How to Conduct Risk Assessments in Banking

Brian's Banking Blog

A rigorous risk assessment is no longer a compliance exercise; it is a core driver of strategic decision-making. For banking executives, the objective is to move beyond static checklists and embed a dynamic, data-centric process that identifies potential threats, quantifies their financial and reputational impact, and builds intelligent mitigation strategies backed by hard numbers. This is how raw data is converted into strategic foresight, empowering leadership to act with conviction.

Why Data-Driven Risk Assessments Are No Longer Optional

In the current financial climate, clinging to traditional, compliance-focused risk assessments is a significant liability. Checklist-based methods cannot keep pace with the velocity and complexity of modern threats, from sophisticated cyberattacks to abrupt economic shifts. For bank executives and directors, relying on outdated processes is not merely inefficient—it is a direct threat to the institution's stability and growth.

The fundamental challenge is that risk is no longer linear or predictable; it is a web of interconnected, dynamic variables. A single geopolitical event can trigger market volatility that immediately stresses commercial loan portfolios. A new digital banking feature, while boosting customer engagement, simultaneously opens new vectors for fraud. A data-driven approach is the only rational method for managing this complexity.

From Hindsight to Foresight

This shift transforms risk management from a reactive, historical function to a proactive, forward-looking strategic capability.

Consider a practical scenario. A mid-sized community bank, leveraging granular data analysis, identified a growing concentration risk in its commercial real estate (CRE) portfolio, specifically within the retail sector.

Traditional methods would have flagged this risk only after delinquency rates began to climb. However, by analyzing market data, tenant occupancy rates, and local economic forecasts, the bank's leadership identified the emerging weakness months before the broader market downturn. This was not an intuitive guess; it was a conclusion drawn from quantifiable data points.

This foresight enabled the board to execute several decisive strategic moves:

- They immediately tightened underwriting standards for new retail CRE loans.

- They initiated a rebalancing of the portfolio, shifting focus toward more resilient sectors.

- They proactively engaged existing borrowers in the at-risk segment to assess their financial health.

The result: This data-driven strategy allowed the bank to avoid an estimated $15 million in potential losses when the CRE market corrected six months later. This is the tangible, bottom-line value of a modern risk management framework.

The Strategic Imperative for Better Data

This example underscores a core truth for banking leadership: risk assessment is no longer about appeasing regulators. It is about building a resilient institution capable of navigating uncertainty and capitalizing on opportunities. The ability to transform disparate data points into actionable intelligence is a primary competitive advantage.

This is precisely where platforms like Visbanking’s Bank Intelligence and Action System (BIAS) provide critical infrastructure. They supply the engine to aggregate, analyze, and visualize complex risk data, converting abstract numbers into clear, actionable directives. For executives, this means moving from asking "What happened?" to confidently answering "What should we do next?"

This is how to conduct risk assessments that genuinely protect and grow your institution. It begins with a commitment to leveraging data not as a compliance burden, but as your most valuable strategic asset. I encourage you to explore Visbanking’s data to benchmark your own performance and see how intelligence drives decisive action.

Building Your Risk Assessment Framework

An effective risk assessment is not an ad-hoc process; it is built on a disciplined, structured framework. Before identifying a single threat, you must define the scope and objectives of the engagement.

This foundational step prevents scope creep, aligns leadership, and ensures the final report is a strategic instrument, not a shelf document.

First, establish clear parameters. Is the assessment enterprise-wide, or is it focused on a specific high-stakes area like mortgage lending or treasury operations? Perhaps the scope is functional, such as evaluating the IT security of a new digital banking platform. Without these boundaries, the effort becomes inefficient, yielding ambiguous results.

Defining Measurable Objectives

Once the scope is defined, objectives must be specific and quantifiable. Vague ambitions like "improve cybersecurity" are strategically useless. A meaningful objective is measurable and has direct business implications.

For example: "Identify and quantify vulnerabilities in our new digital banking platform that could result in a financial loss exceeding $5 million."

In credit risk, instead of a general goal to "reduce potential credit losses," a data-driven objective would be: "Quantify the projected increase in credit loss provisions if local unemployment increases by 2% and commercial property values decline by 10%." This transforms a theoretical discussion into a focused financial stress test.

This is where data intelligence platforms provide an immediate strategic advantage.

An objective without a number is merely a suggestion. Tying risk assessment goals to specific financial metrics and peer benchmarks gives them strategic weight in the boardroom.

Consider a community bank seeking to manage its mortgage portfolio risk. Using a platform like Visbanking’s BIAS, leadership can instantly access real-time peer benchmarks on loan-to-value (LTV) ratios.

They observe that top-performing regional competitors maintain an average LTV of 75%, while their own portfolio stands at 80%. This provides immediate clarity.

This single insight allows them to formulate a goal the board can act on: "Reduce the portfolio's average LTV by 5% over the next two quarters to align with the top quartile of our peer group." This is an objective that can be tracked, measured, and achieved.

Assembling the Right Team with Board Sponsorship

Finally, no framework is complete without two critical human elements: unwavering board sponsorship and a dedicated, cross-functional team.

Board sponsorship provides the assessment with authority and signals its strategic importance to the entire organization. It ensures the team has the mandate and resources required for a thorough investigation.

The team itself must be a blend of diverse expertise. A risk assessment cannot be conducted in a silo. It requires leaders from:

- Finance: To model the financial impact of identified risks.

- Operations: To articulate practical, day-to-day vulnerabilities.

- Compliance: To ensure alignment with regulatory expectations.

- IT and Security: To address the technical threats that underpin modern banking.

When finance, operations, and IT convene around the same verified dataset, organizational silos break down, and a nuanced, holistic picture of the bank’s risk profile emerges. This groundwork is the essential first step in learning how to conduct risk assessments that drive meaningful change.

With a defined scope, measurable objectives, and a sponsored team, you have constructed the chassis for a powerful assessment. The next step is to fuel it with the right data. To see how your institution stacks up against key benchmarks, you can explore Visbanking's data intelligence platform.

Spotting Trouble with Smart Data

Effective risk identification is not a speculative brainstorming session; it is a deep, data-driven investigation into every facet of the bank’s operations. This is how you identify a latent threat before it materializes into a crisis.

You must move beyond surface-level reviews and delve into the data that reveals the ground truth. This involves analyzing historical loss data, internal audit reports, regulatory findings, and external threat intelligence. Synthesizing these disparate sources creates a coherent picture of your institution's true vulnerabilities.

The primary obstacle for most banks is not a lack of data, but data fragmentation. Information is siloed across the core system, loan origination software, cybersecurity logs, and the CRM. This fragmentation obscures critical connections between risk factors.

Bringing Your Data Together for a Clear View

The first step to identifying real risk is to aggregate scattered information into a unified view. This process makes abstract risks tangible and actionable. A dedicated intelligence platform is instrumental here.

For example, by blending its call report data with local economic forecasts on the Visbanking BIAS platform, a community bank can receive an early warning signal about its small business loan portfolio. The combined view might reveal a direct correlation between rising commercial vacancy rates in a specific zip code and the bank's loan concentration in that same area. This insight is invisible when data remains siloed.

This approach transforms risk management from a guessing game into a forensic analysis, providing the capacity to anticipate future challenges.

The most significant error is analyzing data sources in isolation. The most dangerous risks often develop in the intersections between seemingly unrelated datasets, such as the correlation between employee data and operational performance.

Consider a real-world scenario. One regional bank identified an emerging operational risk by connecting a spike in customer complaints from one branch with unusually high employee turnover at the same location. Individually, these were two separate data points managed by HR and customer service.

When viewed together on a unified dashboard, the narrative became clear: an understaffed, undertrained team was causing service failures. This connection, previously invisible, allowed the bank to intervene with targeted training and staffing support before significant customer attrition and reputational damage occurred. Executing this level of analysis requires robust data governance in banking to ensure information is accurate, consistent, and analysis-ready.

Uncovering Risks You Didn't Know You Had

With a unified data view, you can systematically probe different risk categories with precision.

Here is what that looks like in practice:

- Credit Risk: Do not just review loan concentrations. Stress-test the portfolio. Model the impact of an interest rate increase or a 5% decline in local property values on default rates.

- Operational Risk: Correlate system downtime logs with transaction error rates to pinpoint technology weaknesses. Map internal fraud incidents against access control records to identify security gaps.

- Market Risk: Model the effect of a 50-basis-point shift in the yield curve or significant currency fluctuations on your investment portfolio and interest-sensitive assets.

- Cybersecurity Risk: Use threat intelligence feeds to identify new malware targeting financial institutions. Cross-reference this information with your own vulnerability scans to assess your exposure.

This methodical, data-fueled approach ensures a comprehensive review. It transforms risk identification from a subjective exercise into an objective, evidence-based discipline. The objective is to see the entire board, not just a few pieces.

Analyzing and Prioritizing Financial Risks

Identifying a risk is the first step. Determining its strategic significance is the critical next one. You must prioritize which threats demand immediate attention and which constitute acceptable background noise. This requires a blend of quantitative analysis and expert judgment to translate abstract concerns into concrete financial models.

Risk prioritization is a disciplined process for determining which threats have the capacity to disrupt operations, erode capital, or damage the bank's reputation. High-quality data, subjected to rigorous analysis, is what separates a well-managed institution from one that is perpetually reactive.

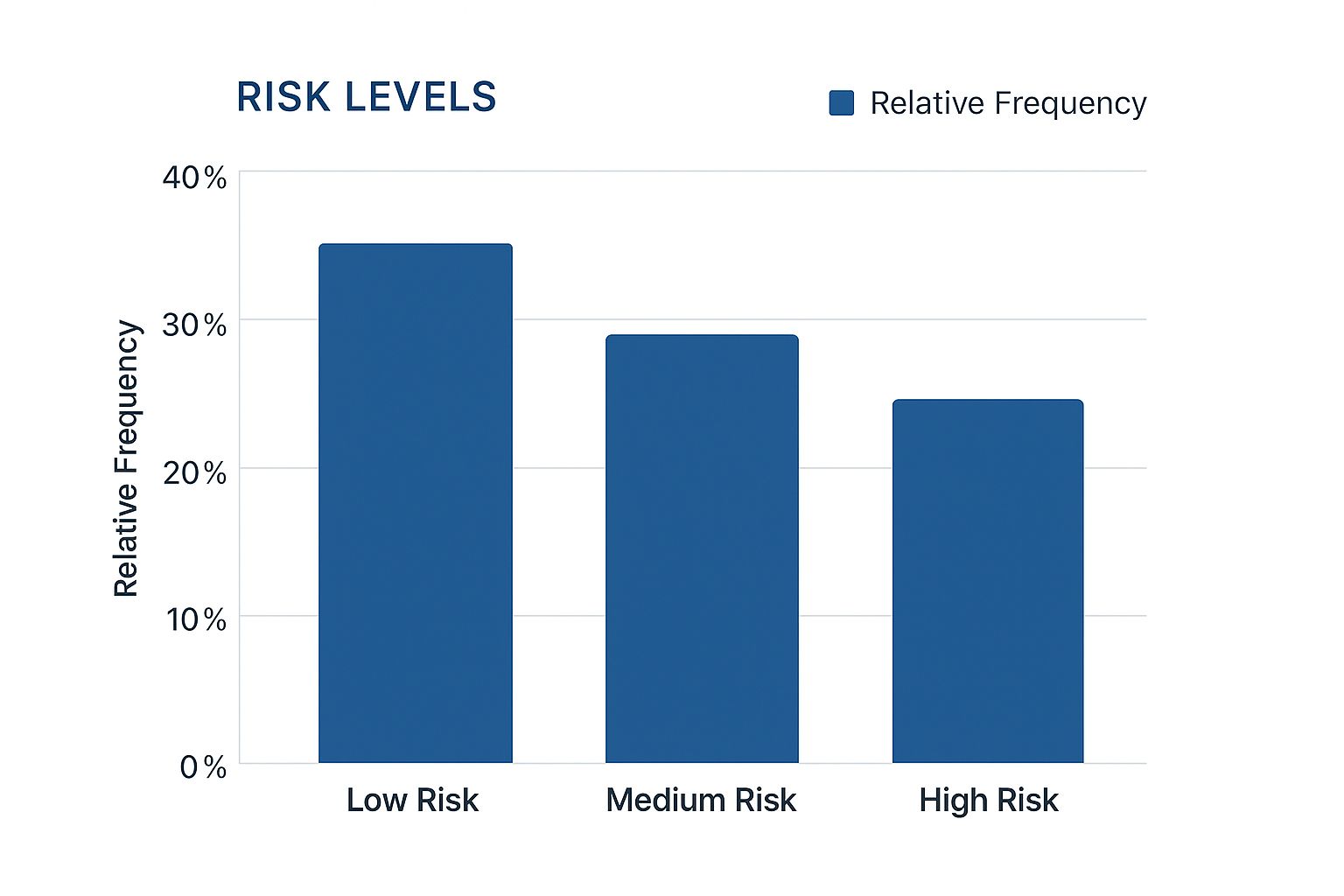

This chart illustrates a typical distribution of risks following initial analysis.

As shown, the highest-risk items constitute a smaller portion (25%), but they must be the primary focus of your mitigation plan.

Quantitative Analysis: Speaking the Language of Dollars and Cents

If a risk can be measured in monetary terms, it must be. Quantitative analysis translates a potential threat into a specific financial outcome—the language of executive leadership and the board. It shifts the conversation from "what if?" to "what is the cost?"

Two key methods include:

- Value at Risk (VaR): This model calculates the potential loss on a portfolio over a defined period at a specific confidence level. A VaR of $5 million at a 95% confidence level indicates a 5% chance of losing at least that amount on the next trading day. It is a simple, powerful metric.

- Probability of Default (PD): A cornerstone of credit risk management, PD models estimate the likelihood that a borrower will fail to meet their obligations. This is a core input for calculating expected credit losses.

To make this tangible, assume your bank is concerned about a cooling housing market. A quantitative model could demonstrate that a 10% decline in local property values would impact $400 million of your mortgage portfolio. The bottom-line impact? An estimated $8 million increase in loan loss provisions. That single number provides the clarity needed to act.

Vague assessments lead to hesitant decisions. Quantifying risk provides the concrete data points required for confident, decisive action. It’s the difference between saying “we have some CRE exposure” and “a 15% drop in office occupancy rates would increase our non-performing assets by $12 million.”

Qualitative Analysis: Sizing Up the Intangibles

Not all risks fit neatly into a spreadsheet. The cost of reputational damage from a data breach or a strategic misstep due to a missed shift in consumer behavior is difficult to quantify but can be equally severe.

This is where qualitative analysis tools, such as a risk matrix, are essential. Risks are plotted based on their likelihood and impact. A low-likelihood, low-impact risk (e.g., a minor clerical error) can be accepted. A high-likelihood, high-impact risk (e.g., a core system failure during business hours) demands immediate mitigation.

Peer benchmarks are an excellent tool for sharpening qualitative analysis. Comparing your key metrics against competitors can turn a vague concern into a clear priority.

Imagine the leadership team is concerned about the commercial loan portfolio. By using a platform with integrated peer data, they discover their commercial loan delinquency rate is 50 basis points higher than the regional average. Suddenly, a general worry becomes a specific, measurable problem demanding an action plan. This is a core function of top-tier banking risk management software, which translates raw data into strategic context.

To truly anticipate uncertainty, advanced tools like a Monte Carlo simulation can be a game-changer. Instead of producing a single static forecast, it runs thousands of "what-if" scenarios to map the probabilities of different outcomes.

Here’s a simplified look at how you might use a matrix to start prioritizing.

Risk Prioritization Matrix Example

This table provides a basic framework for scoring risks. By multiplying the likelihood of a risk by its potential financial impact, you derive a clear, comparable score that informs your prioritization.

| Identified Risk | Likelihood (1-5) | Financial Impact ($, 1-5) | Risk Score (L x I) | Priority Level |

|---|---|---|---|---|

| Major Cybersecurity Breach | 3 | 5 | 15 | High |

| Downturn in CRE Market | 4 | 3 | 12 | High |

| Key System Outage | 2 | 5 | 10 | Medium |

| Regulatory Fine (Minor) | 3 | 2 | 6 | Medium |

| Increased Employee Turnover | 4 | 1 | 4 | Low |

This approach formalizes what can otherwise be a subjective debate. When this structured judgment is combined with hard quantitative data, you build a true, 360-degree view of your risk landscape.

From Analysis to Actionable Mitigation Plans

Analysis without action is an academic exercise. Once hard data has been used to identify and prioritize risks, the critical work of developing concrete mitigation plans begins. For bank executives, this is where strategy is operationalized—moving from understanding a threat to neutralizing it.

Every mitigation strategy falls into one of four categories. The key is to apply the right response to the right risk, always balancing the cost of action against the potential consequences of inaction. This is not about reacting; it is about making a calculated business decision.

The Four Core Risk Responses

Your response to any given threat must be deliberate and well-documented. Each choice has direct implications for capital, operations, and the bank's strategic direction.

- Avoidance: The most decisive response—exiting a product line, market, or activity entirely. For example, if data indicates an unacceptably high fraud rate in a new instant payment service, projected to cost $2 million annually, the board may decide to discontinue the service. This is a strategic retreat to eliminate the risk.

- Reduction: This involves implementing controls to lower a risk's likelihood or potential impact. A classic example is tightening underwriting standards. If analysis shows that commercial loans with LTV ratios over 80% default at three times the portfolio average, leadership might cap new LTVs at 75%. This could lower potential defaults by 15% with a minimal impact on loan volume.

- Transfer: This strategy shifts the financial impact of a risk to a third party. Purchasing cybersecurity insurance to cover a potential data breach is a prime example. The bank pays a predictable premium to transfer the unpredictable—and potentially catastrophic—cost of a major cyber incident.

- Acceptance: Some risks are simply the cost of doing business. A bank might accept a low-level operational risk, such as minor teller cash discrepancies, because the cost of implementing stricter controls would exceed the potential losses, which might average less than $50,000 per year.

Communicating Risk to the Board and Regulators

Your findings must be presented in a format that drives decisive action. A dense, technical report will be ignored. A concise, data-backed executive summary will guide the strategic conversation. The goal is to distill complex analysis into a clear call to action.

A risk assessment's value is not measured by its page count, but by the quality of the decisions it inspires. The board needs a clear line of sight from the data, to the risk, to your proposed fix and its expected financial outcome.

Data visualization tools are invaluable here. Instead of presenting a spreadsheet of delinquency rates, a dashboard from a platform like Visbanking can display a heat map of credit risk by geography. This makes problem areas immediately apparent to all stakeholders, regardless of their technical background. This visual clarity builds consensus and accelerates decision-making.

For a structured approach, a solid bank risk assessment template can provide an excellent foundation for your reporting framework.

Your executive summary must be ruthlessly efficient. Focus on the top 3-5 risks that pose a material threat to the bank. For each, present the following:

- A Clear Risk Statement: What is the specific threat?

- The Quantified Impact: What is the projected financial or reputational cost?

- The Recommended Mitigation Plan: Which of the four responses is advised?

- The Cost and Benefit of Action: What is the plan's cost, and what is the expected reduction in risk exposure?

This structured approach transforms your risk assessment from a compliance task into a strategic playbook for building a more resilient and profitable institution. It is the final, crucial step in demonstrating how to conduct risk assessments that deliver tangible value.

Embedding Continuous Risk Monitoring into Your Strategy

A risk assessment is not a static report to be filed and forgotten. It is a living component of your ongoing strategy. In a market where new threats emerge quarterly, treating risk management as an annual event is a direct invitation to be blindsided.

The key to effective risk assessment is integrating continuous monitoring into the bank's operational rhythm. This shifts risk management from a reactive, backward-looking exercise to a proactive, forward-looking capability that safeguards the institution's future. The foundation of this system is Key Risk Indicators (KRIs).

Establishing Real-Time Key Risk Indicators

KRIs are your early warning system. They are specific, measurable data points that signal a potential shift in your risk profile. These are not generic, off-the-shelf metrics; they must be tailored to your bank’s specific vulnerabilities and strategic objectives.

Examples of effective KRIs include:

- A sudden, sustained decline in non-brokered deposits, which could indicate eroding customer confidence.

- An increase in the 30-day delinquency rate for a loan portfolio that exceeds the peer average by 0.5%.

- A sharp spike in failed login attempts on your digital banking platform, potentially signaling a cyberattack.

The objective is to anticipate events, not merely react to historical data. Using a data intelligence platform like Visbanking, you can set automated alerts for KRI breaches. This enables your team to make proactive adjustments—such as tightening underwriting or bolstering security—long before a risk translates into a loss.

A risk assessment that sits on a shelf for a year is already obsolete. Continuous monitoring turns static data into a dynamic shield, allowing leadership to anticipate and neutralize threats in real time.

Today's risk landscape is also deeply interconnected with global events. Geopolitical conflicts or international trade disputes can create shockwaves in your loan portfolio, affecting everything from supply chain financing to the creditworthiness of local businesses. The World Economic Forum's 2025 Global Risk Report underscores this, highlighting how geopolitical tensions directly fuel supply chain disruption and inflation. You can explore the full WEF report on global risks for a deeper analysis.

Incorporating this forward-looking intelligence is not just a best practice; it is a powerful competitive advantage. It allows you to stress-test your portfolio against macroeconomic shifts and what-if scenarios, ensuring your institution remains resilient.

Ultimately, by weaving continuous monitoring into your corporate DNA, the risk function becomes a true strategic asset. Want to see how your institution's key metrics stack up? Benchmark your performance and start exploring the data at Visbanking.

Your Top Questions Answered

How often should we really be doing a full risk assessment?

While regulators mandate an annual review, this should be considered the absolute minimum. In high-velocity risk areas like cybersecurity or credit, a yearly snapshot is obsolete upon completion.

The modern standard is continuous monitoring. The formal, enterprise-wide assessment is your annual physical, but you need a real-time monitoring system for daily operations. Any significant change—a new strategic initiative, an operational shift, or an economic disruption—must trigger an immediate reassessment. Data intelligence platforms are non-negotiable here, providing the live dashboards to make risk management a daily discipline, not an annual task.

What's the biggest mistake you see banks making with risk assessments?

The most common and costly error is treating risk assessment as a compliance-driven task delegated to a single department. This results in a siloed, check-the-box exercise disconnected from the bank's core strategy.

An assessment conducted this way is dead on arrival; it fails to deliver strategic value. The findings from a rigorous risk assessment must directly inform critical business decisions: lending policies, new product approvals, and operational budget allocation. Anything less reduces a powerful strategic tool to a retrospective report.

How do we get ahead of new threats like AI-driven fraud?

You cannot combat future threats with historical data alone. Relying solely on past loss data is a flawed strategy because it provides no insight into novel attack vectors.

Proactive threat modeling is the only viable defense against emerging, sophisticated risks. You cannot wait to be targeted; you must actively simulate how new types of fraud would impact your systems and your balance sheet.

In practice, this requires several key actions:

- Look beyond your own walls. Leverage external threat intelligence to understand the tactics being used against other financial institutions.

- Conduct simulations. Use data platforms to stress-test your defenses against sophisticated, simulated attacks to identify vulnerabilities.

- Engage with peers. Participate in industry information-sharing groups. A vulnerability identified at another institution is a valuable lesson for your own.

The objective is to shift from a reactive to a proactive posture. It is about hardening your defenses against the threats that are coming, not just those that have already occurred.

Ready to transform risk from a compliance burden into a strategic advantage? Visbanking helps you benchmark performance and convert complex data into clear, decisive action. See how our platform can give you an edge.

Latest Articles

Brian's Banking Blog

What Is Historical Analysis? a Banker's Working Definition

Brian's Banking Blog

Customer Churn Prediction: A Practical Guide for Banks

Brian's Banking Blog

Social Network Analysis for Banking: A Practical Guide

Brian's Banking Blog

How to Increase ROE: A Data-Driven Playbook for Bank Leaders

Brian's Banking Blog

What Is SEC EDGAR and How Banks Use the Data

Brian's Banking Blog