7 Largest Regional Banks: A Data-Driven Analysis for 2025

Brian's Banking Blog

In the current economic climate, the title of 'largest' is a moving target. For bank executives and directors, true strategic advantage lies not in static rankings but in understanding the underlying drivers of performance, efficiency, and market capture among top-tier institutions. This analysis moves beyond surface-level asset totals to dissect the operational DNA of the largest regional banks. We will examine critical performance indicators, such as net interest margin (NIM), efficiency ratios, loan growth, and deposit composition, to reveal the data-driven strategies separating leaders from the pack.

This roundup provides an actionable framework for benchmarking your institution against key players, including PNC Bank, U.S. Bank, and Truist. Each profile will dissect specific strategic choices and their quantifiable outcomes, such as how one bank’s targeted loan origination in high-growth sectors boosted its NIM by 15 basis points while a competitor struggled with deposit flight.

The insights presented are designed to be immediately applicable, demonstrating how a granular understanding of peer performance, powered by a comprehensive bank intelligence system like Visbanking, enables your institution to benchmark effectively. Use this analysis to identify competitive opportunities, refine your own strategies, and execute decisions with greater precision and confidence.

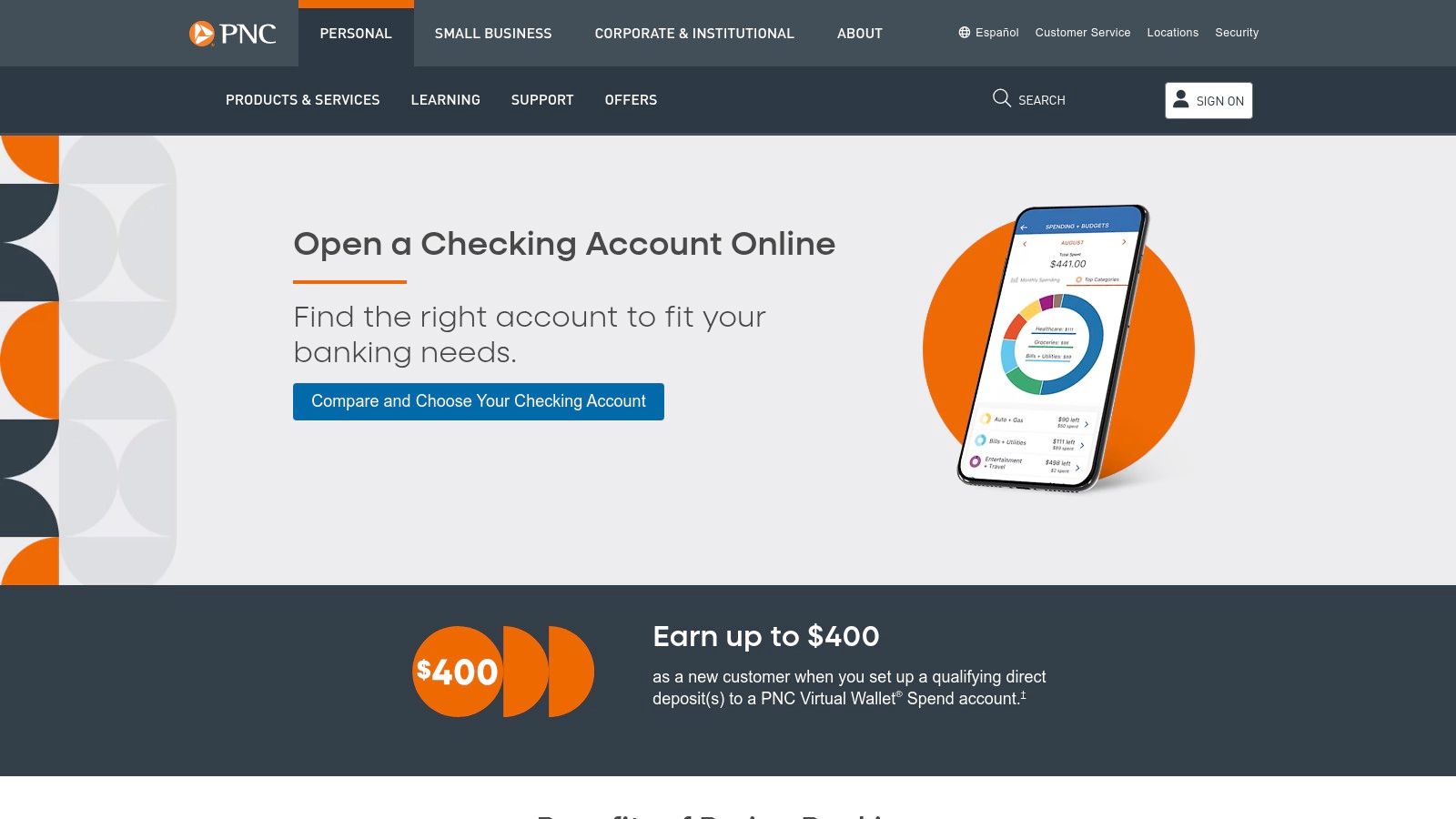

1. PNC Bank: The Digital Juggernaut Redefining Customer Engagement

PNC’s consistent performance is anchored by its early and aggressive investment in digital infrastructure. Analysis of their call report data reveals a lower-than-peer non-interest expense ratio, a direct result of efficiencies gained from platforms like its signature Virtual Wallet. For executives at other large regional banks, the critical insight is how PNC’s digital integration directly impacts the bottom line.

This isn't just about features; it's about a data-proven link between digital customer experience and superior financial performance. PNC’s strategy demonstrates that investment in technology is not a cost center, but a primary driver of margin and efficiency.

Actionable Insight: Modeling Digital Efficiency

A competing regional bank with a similar asset size (e.g., ~$600B) might show a 5% higher efficiency ratio. Using a platform like Visbanking to model the impact of adopting a similar digital-first deposit acquisition strategy, a bank could project a potential $150 million annual reduction in operating costs. This is achieved by reducing branch transaction dependency and automating low-value service interactions.

Key Features and Strategic Impact

PNC’s Virtual Wallet is more than a checking account; it's an ecosystem designed to drive customer loyalty and reduce service costs.

- Integrated Accounts: Bundles Spend (checking), Reserve (short-term savings), and Growth (long-term savings) with built-in money management tools.

- Intelligent Alerts: Features like Calendar view and Low Cash Mode proactively alert customers, reducing overdraft incidents and the associated customer service burden.

- Transparent Fee Structures: The platform clearly displays monthly charge rules and multiple waiver options, such as minimum balances or direct deposit amounts, enhancing customer trust and reducing disputes.

Key Takeaway: PNC's digital suite successfully merges customer-centric tools with operational efficiency. By automating budgeting and providing financial clarity, PNC builds stickier relationships while lowering its cost-to-serve ratio, a powerful combination for any of the largest regional banks aiming for market leadership.

For more information, visit the PNC Virtual Wallet overview page.

2. U.S. Bank: Mastering Accessible Banking at Scale

U.S. Bank’s strategy demonstrates how one of the largest regional banks can effectively combine a massive physical footprint with an exceptionally low-friction digital onboarding process. Their approach prioritizes accessibility, proven by a low $25 minimum opening deposit for their flagship Bank Smartly Checking. For banking executives, this model shows how to capture a broad customer base, from students to seniors, without sacrificing the efficiency of digital channels.

This isn't just about offering a low entry point; it's a calculated strategy to grow core deposits by removing barriers. U.S. Bank’s performance, especially following its significant acquisition of MUFG Union Bank, underscores the power of a streamlined, highly accessible customer acquisition engine. For more on this, you can read about the U.S. Bank community benefits plan.

Actionable Insight: Analyzing Low-Barrier Deposit Growth

A competing bank with a higher average opening deposit requirement (e.g., $100) and a more complex onboarding process might see lower new account velocity. By modeling the financial impact with Visbanking, that bank could project a 15% increase in new-to-bank checking relationships over two quarters by adopting a similar low-deposit, digital-first strategy. This approach directly translates into faster core deposit growth and a lower aggregate cost of funds.

Key Features and Strategic Impact

U.S. Bank’s checking platform is designed for mass-market appeal, focusing on simplicity and essential digital tools that drive adoption and reduce operational strain.

- Ultra-Low Entry Barrier: A $25 minimum opening deposit significantly lowers the hurdle for new customers, maximizing the top of the acquisition funnel.

- Segmented Benefits: Offers customized perks and fee waiver structures for specific demographics like students, military members, and seniors, allowing for targeted marketing and relationship deepening.

- Comprehensive Digital Suite: Standard features like Zelle, mobile deposit, and bill pay are seamlessly integrated, ensuring customers can self-serve for most daily transactions, which in turn reduces branch and call center traffic.

Key Takeaway: U.S. Bank proves that accessibility and scale are not mutually exclusive. By minimizing friction in the account opening process and providing essential digital tools, it effectively captures a wide demographic spectrum, fueling low-cost deposit growth and solidifying its position among the largest regional banks in the nation.

For more information, visit the U.S. Bank Checking Accounts page.

3. Truist: Engineering Overdraft Forgiveness into the Core Product

The merger of BB&T and SunTrust created Truist, a formidable player among the largest regional banks, and its product strategy reflects a deliberate move to address a major customer pain point: overdraft fees. Analysis of peer call reports often highlights non-interest income from service charges as a significant revenue line. Truist’s approach with its flagship Truist One Checking account directly challenges this model.

This isn't merely a marketing gimmick; it's a strategic decision to trade short-term fee revenue for long-term primary-bank relationships and higher customer lifetime value. For executives at competing institutions, Truist provides a powerful case study in embedding customer-centric policies directly into product design to gain a competitive advantage.

Actionable Insight: Quantifying the Impact of Fee Elimination

A competing regional bank with a similar deposit base (e.g., ~$470B) might generate $50 million annually from consumer checking overdraft fees. Using a platform like Visbanking to model customer retention and acquisition, the bank could project that eliminating these fees might lead to a 5% increase in primary checking account holders within 24 months. This shift could offset the initial revenue loss through increased loan and investment product cross-sells, demonstrating a data-backed path to sustainable, relationship-driven growth.

Key Features and Strategic Impact

Truist One Checking is built around simplicity and fee avoidance, directly targeting a core source of customer dissatisfaction and operational friction.

- No Overdraft Fees: The account's core feature, which fundamentally changes the risk-reward calculation for customers and reduces the service costs associated with fee disputes.

- Balance Buffer: Eligible clients receive a buffer (e.g., $100) that allows them to overdraw their account up to that amount without penalty, a feature that builds significant goodwill.

- Simple Waiver Requirements: The monthly maintenance fee is waived with straightforward actions like a single $500 direct deposit, making it accessible to a broad customer base and lowering barriers to entry.

Key Takeaway: Truist's strategy proves that core banking products can be redesigned to eliminate historical friction points. By removing overdraft fees, Truist attracts and retains deposit relationships that are less transactional and more deeply integrated, positioning itself as a primary financial partner rather than just another service provider.

For more information, visit the Truist checking accounts page.

4. Citizens Bank: Streamlining Deposit Products for Mass Market Appeal

Citizens Bank has carved out a strong position among the largest regional banks by simplifying its core deposit offerings to directly address common consumer pain points: monthly fees and overdraft penalties. Analysis of their product strategy shows a deliberate move away from complex, tiered accounts toward straightforward, transparent options like One Deposit Checking and EverValue Checking. This approach is designed to attract and retain a broad customer base by offering clear, achievable value.

For banking executives, the key lesson is how Citizens leverages product simplicity as a competitive advantage. This strategy minimizes customer confusion, reduces service calls related to fee disputes, and creates a powerful marketing message that resonates with fee-sensitive consumers.

Actionable Insight: Modeling Low-Complexity Product Impact

A competitor with a complex array of checking accounts might see higher-than-average account attrition rates. By using a platform like Visbanking to model the adoption of a simplified product suite like Citizens', a bank could project a 5-7% reduction in annual customer churn. This is achieved by removing friction in the customer journey and aligning products with transparent, easily understood benefits, which directly boosts lifetime customer value.

Key Features and Strategic Impact

Citizens' checking lineup is built on simplicity and customer-friendly features that drive both acquisition and loyalty while managing risk.

- One Deposit Checking: Its primary feature is waiving the $9.99 monthly fee with just one deposit of any amount per statement period, a low barrier that appeals to a wide demographic.

- EverValue Checking: This account offers a no-overdraft-fee structure for a flat $5 monthly fee, directly targeting consumers who prioritize overdraft protection and predictable costs.

- Paid Early Feature: Allows customers with direct deposit to access their paychecks up to two days early, a high-value feature that encourages primary banking relationships.

Key Takeaway: Citizens Bank proves that product innovation doesn't have to be technologically complex. By focusing on simple, transparent fee structures and eliminating common financial stressors like overdrafts, it builds a loyal deposit base. This approach demonstrates how strategic product design can be a powerful and cost-effective growth engine.

For more information, visit the Citizens Bank One Deposit Checking page.

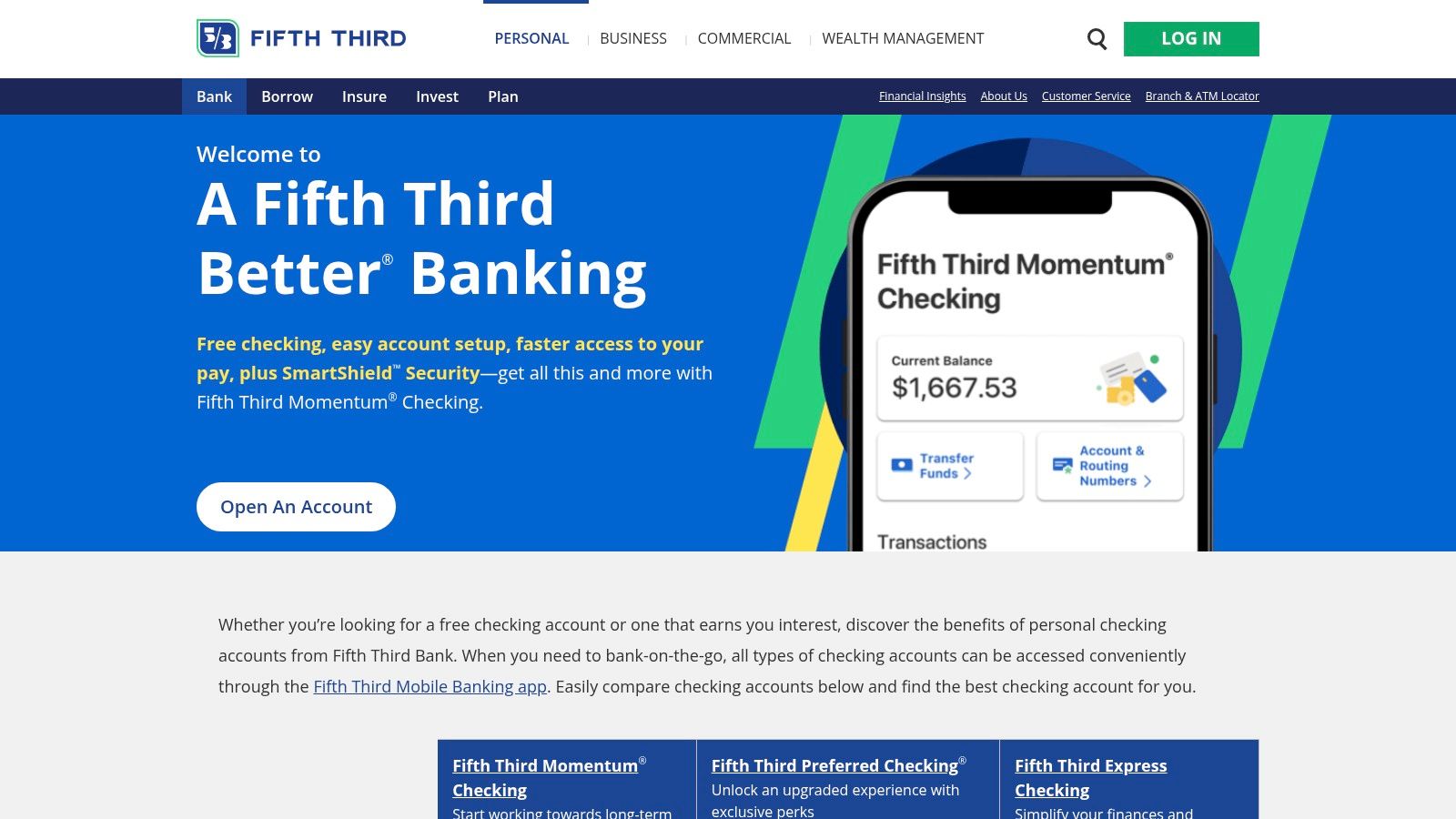

5. Fifth Third Bank: Mastering Fee-Free Accessibility to Capture Market Share

Fifth Third Bank has strategically positioned its Momentum Checking account as a powerful customer acquisition tool, directly challenging the fee-heavy models of many competitors. By eliminating monthly maintenance fees, minimum balance requirements, and even opening deposit minimums, they have removed the primary friction points for mass-market consumers. This approach is a calculated play for deposit growth, prioritizing volume and long-term customer value over immediate fee income.

For executives at other regional banks, Fifth Third’s model demonstrates a successful pivot from traditional revenue streams to a strategy based on scale and digital engagement. The low-cost account structure is supported by an efficient digital platform and a vast fee-free ATM network, minimizing the operational drag typically associated with high-volume, low-balance accounts.

Actionable Insight: Quantifying the Impact of Fee Elimination

A competing regional bank might generate $20 million annually from maintenance fees on basic checking accounts. While this seems like significant revenue, analysis often reveals a high customer churn rate and acquisition cost associated with these accounts. By modeling a shift to a fee-free structure like Momentum Checking, a bank could project a 15% increase in new deposit account openings and a subsequent 10% lift in cross-sell opportunities for higher-margin products like auto loans and mortgages within the first 24 months. The long-term household value can far exceed the sacrificed fee revenue.

Key Features and Strategic Impact

Fifth Third's value proposition is built on simplicity and accessibility, designed to attract and retain a broad customer base.

- Momentum Checking: The core offering is truly free, with a $0 monthly fee, no minimum balance, and no minimum opening deposit required, making it highly competitive.

- Early Pay & Overdraft Tools: Features like receiving direct deposits up to two days early, "Extra Time" to avoid overdrafts, and "MyAdvance" for small-dollar loans directly address key consumer pain points.

- Expansive ATM Network: Access to over 40,000 partner ATMs without fees is a critical feature that extends Fifth Third's physical reach far beyond its Midwestern and Southeastern branch footprint.

Key Takeaway: Fifth Third proves that a "free" checking account can be a potent strategic weapon for growth among the largest regional banks. By focusing on removing barriers and solving everyday financial needs, they build a wide funnel for new customers, creating future opportunities for more profitable relationships. This strategy is essential for any institution looking to compete for market share in a crowded digital landscape.

For a deeper analysis, explore the data behind Fifth Third Bank's growth strategy.

6. KeyBank: Monetizing Deposit Relationships Through Strategic Incentives

KeyBank excels at using a multi-tiered checking account structure to attract and segment customers, directly tying product features to relationship depth. Their digital platform clearly articulates the value proposition for each account, from the no-fee Key Smart Checking to the interest-bearing Key Select account with its cash bonus. For executives at competing regional banks, this strategy provides a masterclass in using transparent incentives to drive specific customer behaviors and increase deposit stability.

This approach is more than just marketing; it's a data-informed strategy to optimize the cost of funds. By offering tangible rewards like cash bonuses for deeper deposit relationships, KeyBank effectively reduces its reliance on higher-cost promotional CDs or money market specials, a crucial advantage in a competitive rate environment.

Actionable Insight: Modeling the Impact of Tiered Incentives

A competing bank with a high concentration of low-balance, non-relationship checking accounts could see its net interest margin compress. Using a platform like Visbanking to analyze deposit-tier performance, that bank could model a KeyBank-style incentive program. Projecting an upgrade of just 15% of its basic checking households to a premium, relationship-based account could generate an estimated $50 million in additional low-cost core deposits and reduce customer attrition by 3-4% annually.

Key Features and Strategic Impact

KeyBank's digital account opening process and product suite are engineered to convert prospects and deepen relationships through clear, tiered benefits.

- Key Select Checking: Offers a $100 annual cash bonus for qualifying direct deposits, directly rewarding customers for making KeyBank their primary financial institution.

- EasyUp Automatic Savings: This feature rounds up debit card purchases to the nearest dollar and transfers the difference to savings, creating a frictionless way for customers to build balances, which in turn provides a stable, low-cost funding source for the bank.

- Transparent Digital Access: The website clearly outlines bonus criteria, fee schedules, and APY tiers by market, reducing ambiguity and minimizing customer service inquiries related to product terms.

Key Takeaway: KeyBank demonstrates how to structure and market deposit products as a strategic tool for relationship banking. By transparently rewarding desired behaviors like direct deposits and higher balances, they build a more profitable and loyal customer base, a core objective for any of the largest regional banks aiming for sustainable growth.

For more information, visit the KeyBank checking account options page.

7. Regions Bank: Mastering Fee Transparency and Customer Choice

Regions Bank has carved out a strong position among the largest regional banks by offering a diversified product suite that directly addresses consumer demand for fee transparency and flexibility. Their approach isn't just about providing options; it's a strategic move to capture distinct customer segments, from those seeking full-service banking to those prioritizing overdraft avoidance, thereby reducing customer attrition linked to fee dissatisfaction.

This strategy of clear segmentation and transparent fee structures is a powerful tool for customer acquisition and retention. For executives at competing banks, Regions provides a model for how to structure a product lineup that minimizes fee-related friction while still generating sustainable non-interest income.

Actionable Insight: Analyzing Fee Sensitivity and Product Profitability

A competing bank with a concentrated Southeast footprint might see an above-average attrition rate of 12% in its core checking portfolio, often linked to overdraft fees. Using a platform like Visbanking to analyze peer performance, executives could model the impact of introducing a product similar to Regions' Now Checking. The analysis might project a 3% reduction in customer churn, preserving low-cost deposits and saving an estimated $50 million in annual acquisition costs needed to replace those lost customers.

Key Features and Strategic Impact

Regions’ consumer checking lineup is designed to provide clear pathways for customers to control their banking costs, enhancing trust and loyalty.

- Segmented Account Options: Offers multiple checking accounts, including LifeGreen for traditional banking, Preferred for relationship benefits, and the innovative Now Checking account, which eliminates overdraft fees entirely.

- Early Pay Feature: Provides automatic access to direct deposits up to two days early without requiring enrollment, a high-demand feature that increases account stickiness.

- Transparent Fee Waivers: Each account has clearly defined rules for waiving monthly fees, such as minimum balances or direct deposit requirements, which are prominently displayed during the online account opening process.

Key Takeaway: Regions Bank’s strength lies in its explicit commitment to customer choice regarding fees. By offering products like Now Checking and features like Early Pay, Regions directly addresses major consumer pain points, creating a more resilient and loyal deposit base that is less sensitive to market-wide rate fluctuations.

For more information, visit the Regions Bank account opening page.

Top 7 Regional Banks Comparison

| Bank | 🔄 Implementation Complexity | ⚡ Resource Requirements | 📊 Expected Outcomes | 💡 Ideal Use Cases | ⭐ Key Advantages |

|---|---|---|---|---|---|

| PNC Bank | Moderate | Moderate (tiered accounts, digital tools) | Good budgeting and savings control | Users wanting integrated digital money management | Robust budgeting tools, multiple fee-waiver options |

| U.S. Bank | Low | Low (simple deposit, broad network) | Wide access and convenience | Customers needing low deposit and broad ATM access | Low minimum opening deposit, extensive network |

| Truist | Low-Moderate | Moderate (fee waivers, overdraft buffer) | Fee savings, overdraft protection | Overdraft-avoidant users in Southeast/Mid-Atlantic | No overdraft fees, clear fee waiver criteria |

| Citizens Bank | Low | Low (simple fee waivers, limited regions) | Ease of fee waivers and overdraft relief | Northeast/Mid-Atlantic customers seeking simplicity | Simple deposit fee waiver, overdraft-fee-free option |

| Fifth Third Bank | Low | Low (free checking, large ATM network) | Cost savings, convenience | Users wanting no-fee accounts with large ATM access | Truly free checking, very large fee-free ATM network |

| KeyBank | Moderate | Moderate (bonus accounts, overdraft) | Interest earnings plus fee savings | Regional users seeking interest and bonuses | Interest-bearing accounts with bonuses, clear fees |

| Regions Bank | Moderate | Moderate (multiple accounts, early pay) | Flexible fee waivers and early deposits | Southeastern users needing variety and digital help | Multiple fee waiver methods, early direct deposit |

From Insight to Action: Activating Your Bank's Competitive Intelligence

This analysis of the largest regional banks reveals a clear imperative: data-driven decision-making is the cornerstone of sustained success. These institutions do not operate on intuition. Their growth, efficiency, and market positioning are the direct results of a culture that prioritizes rigorous, continuous competitive intelligence.

The strategies of these leaders are quantifiable actions rooted in precise performance metrics. Whether it is Fifth Third Bank optimizing its loan-to-deposit ratio or PNC leveraging digital engagement to lower its efficiency ratio, every move is informed by a deep understanding of their own performance relative to the competitive landscape. This level of clarity is no longer an exclusive advantage for the top tier.

From Data Points to Strategic Imperatives

The insights from these banking giants provide a clear roadmap for any institution. The critical takeaway is that comprehensive data empowers leadership to move from reactive analysis to proactive, strategic execution. Simply knowing your asset size is surface-level information; understanding how your asset utilization, net interest margin, and efficiency ratio compare to a curated peer group is actionable intelligence.

Consider a mid-sized regional bank aiming to improve its profitability. Instead of broad cost-cutting initiatives, a data-driven approach allows for surgical precision. By benchmarking its noninterest expenses against a peer group of similar-sized banks in its primary markets, the leadership team might discover its technology spend is 15% higher than the peer average, while its return on assets is 10 basis points lower. This specific insight transforms a vague goal ("improve efficiency") into a targeted strategic question: "Are we achieving a sufficient return on our technology investment, or is there an opportunity to reallocate capital or renegotiate vendor contracts?"

Activating Your Competitive Edge

Translating this intelligence into action requires a structured approach. Your institution can begin by focusing on these key steps:

- Establish Your True Peer Group: Move beyond generic asset-based comparisons. Use granular data to build a peer set that reflects your specific business model, geographic footprint, and strategic goals. This ensures your benchmarks are relevant and your targets are realistic.

- Identify Key Performance Gaps: Conduct a thorough analysis comparing your institution against this peer group across critical metrics like loan growth, deposit composition, and risk-adjusted returns. Isolate the 2-3 areas with the most significant performance gaps.

- Connect Metrics to Operations: Drill down into the operational drivers behind the data. If your net interest margin is lagging, is the cause a less favorable loan mix, higher funding costs, or a combination of both? This connection is vital for developing effective tactical responses.

- Empower Your Board with Clarity: Present data in a clear, contextualized format. Instead of just showing raw numbers, illustrate trends over time and performance against your defined peer group. This enables your board to move beyond simple oversight and engage in strategic, forward-looking guidance.

The success of the largest regional banks underscores that superior performance is a direct result of superior intelligence. The tools and data are now accessible, leveling the playing field and empowering leadership teams to act with the same confidence and precision as the industry's top players.

The strategies of these leading institutions are not secrets; they are written in the data. With the Visbanking Bank Intelligence and Action System (BIAS), you can stop guessing how you stack up and start knowing. Benchmark your performance against any peer group, identify market opportunities with precision, and transform your decision-making process by visiting Visbanking today.

Latest Articles

Brian's Banking Blog

Social Network Analysis for Banking: A Practical Guide

Brian's Banking Blog

How to Increase ROE: A Data-Driven Playbook for Bank Leaders

Brian's Banking Blog

What Is SEC EDGAR and How Banks Use the Data

Brian's Banking Blog

What Is Value at Risk and Why Bank Leaders Rely on It

Brian's Banking Blog

How to Build a Leadership Pipeline for Banks

Brian's Banking Blog