growth opportunities before they become apparent to the competition.

Why Predictive Analytics is a Board-Level Imperative

Historical performance reports are rearview mirrors; they confirm where the institution has been but offer no guidance on the road ahead. Predictive analytics closes this gap. This is not a technology upgrade; it is a fundamental evolution in strategy, moving from reviewing the past to actively shaping the future.

This shift transforms data from a static compliance asset into a dynamic intelligence engine, enabling leadership to move beyond descriptive dashboards and ask strategically vital questions about what is next.

From Reactive to Proactive Operations

Instead of reacting to a spike in loan delinquencies, you can predict which commercial or consumer accounts are most likely to enter distress within the next six to twelve months. Rather than discovering fraud after the financial loss, you can identify and block anomalous transactions in real time. This is the foundation of modern risk management and capital allocation.

A proactive strategy, fueled by predictive models, enables a bank to deploy capital more efficiently, price risk with greater precision, and insulate its balance sheet from market volatility. It is the difference between navigating with a rearview mirror and a forward-looking, real-time GPS.

Integrating Data for a Complete View

Effective prediction requires a holistic view of the operating environment. Analyzing internal transaction data in isolation is insufficient. The strategic advantage is created by integrating proprietary data with external market and regulatory intelligence.

This is where a dedicated bank intelligence platform becomes indispensable. A system like Visbanking aggregates disparate, complex datasets into a unified source for analytical models, providing a clear signal from the noise. Crucial external sources include:

- FDIC Call Reports: To benchmark performance against peers and identify systemic risks.

- HMDA Filings: To anticipate mortgage market trends and ensure fair lending compliance.

- UCC Filings: To monitor commercial lending activity and flag potential credit deterioration.

By integrating these sources, banks develop robust models that identify market shifts and predict customer behavior with actionable clarity. Our overview of banking analytics details the tools involved. This is how data transitions from a compliance burden to a primary strategic asset.

Translating Data Into Financial Performance

Data holds potential, but predictive analytics is the engine that converts that potential into measurable profit. For bank executives, the operative question is not about the technology's validity but its application to core business challenges. The objective is to direct analytical power where it will have the most significant financial impact, turning data points into decisive, dollar-driven actions.

This strategic imperative is why the market for predictive analytics in the banking industry is forecast to expand from $5.2 billion in 2024 to $19.9 billion by 2033. This growth is a direct response to the pressures on financial institutions: vast data volumes, stringent regulations, and persistent fraud threats. You can understand the forces driving this industry shift through deeper market analysis.

Below are four areas where predictive analytics delivers an immediate and material impact on the bottom line.

Refining Credit Risk Assessment

Traditional credit scoring models are inherently retrospective, analyzing past behavior to assess current risk. They often fail to capture leading indicators of a borrower's future financial stability. Predictive analytics shifts the paradigm from a historical to a forward-looking assessment, incorporating a richer dataset to forecast the probability of default with significantly higher accuracy.

By combining internal customer data with external sources—such as UCC filings or macroeconomic data from the Bureau of Labor Statistics (BLS)—a comprehensive risk profile emerges. A unified data intelligence platform like Visbanking integrates these sources, enabling models to detect distress signals long before a payment is missed.

Practical Example: A $2.5 billion community bank implemented a predictive model for its commercial loan portfolio. By analyzing client cash flow trends against industry-specific economic data, the model identified a segment of borrowers whose true default risk was 35% higher than their traditional credit scores suggested. This early warning enabled the bank to proactively restructure loans, reducing its loan loss provisions by an estimated 6%, or approximately $1.2 million, in the first year.

Identifying Fraud in Real Time

Fraud detection has evolved from a forensic, after-the-fact process to a real-time, automated defense. Predictive models are the core of this defense, analyzing thousands of transactions per second to identify patterns inconsistent with established customer behavior.

These systems learn a customer's typical transaction profile—spending habits, geographic locations, and transfer patterns. Any significant deviation, such as an unusual international purchase or a sudden large withdrawal, is flagged instantaneously. This intervention often occurs before funds leave the institution, preventing financial loss and eliminating the need for costly recovery investigations.

Forecasting Customer Churn

Acquiring a new customer is substantially more expensive than retaining an existing one. Predictive analytics provides an early-warning system to identify high-value customers at risk of attrition, creating an opportunity for proactive intervention.

Models analyze subtle behavioral shifts—declining account balances, reduced login frequency to digital banking platforms, or a drop in transaction volume. These leading indicators, often missed by relationship managers, trigger alerts. This allows retention teams to execute targeted campaigns with personalized offers, reinforcing the value proposition before the relationship is severed.

- Proactive Intervention: Instead of reacting to a closed account, an alert is triggered when a customer's churn risk score crosses a predefined threshold.

- Targeted Offers: Models can suggest the most effective retention tactic, such as a fee waiver, an improved deposit rate, or a consultation with a financial advisor.

- Improved Profitability: Retention efforts are focused on the most valuable customer segments, maximizing the return on investment.

Optimizing Customer Lifetime Value

Predictive analytics enables a strategic shift from a product-centric to a customer-centric model. By forecasting a customer's total potential value over the entire relationship—their Customer Lifetime Value (CLV)—banks can make more informed decisions on marketing spend, product development, and service levels.

A CLV model helps answer critical strategic questions. Which customers are most likely to require a mortgage or wealth management services in the future? What is the appropriate level of investment for serving a specific customer segment? This foresight ensures resources are allocated to cultivate the most profitable and loyal relationships. Our guide on leveraging banking data analytics offers a deeper analysis of these customer-centric strategies.

By embedding these capabilities into core operations, a bank moves beyond reporting on past events. It begins to anticipate needs, mitigate risks, and seize opportunities—directly converting raw data into a stronger balance sheet.

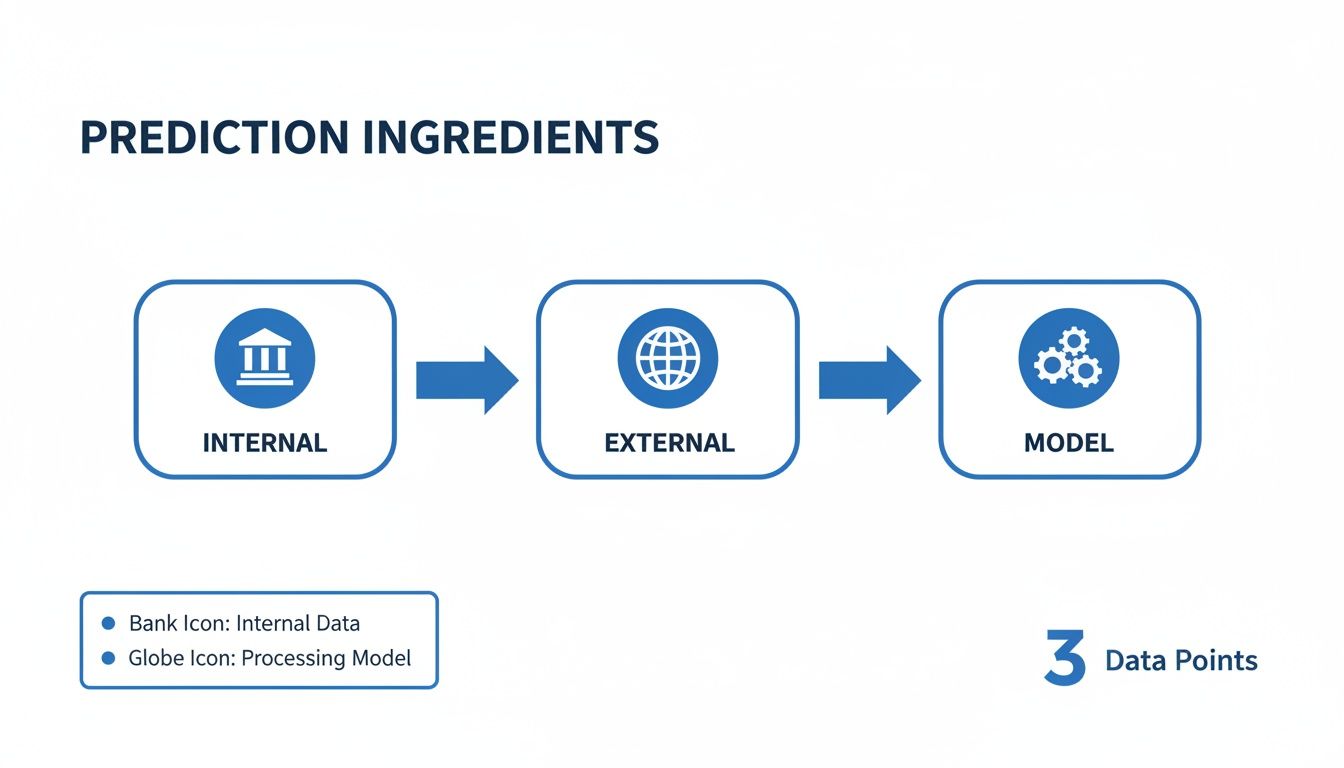

The Anatomy of a High-Value Prediction

Accurate predictions are not accidental; they are engineered from specific, high-quality components. For bank executives, understanding this process is crucial. It is not about mastering the technical minutiae but about grasping how raw data is transformed into a strategic asset that informs risk management, growth initiatives, and capital planning.

The core principle is the synthesis of two complementary data types: internal proprietary data and external market intelligence. This integration breaks down information silos to create a unified, 360-degree view of the customer within their economic context.

This flowchart illustrates the essential components for building a powerful predictive model.

The methodology is straightforward: combine internal customer data with external market data, then process the unified dataset through a purpose-built analytical model.

Unifying Internal and External Data Streams

First, internal data represents the information generated through daily operations—transaction histories, loan performance records, customer demographics, and product utilization. This provides a detailed portrait of existing customer relationships.

However, relying solely on internal data provides an incomplete picture. To anticipate future trends, this information must be enriched with external data that supplies critical market context. A bank intelligence platform like Visbanking automates this integration, programmatically incorporating vital datasets:

- FDIC Call Reports & NCUA 5300 Data: These regulatory filings offer a direct view into the financial health and strategic positioning of all U.S. banks and credit unions. This enables performance benchmarking, systemic risk identification, and early detection of economic shifts.

- HMDA Filings: Home Mortgage Disclosure Act data provides granular detail on mortgage lending activity across the market. It is essential for understanding the competitive landscape and ensuring adherence to fair lending regulations.

- UCC Filings: Uniform Commercial Code filings serve as a powerful leading indicator for commercial lending. They reveal which businesses are securing new debt and with which lenders, providing intelligence on both competitive opportunities and emerging credit risks.

The fusion of these internal and external sources creates a dataset far more powerful than its individual parts, enabling genuine strategic foresight.

Demystifying the Predictive Model

Once the data is prepared, it is fed into a predictive model. This is not a "black box" but a specialized algorithm designed for a specific analytical task.

A credit risk model, for example, is engineered to identify the combination of internal and external factors that have historically preceded loan defaults. A customer churn model is calibrated differently, designed to detect subtle behavioral signals that indicate a customer may be considering competitors. These models do not guess; they calculate probabilities based on patterns identified across millions of data points. The key to maximizing their effectiveness is unlocking the power of AI to discover these non-obvious correlations.

Ensuring Transparency with Explainable AI (XAI)

In a highly regulated industry like banking, a prediction is operationally useless if its rationale cannot be explained. This makes Explainable AI (XAI) a non-negotiable requirement. Regulators, auditors, and the board of directors must be able to understand the "why" behind an automated decision, particularly for critical functions like credit underwriting.

A transparent model does not just provide an answer; it shows its work. If a loan application is flagged as high-risk, an explainable model will specify the contributing factors—such as a high debt-to-income ratio combined with negative trends in the applicant's industry sector—providing a clear, defensible rationale.

This transparency is essential for meeting fair lending standards and building institutional trust in analytical models. It ensures that models are not only accurate but also fair, auditable, and compliant. With a clear understanding of what drives the insights, leadership can act on them with confidence.

Measuring the ROI of Predictive Intelligence

Any significant capital investment must answer a direct question: what is the return? For predictive analytics in banking, the return is measured on the bottom line. The transition from retrospective dashboards to forward-looking intelligence provides a distinct and quantifiable financial advantage.

The primary value is derived from making smarter, faster decisions across the institution. Instead of reacting to market shifts or spikes in default rates, the bank anticipates them. This capability directly enhances operational efficiency, reduces credit and fraud losses, and drives revenue growth.

Defining Your Key Performance Indicators

To measure ROI effectively, focus must be on business outcomes, not the analytical models themselves. The correct key performance indicators (KPIs) create a direct link between predictive insights and financial performance, making the return on investment unambiguous.

Consider these tangible outcomes:

- A 15% reduction in losses from fraudulent transactions by identifying and blocking them pre-execution.

- A 10% increase in cross-sell success from marketing offers tailored to a customer's predicted needs.

- A 20% reduction in manual loan application review time by automatically segmenting applications based on risk profiles.

These are not theoretical figures; they are the direct results of applying predictive intelligence to core banking functions. Industry-wide, institutions implementing these tools report 10-15% sales increases and 15-20% cost reductions. It is no surprise the market for these solutions is projected to reach $100.20 billion by 2034. You can discover more insights on how predictive analytics powers business decisions here.

Quantifying the Before-and-After Impact

The most compelling business case is a simple before-and-after comparison. This requires clean, comprehensive data—not only for building the models but also for measuring their success. A unified intelligence platform like Visbanking provides this foundation by integrating siloed sources like FDIC call reports and UCC filings into a single, coherent view.

The table below illustrates the real-world performance improvements banks achieve through the effective implementation of predictive analytics.

Quantifying the Impact of Predictive Analytics

| Banking Function | Metric Without Predictive Analytics | Metric With Predictive Analytics | Percentage Improvement |

|---|---|---|---|

| Credit Risk | 3.5% Loan Default Rate | 2.8% Loan Default Rate | 20% Reduction |

| Fraud Detection | 0.1% of Transaction Value Lost | 0.075% of Transaction Value Lost | 25% Reduction |

| Marketing | 1.5% Campaign Conversion Rate | 3.0% Campaign Conversion Rate | 100% Increase |

| Operational Efficiency | 4 hours for Manual Underwriting | 1.5 hours for Automated Review | 62.5% Reduction |

The data is conclusive. Predictive intelligence is not a cost center; it is a significant profit driver. It delivers a clear competitive advantage by enabling teams to capitalize on opportunities and mitigate risks with superior speed and precision.

Ultimately, the ROI extends beyond incremental gains. It is about building a more resilient, intelligent, and profitable institution. By benchmarking current performance and analyzing the predictive signals within market data, you can identify the highest-value starting points for implementation.

Your Practical Roadmap to Implementation

Transitioning predictive analytics from a strategic concept to an operational reality requires a disciplined, pragmatic implementation plan. The objective is not a disruptive "big bang" overhaul but a phased rollout designed to deliver immediate value and build institutional momentum.

A successful roadmap avoids common pitfalls: data integration challenges, internal skill gaps, and "analysis paralysis."

The path forward begins with a narrowly focused, high-impact pilot project to prove the concept's value. This is followed by the development of a robust data foundation and, finally, the scaling of proven models across the institution. This methodology manages risk and ensures each phase delivers a measurable return.

Phase 1: Start with a High-Impact Pilot

Begin by selecting a single, well-defined business problem where a predictive model can achieve a clear, quantifiable victory. Resist the temptation to address all challenges simultaneously. A focused pilot demonstrates the potential of the technology, builds internal consensus, and provides invaluable lessons for subsequent phases.

A successful pilot project has two key characteristics:

- Measurable Impact: The outcome is directly tied to an existing KPI. Examples include reducing loan application review times by 25% or identifying 10% of high-risk churn candidates within a specific customer segment.

- Accessible Data: The necessary data for the model already exists and is reasonably accessible. This prevents the project from becoming mired in a lengthy data engineering effort before any modeling can begin.

A mid-sized commercial bank could pilot a model to predict which business clients are most likely to require a new line of credit within the next 90 days. Success is measured by the conversion rate of targeted offers. A win here builds a powerful business case for broader implementation.

Phase 2: Build a Solid Data Foundation

With an initial success demonstrated, the priority shifts to constructing a unified data infrastructure. This is often the most challenging phase, as it requires breaking down the data silos that exist within nearly every financial institution.

The accuracy and reliability of predictive models are entirely dependent on the quality of the data they consume. A clean, integrated data source is a non-negotiable prerequisite for scaling analytics.

This involves consolidating disparate datasets—from the core banking system to external sources like FDIC Call Reports and HMDA filings. A solid data foundation ensures models are fed comprehensive, high-quality information, which is essential for generating trustworthy predictions. For a deeper dive, review our guide on data integration best practices.

Phase 3: Scale Success and Accelerate Value

Attempting to build an in-house data science team and the associated MLOps (Machine Learning Operations) infrastructure from the ground up is a multi-year, multi-million-dollar endeavor with a high risk of failure. The required talent is scarce, the technology is complex, and the time-to-value is unacceptably long. Partnering with a specialized platform provides a decisive advantage.

A platform like Visbanking provides the production-grade data pipelines, feature stores, and pre-built model frameworks necessary to become operational quickly. This allows your bank to circumvent the enormous cost and complexity of in-house development. You gain immediate access to an infrastructure that has been tested, secured, and optimized for the specific demands of the banking industry.

This approach is becoming the industry standard. Approximately 66% of global financial institutions have already integrated predictive analytics into their core operations. Discover more insights about this seismic shift in banking strategy.

By leveraging a proven Bank Intelligence and Action System, you shift focus from building technology to acting on intelligence. This practical roadmap enables your team to concentrate on what matters most: making smarter, faster decisions that drive performance, manage risk, and secure a sustainable competitive advantage.

From Insight to Action: Gaining Your Competitive Edge

The purpose of predictive analytics is not to generate more complex reports; it is to drive intelligent, decisive, and profitable action. Dashboards report on the past; predictive intelligence dictates the next move. This is the critical leap from passively observing market trends to actively shaping the bank's future.

By transforming vast quantities of raw data into clear, forward-looking signals, you empower your teams to manage risk with precision, identify opportunities missed by competitors, and build a foundation for sustainable growth. Your data is your most valuable asset, but only when it is put to work. When models can accurately forecast loan demand, flag a high-value customer at risk of attrition, or pinpoint the next ideal prospect, you establish an undeniable competitive advantage.

Activating Your Data Intelligence

Translating insight into action requires a sharp operational focus. For example, using customer data to drive personalized communication is a proven strategy. Reviewing CRM email personalization best practices can provide a tactical playbook for converting predictive signals into customer engagement that drives revenue.

The objective is to embed this intelligence directly into daily workflows. For example, a predictive model flags that a commercial client's risk profile has changed based on recent UCC filing activity. The action is an immediate, automated alert to the relationship manager, prompting a proactive account review. There is no manual analysis or delay.

Data intelligence without a clear path to execution is a wasted opportunity. The true ROI of predictive analytics is realized when insights trigger specific, value-creating actions across lending, marketing, and risk management.

The signals needed to outperform the competition already exist within your data. The next step is implementing the right system to detect and act upon them. A true Bank Intelligence and Action System delivers this capability, enabling you to benchmark performance against peers and harness the predictive signals hidden within your market.

Addressing Executive Questions

Discussions with bank executives about implementing predictive analytics invariably surface three core concerns: resource constraints, regulatory scrutiny, and the timeline for realizing a return on investment. Here are direct answers to these critical questions.

"We are a mid-sized bank. How can we implement this without a large data science team?"

This is the most common concern. Building a full data science function is a costly and lengthy process. The strategic alternative is to partner with a specialized platform. This provides immediate access to proven data pipelines and pre-built models for high-impact use cases like credit risk modeling and customer churn prediction. This approach bypasses the significant upfront investment in hiring and infrastructure, allowing the bank to focus on acting on the intelligence provided.

"Aren't these models a 'black box'? How will our examiners view this?"

This is a valid regulatory concern. Modern analytical platforms are built on the principle of 'Explainable AI' (XAI). This means the models are transparent, providing clear, human-readable justifications for every prediction.

If a model flags a commercial loan application as high-risk, it will specify the reasons: for example, deteriorating cash flow trends in the borrower's industry sector, combined with an increase in UCC filings by their direct competitors. This level of transparency is essential for satisfying regulators, ensuring fair lending practices, and building internal trust in the system's outputs.

"When can we expect to see a return on this investment?"

With a platform-based approach, the timeline for ROI is significantly compressed. By initiating a focused pilot project using proven tools, most institutions can demonstrate a measurable impact within one to two fiscal quarters. For instance, a fraud detection model can begin reducing losses by 5-10% within six months. Larger strategic initiatives, such as recalibrating the entire loan portfolio based on forward-looking risk, will demonstrate their full value over a 12- to 18-month horizon. The key is to secure a tangible early win to build momentum and validate the investment.

The signals that will define your bank's future performance are already present in your data. The challenge is having the right system to interpret them. Visbanking is that system—a Bank Intelligence and Action System designed to help you benchmark performance, identify predictive signals, and gain a decisive competitive edge.

Related Articles

Visbanking Blog

Banking Data Analytics: Turning Information Into Profit

Visbanking Blog

BIAS: A New Dawn in Banking Decision-Making

Visbanking Blog

Fastest Growing Banks: Who's Winning the Asset Race?

Visbanking Blog

Revolutionize Your Banking Operations with Data-Driven Insights from BIAS

Visbanking Blog

Revolutionize Your Bank's Performance with BIAS: Unlocking the Future of Visual Banking Data

Visbanking Blog