Stress Testing for Banks: Strategies for Financial Resilience

Brian's Banking Blog

The Evolution of Stress Testing: From Optional to Essential

Stress testing for banks wasn't always the bedrock of financial stability we know today. Back in the early 1990s, individual banks primarily used stress tests internally for risk management. This was a more localized and less formal approach compared to the comprehensive systems we see now. But this early stage paved the way for the vital role stress testing now plays in the global financial system.

This change highlights the increasing awareness of how important stress testing is for maintaining financial stability. The concept itself has changed dramatically, especially after the 2008 financial crisis. The crisis revealed how undercapitalized banks struggled, leading to broad economic consequences.

This prompted a global regulatory shift, making stress tests mandatory for large banks. This evolution from optional to essential marks a significant change in finance. It emphasizes the growing need to assess and mitigate potential financial risks proactively. The growing use of AI in stress testing further reinforces this trend. For a deeper dive into this topic, explore our perspective on AI in Financial Services.

From Internal Tool to Global Standard

The 1996 market risk amendment to the Basel Capital Accord was a pivotal moment. It formalized stress testing for evaluating trading portfolios, signaling a move towards greater standardization and regulatory oversight.

By the early 2000s, authorities began broadening their perspective on stress tests. This reflected a growing understanding of systemic risk and how interconnected financial institutions are. After the 2008 financial crisis, stress testing became mandatory for large banks worldwide. This was driven by the need for banks to show they could weather extreme financial storms.

The 2008 crisis underscored the importance of robust stress testing. Undercapitalized banks struggled to cover losses from devalued mortgages, which led to severe economic fallout. Today, regulators like the Federal Reserve, the European Banking Authority, and the International Monetary Fund require regular stress tests. This ensures banks have enough capital to absorb potential losses in tough times. Learn more about the stress testing evolution.

The Modern Stress Testing Landscape

Today’s stress tests are characterized by sophisticated frameworks and strict regulatory oversight. These frameworks incorporate various scenarios, from moderate downturns to severe global recessions, preparing banks for a range of economic challenges.

For example, regulators often use hypothetical scenarios with large declines in GDP, increased unemployment, and stressed markets. These scenarios help assess a bank’s vulnerability to macroeconomic shocks. Modern stress testing has also expanded beyond just assessing capital adequacy.

It now evaluates a bank's ability to manage liquidity, credit risk, and operational risks under pressure. This holistic approach provides a more complete view of a bank's resilience. These advancements highlight the critical role of stress testing in maintaining the stability and integrity of the global financial system.

This means banks must constantly adapt their stress testing methods to stay ahead of evolving risks and regulatory expectations. This constant change emphasizes the dynamic nature of stress testing in today’s financial world.

Mastering Stress Testing Methodologies That Actually Work

Stress testing is essential for evaluating a bank's financial resilience. Understanding the core methodologies is key for any financial institution. These tests go beyond basic capital requirements and assess a bank's ability to weather economic downturns. A historical perspective can provide helpful context. For a deeper dive into this history, check out the evolution of accounting practices.

Top-Down Vs. Bottom-Up Approaches

There are two main approaches to stress testing: top-down and bottom-up.

The top-down approach, frequently used by regulators, applies standardized scenarios across various banks. This allows for comparisons and a system-wide view of the financial sector's health.

However, this approach may not fully capture individual banks' unique risk profiles. It can also oversimplify the complex relationships within a bank's portfolio. Therefore, combining this method with more granular approaches is important.

The bottom-up approach, on the other hand, allows banks to tailor scenarios to their specific business models and risk exposures. This offers a more detailed and customized assessment. For instance, a bank heavily invested in commercial real estate could model a scenario with falling property values.

This targeted approach reveals potential vulnerabilities. However, it demands considerable internal resources and expertise. Smaller banks might struggle to implement this granular approach effectively.

Integrating Emerging Risks

Modern stress testing needs to incorporate more than traditional financial risks.

Leading banks are now including emerging risks like climate change and cybersecurity in their frameworks. This recognizes the significant financial implications of these risks.

Climate-related events can disrupt operations and affect loan portfolios. A major cyberattack could cause substantial financial losses and damage a bank's reputation. Ignoring these risks puts banks at a disadvantage.

This proactive approach demonstrates a commitment to long-term stability. It is also critical for maintaining trust with stakeholders and meeting regulatory expectations. These expectations continually evolve, encouraging banks to adopt more dynamic and comprehensive stress testing methods.

To understand the nuances of different stress testing approaches, refer to the comparison table below:

Introduction to the table: The following table provides a comparison of various stress testing methodologies, outlining their key features, advantages, limitations, and typical applications within the banking industry.

| Methodology | Key Features | Advantages | Limitations | Typical Applications |

|---|---|---|---|---|

| Top-Down | Standardized scenarios applied across multiple banks | Allows for comparison and systemic view | May not capture unique risk profiles; can oversimplify complex relationships | Regulatory assessments, industry-wide analysis |

| Bottom-Up | Tailored scenarios specific to individual bank's business model and risk exposures | Provides detailed and customized assessment | Requires significant internal resources and expertise | Internal risk management, capital planning |

| Hybrid | Combines elements of top-down and bottom-up approaches | Balances standardization with customization | Can be complex to implement | Comprehensive risk assessments |

| Reverse Stress Testing | Identifies scenarios that could lead to failure | Helps pinpoint vulnerabilities | Requires sophisticated modeling techniques | Capital planning, risk mitigation |

| Sensitivity Analysis | Examines the impact of changing individual variables | Easy to understand and implement | Doesn't consider interactions between variables | Preliminary risk assessment, identifying key risk drivers |

Key Insights from the Table: As the table illustrates, each methodology has its strengths and weaknesses. Choosing the right approach depends on the specific needs and resources of the bank. A hybrid approach often provides the most comprehensive view by combining the benefits of both top-down and bottom-up methodologies.

Navigating the Global Regulatory Landscape With Confidence

The world of stress testing for banks presents a complex network of global regulations. These regulations differ significantly across various jurisdictions. This includes understanding the specific requirements of institutions like the Federal Reserve, the European Banking Authority, and the Bank of England. Successfully managing these diverse requirements involves strategic planning and efficient resource allocation.

Key Regulatory Frameworks

The Federal Reserve's Comprehensive Capital Analysis and Review (CCAR) in the United States represents a thorough assessment of a bank's capital planning processes. Similarly, the European Banking Authority (EBA) conducts regular stress tests to evaluate the resilience of European banks. The Bank of England employs its own distinct stress test scenarios. These scenarios reflect the specific characteristics of the UK financial system. Managing these varied requirements efficiently is crucial for international banks. You might also find this helpful: How to master regulatory compliance.

This efficient management involves avoiding duplicated effort and improving reporting processes. For example, a bank operating in multiple jurisdictions needs a flexible framework. This framework should adapt to different regulatory requirements without needless repetition.

Disclosure Practices and Stakeholder Confidence

Transparency and effective communication are key to building trust with stakeholders. Clear and concise disclosure practices are essential. These practices demonstrate a bank's commitment to sound risk management.

They also reassure investors and customers. This reassurance builds confidence in the bank's ability to handle challenging economic conditions. However, simply meeting the minimum regulatory standards is often not enough. Leading banks aim to exceed these minimums. This demonstrates their strong commitment to robust financial health.

Staying ahead of upcoming regulatory changes is also critical. This helps maintain compliance and avoid penalties. This proactive approach involves monitoring regulatory developments. It also means adapting internal processes as needed.

For example, incorporating emerging risks into stress testing models is becoming increasingly important. One example of these emerging risks is climate change. This proactive integration is crucial for maintaining long-term resilience.

Global Perspectives on Stress Testing

The increasing interconnectedness of the global financial system highlights the importance of international cooperation. This is especially true when it comes to stress testing. The first global bank stress test, conducted in 2022, analyzed data from 257 banks spanning over two and a half decades. This landmark assessment revealed improved financial resilience in the banking sector. Discover more insights about global stress tests.

This global approach offers valuable insights for both regulators and banks. It helps them prepare for future economic challenges. It achieves this by identifying vulnerabilities and improving risk management practices. These improvements apply across international markets. Understanding and responding to evolving international standards are essential for global banks.

Inside the Fed's CCAR: Lessons From Banking's Ultimate Test

The Federal Reserve's Comprehensive Capital Analysis and Review (CCAR) stress tests are considered the gold standard for assessing bank resilience. These tests push banks to their limits, simulating severe hypothetical economic downturns to evaluate their ability to withstand financial shocks. This intensive process ensures regulatory compliance and provides valuable insights that banks can use to improve internal risk management. Learn more in our article about the Fed's 2023 stress test scenarios.

Analyzing Real Results: Who Thrives and Who Falters

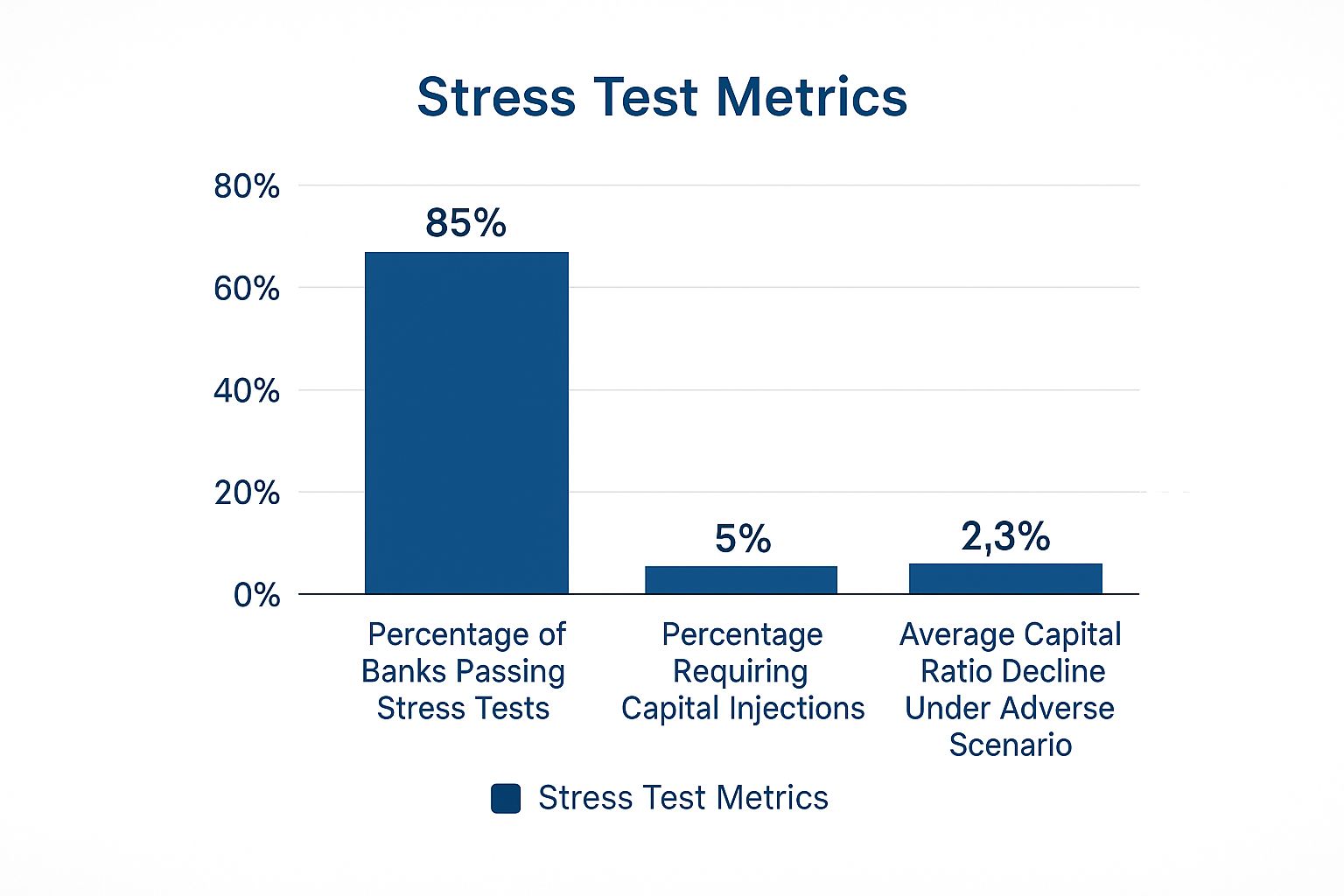

Analyzing results from recent CCAR exercises reveals a divide between thriving and faltering institutions. Some consistently demonstrate robust capital planning and risk identification, while others struggle to meet minimum requirements. This divergence highlights varying preparedness levels within the banking industry. The infographic below visualizes three key stress test metrics: the percentage of banks passing stress tests, the percentage requiring capital injections, and the average capital ratio decline under an adverse scenario.

As the infographic shows, while most banks pass stress tests, a small percentage still require capital injections and experience declining capital ratios under adverse conditions. This reinforces the need for constant improvement and adaptation in stress testing methodologies.

The following table presents key statistics from recent CCAR stress tests, including projected losses by loan category, capital impact, and performance metrics across participating banks.

Results of Recent Federal Reserve Stress Tests

| Year | Number of Banks | Scenario Severity | Total Projected Losses | CET1 Capital Impact | Failure Rate |

|---|---|---|---|---|---|

| 2023 | 23 | Severe Global Recession | $541 Billion | Remained above minimum requirements | 0% |

The 2023 stress test simulated a severe global recession with a 40% decline in commercial real estate prices and a 38% decline in house prices. Despite these conditions, all 23 tested banks remained above their minimum capital requirements. The test projected total losses of $541 billion, including significant losses from commercial real estate and residential mortgages. These results highlight the robustness of major U.S. banks. Find more detailed statistics here.

Transforming Weaknesses Into Strengths

Leading banks treat CCAR as a strategic opportunity. They use insights from these tests to identify and address weaknesses in their capital planning. This proactive approach strengthens overall risk management frameworks. It also optimizes capital allocation and improves preparedness for future economic uncertainties.

Additionally, these institutions recognize the importance of robust risk identification capabilities. These go beyond simple CCAR compliance, providing valuable information for better strategic decisions.

Learning From Top Performers

By studying top-performing banks in CCAR exercises, other institutions can gain valuable knowledge. These top performers often implement best practices in data management, model development, and scenario design. They also emphasize communication and transparency in their stress testing processes.

This focus on best practices helps identify potential vulnerabilities early and develop effective mitigation strategies. It also enables them to communicate their resilience to regulators and investors, fostering trust and confidence. Read also: Mastering Stress Testing.

Building Your Stress Testing Program: From Theory to Practice

A robust stress testing program is more than just checking a regulatory box. It's a critical tool for navigating economic uncertainty and ensuring your institution's stability for the long haul. Building a successful program requires a shift from theory to practical application, focusing on key areas like governance, data, and validation. This means moving beyond simply meeting the minimum requirements and building a program that offers real, actionable business insights.

Establishing Strong Governance Structures

Effective stress testing hinges on a solid governance framework. This includes clearly defined roles and responsibilities, robust reporting procedures, and a culture of open communication. This framework ensures accountability and promotes transparency throughout the entire process. For instance, a dedicated stress testing committee can oversee the program's development and execution, making sure it aligns with the bank's overall risk management strategy. This emphasis on accountability ensures potential vulnerabilities are addressed proactively. Check out our guide on How to master financial risk management strategies.

Regular reporting to senior management and the board of directors is also essential. This provides visibility into the bank's stress testing activities and empowers informed decision-making. Clear communication like this helps integrate stress testing insights into strategic planning.

Managing Data and Model Risk

High-quality data is the bedrock of accurate stress testing. Banks need comprehensive datasets that cover diverse portfolios and risk exposures. This requires robust data management processes to ensure data accuracy and completeness. For example, implementing data quality checks and validation procedures can help minimize errors and maintain consistency.

Furthermore, effective model risk management is crucial. This involves thoroughly validating and calibrating stress testing models to ensure they accurately reflect real-world economic conditions. It also includes considering the limitations of models and incorporating expert judgment where necessary.

Designing Effective Scenarios

Stress testing scenarios should reflect a range of potential economic shocks, from minor dips to major recessions. Leading institutions design scenarios that balance regulatory requirements with practical business insights. This means tailoring scenarios to the bank's unique risk profile and specific business model. This targeted approach provides a much more accurate assessment of potential vulnerabilities. For example, a bank with significant exposure to a particular industry should incorporate scenarios that reflect potential downturns in that sector.

Leveraging Automation for Efficiency

Automation can dramatically reduce the operational burden of stress testing. This frees up valuable resources for more in-depth analysis and interpretation. Many banks are adopting automated tools for data processing, model execution, and report generation. This not only boosts efficiency but also minimizes the risk of human error. Furthermore, automation allows for more frequent and granular stress testing, enabling banks to respond more quickly to changing market conditions. This increased agility is essential in today's dynamic financial world.

Beyond Compliance: Turning Stress Tests Into Strategic Assets

Stress testing for banks has changed significantly. It's no longer just a checkbox for regulators. Forward-thinking institutions are using stress test insights to gain a competitive edge. This means using the data not just for compliance, but for strategic decision-making.

From Reactive to Proactive: Using Stress Tests for Strategic Advantage

Sophisticated banks are using stress tests to inform capital allocation. For example, by identifying vulnerabilities in specific portfolios under different economic scenarios, banks can optimize their capital reserves. This ensures sufficient capital where it's needed most, avoiding over-allocation in less vulnerable areas. This proactive approach to resource management helps maintain profitability during uncertain economic times.

Banks are also using stress tests to refine their risk appetites. By understanding how different risks impact the bank under stress, institutions can make more informed decisions about acceptable risk levels. This leads to a more defined and robust risk management framework, better aligning risk tolerance with overall business strategy.

Furthermore, stress tests can reveal emerging opportunities. Analyzing the impact of various economic scenarios helps banks anticipate market trends and identify potential growth areas. This allows them to position themselves strategically and capitalize on opportunities before competitors. This forward-thinking approach transforms stress testing from a defensive measure into an offensive tool for business development.

Integrated Frameworks: Transforming Decision-Making

Integrated stress testing frameworks are changing how banks operate. These frameworks are embedded throughout the organization, from the board level to front-line management, ensuring a unified approach to risk assessment and enabling more informed, coordinated decision-making.

Stress test insights can inform lending decisions, pricing strategies, and product development. They can also be used for portfolio optimization and strategic investment planning. This comprehensive integration of stress testing data creates a more agile and resilient institution, allowing banks to react effectively to shifting markets.

Communicating Results: Building Trust and Transparency

Communicating stress test results effectively builds trust with stakeholders. Banks must convey complex information clearly to a diverse audience, including investors, customers, and regulators. This includes outlining the bank's stress testing methodology and explaining the results in a straightforward manner.

Different stakeholders have varying levels of financial expertise. Banks must tailor their communication strategies to ensure everyone understands the information. This transparency can ease anxieties, build confidence, attract investment, and improve standing with regulators.

Preparing for the Future: Evolving Stress Testing Practices

Leading banks are preparing for the next evolution of stress testing. This includes integrating climate risk into their frameworks and enhancing their focus on operational resilience. This means moving beyond financial risks and incorporating more complex factors. For instance, climate change impacts asset values, necessitating robust climate risk models.

This integration of broader risk factors reflects the evolving financial landscape and underscores the importance of staying ahead of emerging trends. This proactive approach positions banks for long-term success in a rapidly changing world.

Ready to transform your bank's stress testing program from a compliance exercise to a strategic asset? Explore how Visbanking can help you gain a competitive edge through data-driven insights.

Latest Articles

Brian's Banking Blog

Alternative Investment Jobs: A Guide for Bank Executives

Brian's Banking Blog

Investor Relations Associate: A Strategic Banking Asset

Brian's Banking Blog

Customer Service Survey: A Guide for Bank Executives

Brian's Banking Blog

Dun Number Registration: Banking Executive's 2026 Guide

Brian's Banking Blog

Equity and Debt Financing: A Banker's Decision Guide

Brian's Banking Blog