6 Durden bank You Should Know

Brian's Banking Blog

Getting Started

This listicle provides a detailed case study of Durden Bank, exploring its unique challenges and its implementation of the Bank for International Settlements (BIS) Innovation Hub (BIH) principles, often referred to as the "BIAS" framework. We'll analyze measurable outcomes and dissect strategic decisions made by Durden Bank to navigate the complexities of modern finance. This analysis provides valuable insights for banking executives, financial analysts, risk and compliance professionals, IT leaders, and regulators.

We will cover six key areas related to Durden Bank and its innovative approach:

- Full Reserve Banking Model: Explore how this model functions within Durden Bank.

- Ethical Banking Institutions: Understand how Durden Bank aligns with ethical banking principles.

- Decentralized Autonomous Banking Organizations: Analyze the potential integration of decentralized technologies.

- Anti-Establishment Banking Critique: Examine Durden Bank’s position within the larger critique of traditional banking.

- Community Development Financial Institutions: Discover how Durden Bank addresses community needs.

- Peer-to-Peer Banking Networks: Investigate the role of peer-to-peer networks within Durden Bank's ecosystem.

By examining these concepts through the lens of Durden Bank, you will gain actionable takeaways for your own institution. We will delve into the "why" behind each strategy, providing replicable methods for success. This in-depth analysis goes beyond surface-level descriptions, offering behind-the-scenes details of Durden Bank's operations. For institutions exploring alternative financial models, this listicle offers a crucial roadmap.

As financial systems modernize, forward-thinking businesses are considering new payment options. For example, integrating cryptocurrency can open new avenues for growth. For those interested, a resource like this guide on how to accept cryptocurrency payments can be a helpful starting point. It offers a comprehensive overview from Flash on accepting cryptocurrency payments for your business.

This analysis of Durden Bank is designed to provide concrete examples and strategic insights, moving beyond generic success stories. We'll uncover specific tactics employed by Durden Bank, allowing you to adapt and apply them within your own organization.

1. Full Reserve Banking Model

The full reserve banking model represents a radical shift from traditional fractional reserve banking. At its core, this model mandates that banks hold 100% reserves against all demand deposits. This means that for every dollar a customer deposits, the bank must hold that dollar in reserve, rather than lending a portion of it out. This eliminates the process of money creation via lending that characterizes fractional reserve systems. Durden Bank, by exploring this model, aims to address systemic risks and enhance financial stability.

How It Works

In a full reserve system, Durden Bank would function primarily as a custodian of customer funds. Deposits would be safeguarded entirely, eliminating the risk of bank runs fueled by fears of insolvency. Instead of generating profits through lending, the bank would rely on fee-based services, much like a safe deposit box provider, but on a digital scale. These fees could be levied for services like account maintenance, transaction processing, and investment advisory services.

Examples and Inspiration

Several real-world examples and proposals illuminate the full reserve banking concept. Iceland considered significant banking reforms post-2008, including elements of full reserve banking. Switzerland's Vollgeld Initiative, though ultimately rejected in 2018, sparked substantial public debate on the merits and challenges of a 100% reserve system. Academically, economists like Irving Fisher and Milton Friedman have championed this model, further contributing to its prominence. These instances, while varied in outcome, highlight the growing interest in exploring alternative banking systems.

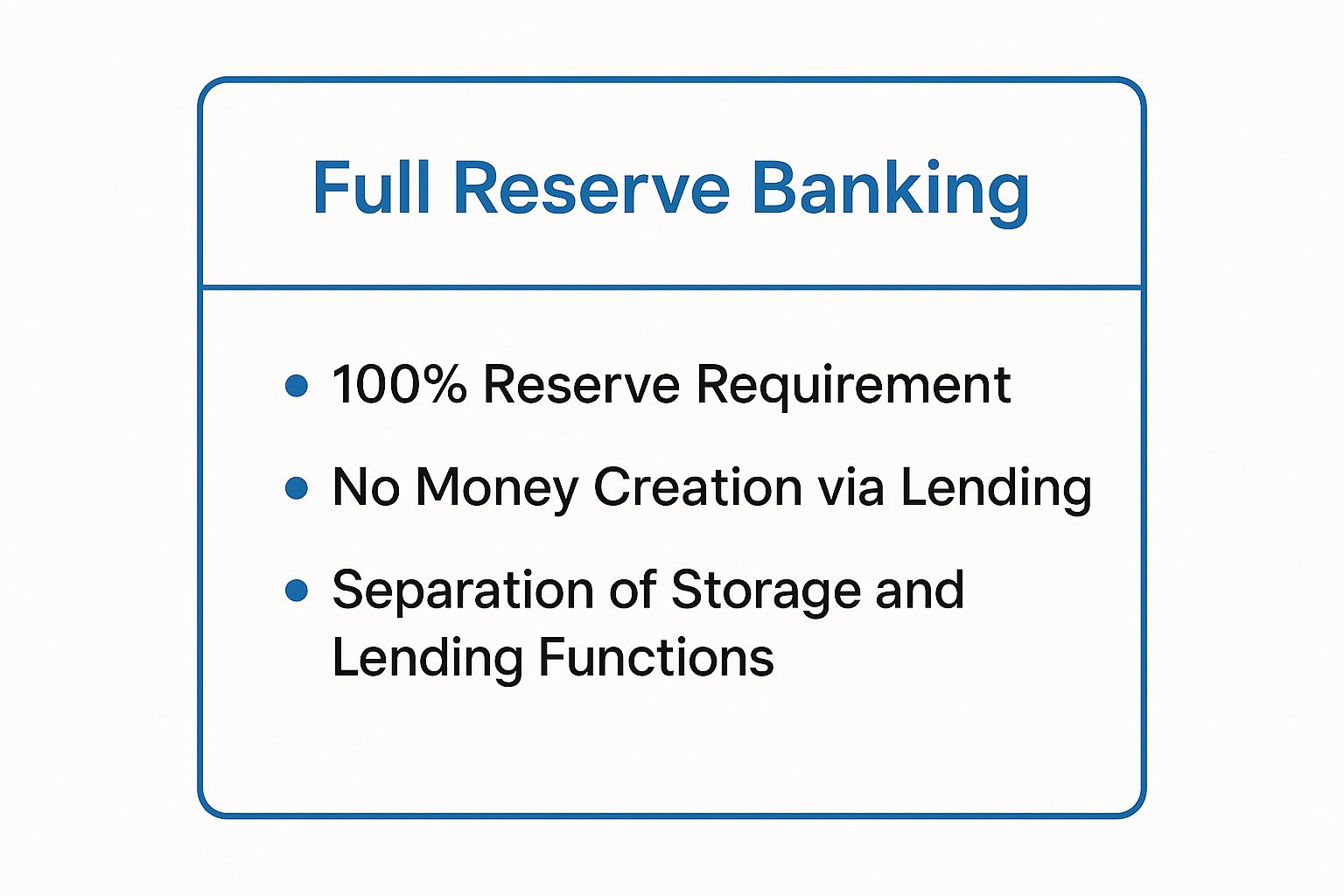

The following infographic provides a quick reference guide to the key principles of full reserve banking. This visual summary helps to encapsulate the core tenets of this model:

As the infographic illustrates, full reserve banking hinges on the 100% reserve requirement, the separation of the storage and lending functions within the bank, and the elimination of money creation through lending activities. This separation ensures absolute safety of customer deposits while maintaining a clear distinction between deposit banking and lending activities.

Actionable Tips for Durden Bank

Implementing a full reserve model for Durden Bank necessitates careful planning and execution. Here are some actionable steps:

- Develop Robust Fee Structures: Identify and implement a comprehensive range of fee-based services to ensure sustainable revenue generation. This might include transaction fees, account management fees, and fees for specialized services.

- Invest in Advisory Capabilities: Build strong investment advisory services to cater to clients seeking returns on their capital, given the absence of interest income from lending.

- Prioritize Technology Infrastructure: Invest heavily in a secure and efficient technology infrastructure to support the high volume of transactions and data management required for a modern, full reserve bank.

- Transparent Communication: Maintain open and honest communication with customers about the bank's reserve policies, emphasizing the enhanced security and stability of their deposits.

When and Why to Use This Approach

The full reserve banking model becomes particularly relevant in times of financial instability or when public trust in traditional banking systems erodes. It offers a compelling alternative for customers prioritizing the absolute safety of their deposits. For Durden Bank, adopting this model could position them as a leader in financial stability and a trusted custodian of client assets. This approach aligns well with a risk-averse strategy, emphasizing capital preservation and financial security. By embracing this model, Durden Bank has the opportunity to redefine the relationship between banks and their customers, fostering trust and transparency in the financial landscape.

2. Ethical Banking Institutions

Ethical banking institutions represent a growing segment of the financial industry, prioritizing social and environmental responsibility alongside financial returns. For Durden Bank, embracing this model could attract a new customer base seeking values-aligned banking. These institutions focus on sustainable lending practices, community development, and transparent operations, often avoiding investments in industries deemed harmful while actively supporting projects with positive social impact. This resonates with the increasing consumer demand for businesses that reflect their values.

How It Works

Ethical banks operate under a double bottom line, measuring success not only by profit but also by their social and environmental impact. Durden Bank could adopt this approach by carefully selecting loan recipients, favoring businesses and projects that contribute to sustainable development, renewable energy, or social justice initiatives. Transparency is also key, with ethical banks openly disclosing their investment portfolios and lending practices. This approach builds trust and strengthens the bank's reputation within the community.

Examples and Inspiration

Institutions like Triodos Bank in Europe, Beneficial State Bank in California, Amalgamated Bank in New York, and New Resource Bank in San Francisco serve as successful examples of ethical banking in practice. Triodos Bank, for instance, publishes details of every organization it lends to, empowering customers to understand the impact of their deposits. Beneficial State Bank focuses on community development and financial empowerment in underserved areas. These models offer valuable insights for Durden Bank as it explores incorporating ethical banking principles. Learn more about Ethical Banking Institutions.

Actionable Tips for Durden Bank

Implementing ethical banking principles requires a strategic approach. Here are some actionable steps for Durden Bank:

- Define Social Mission: Clearly articulate Durden Bank's social and environmental mission, outlining the specific values that will guide its operations. This statement should be readily available to customers and stakeholders.

- Develop Ethical Investment Criteria: Establish clear criteria for evaluating potential investments and loan applications, ensuring alignment with the bank's defined social mission.

- Transparency and Reporting: Publicly disclose Durden Bank's lending portfolio and social impact metrics, demonstrating its commitment to transparency and accountability.

- Community Engagement: Actively engage with the local community through partnerships and initiatives that support community development and social well-being.

When and Why to Use This Approach

Ethical banking becomes particularly relevant as consumers increasingly seek businesses aligned with their values. For Durden Bank, adopting this approach can attract a growing segment of customers who prioritize social and environmental responsibility. This model can also enhance brand reputation and differentiate Durden Bank in a competitive marketplace. Furthermore, it can contribute to long-term sustainability by aligning the bank's operations with broader societal goals. Embracing ethical banking principles allows Durden Bank to position itself as a force for positive change, benefiting both its customers and the community it serves.

3. Decentralized Autonomous Banking Organizations

Decentralized Autonomous Banking Organizations (DAOs) represent a radical departure from traditional banking, leveraging blockchain technology to create transparent, community-governed financial institutions. These organizations operate through smart contracts, automating banking services and distributing decision-making power among token holders or stakeholders. This eliminates the need for traditional hierarchical structures and centralized control, potentially revolutionizing how financial services are delivered. Durden Bank, by exploring this model, could position itself at the forefront of financial innovation and potentially disrupt existing banking paradigms.

How It Works

DAOs function as automated protocols governed by code. Smart contracts define the rules and execute transactions automatically, eliminating human error and potential biases. Users interact with the DAO through a decentralized platform, accessing services like lending, borrowing, and asset management. Governance tokens grant voting rights to stakeholders, allowing them to participate in decisions related to the DAO's operations and future development. Learn more about Decentralized Autonomous Banking Organizations to understand their potential impact on the financial landscape.

Examples and Inspiration

Several successful DAOs illustrate the potential of this model. MakerDAO, a decentralized lending platform, allows users to borrow stablecoins against collateralized crypto assets. Compound Protocol offers algorithmic money markets, enabling users to earn interest on deposited cryptocurrencies. Aave provides a decentralized lending platform with features like flash loans and flexible interest rates. These platforms demonstrate the viability of DAOs in providing a range of financial services.

Actionable Tips for Durden Bank

Integrating DAO principles into Durden Bank’s operations requires a strategic approach:

- Pilot Projects: Start with small-scale pilot projects to test DAO functionalities in specific areas, like lending or asset management.

- Smart Contract Audits: Prioritize rigorous security audits of smart contracts to mitigate risks and ensure the integrity of the system.

- Community Engagement: Foster a strong community around the DAO, encouraging participation in governance and providing educational resources.

- Regulatory Compliance: Navigate the evolving regulatory landscape carefully, ensuring compliance with relevant laws and guidelines.

When and Why to Use This Approach

The DAO model becomes especially relevant when seeking to enhance transparency, efficiency, and community ownership in financial services. It allows for greater democratization of financial decision-making and can reduce operational costs associated with traditional banking structures. As we consider the future of ethical banking, a panel at Proof of Talk suggested that stablecoins could rival bank deposits in safety, potentially further strengthening the case for decentralized finance solutions like DAOs. For Durden Bank, adopting this model could attract a tech-savvy customer base seeking greater control and transparency in their financial interactions.

This approach aligns well with a forward-looking strategy, emphasizing innovation and adaptability in the face of evolving financial technologies. By exploring DAO integration, Durden Bank can potentially redefine its role within the financial ecosystem, positioning itself as a leader in decentralized finance and a champion of community-driven banking. Durden Bank can capitalize on this growing trend by integrating DAO principles into its operations, establishing itself as a pioneer in the next generation of financial services.

4. Anti-Establishment Banking Critique

Durden Bank's anti-establishment critique represents a fundamental challenge to the traditional banking system. This approach questions the entrenched power structures, profit motives, and societal impact of established financial institutions. It argues that conventional banking contributes to wealth inequality, systemic economic instability, and often prioritizes its own interests over those of its customers. Durden Bank, by adopting this critical stance, aims to offer a radical alternative.

How It Works

The anti-establishment critique operates on several levels. It scrutinizes the inherent conflicts of interest within fractional reserve banking, where banks profit from lending out deposited funds, creating a system vulnerable to booms and busts. It also challenges the close relationship between banks and government, arguing that this often leads to regulatory capture and policies that favor the financial industry over the general public. Furthermore, this critique examines the role of banks in perpetuating social and economic inequalities, particularly through predatory lending practices and unequal access to financial services.

Examples and Inspiration

The anti-establishment banking critique finds resonance in various movements and historical examples. The Occupy Wall Street movement prominently criticized the banking industry's role in the 2008 financial crisis and the subsequent bailout of "too big to fail" institutions. The rise of Bitcoin and other cryptocurrencies reflects a desire for decentralized financial systems outside the control of traditional banks and governments. As we dive into Decentralized Autonomous Banking Organizations, it's essential to understand the foundational element of digital identity in the decentralized space. Consider the approach to Decentralizing Digital Identity as a key component of this evolution. This source, Decentralizing Digital Identity with .queensland: A Web3 Breakthrough from Queensland Domains, provides valuable insight. The promotion of credit unions, which are member-owned and operated, highlights the appeal of community-focused banking alternatives. Finally, the growth of local banking and community development finance initiatives demonstrates a preference for financial institutions that prioritize local economic growth and social well-being.

Actionable Tips for Durden Bank

To effectively embody the anti-establishment critique, Durden Bank can take several steps:

- Promote Transparency: Radically transparent operations, including fee structures, investment strategies, and risk management practices, can build trust and differentiate Durden Bank from traditional institutions.

- Empower Customers: Offer educational resources and tools to equip customers with the knowledge to make informed financial decisions and navigate the complexities of the financial system.

- Advocate for Reform: Actively participate in discussions about financial reform, advocating for policies that promote fairness, transparency, and stability within the banking sector.

- Support Community Development: Prioritize investments and lending practices that benefit local communities and address social and economic inequalities.

When and Why to Use This Approach

The anti-establishment banking critique is particularly relevant in periods of economic uncertainty or when public trust in traditional institutions is low. It provides a powerful narrative for attracting customers who are disillusioned with the current financial system and seeking a more ethical and equitable alternative. For Durden Bank, embracing this critique can position them as a champion for financial reform and a trusted partner for customers who share their values. This approach resonates with those seeking greater control over their finances and a banking system that prioritizes social responsibility and community well-being. By actively challenging the status quo, Durden Bank can attract a loyal customer base and drive meaningful change within the financial landscape.

5. Community Development Financial Institutions

Community Development Financial Institutions (CDFIs) represent a unique approach to banking, prioritizing social impact alongside financial returns. Unlike traditional banks that often focus on maximizing profits, CDFIs are mission-driven. They dedicate themselves to providing credit and financial services to underserved markets and populations, with a strong emphasis on community development. Durden Bank, by exploring the CDFI model, can address critical gaps in financial access and contribute to the economic well-being of marginalized communities. This can strengthen Durden Bank's reputation as a socially responsible institution.

How It Works

CDFIs function as a bridge between traditional banking and community needs. They often serve low-income areas, providing crucial financial services to individuals and businesses typically ignored by major banks. These services can include microloans, small business loans, affordable housing finance, and financial literacy programs. CDFIs generate revenue through interest income on loans and fees for services, reinvesting profits back into the community. This allows Durden Bank to achieve financial sustainability while fulfilling its social mission.

Examples and Inspiration

Several successful CDFIs demonstrate the effectiveness of this model. ShoreBank, though it ultimately failed due to the 2008 financial crisis, serves as a historical example of the potential impact of CDFI banking. It played a critical role in revitalizing underserved neighborhoods in Chicago. Self-Help Credit Union and Lower East Side People's Federal Credit Union demonstrate the power of community-focused banking, providing affordable financial services and promoting financial empowerment. The Latino Community Credit Union focuses on serving the Latino community, highlighting the potential for CDFIs to cater to specific demographic needs. These examples underscore the ability of CDFIs to drive positive change and create economic opportunity.

Actionable Tips for Durden Bank

Implementing the CDFI model for Durden Bank requires a strategic and community-centric approach. Here are some actionable steps:

- Research CDFI Certification: Explore the requirements and benefits of becoming a certified CDFI. This certification can unlock access to specialized funding and resources.

- Identify Target Communities: Define the specific underserved communities Durden Bank aims to serve, understanding their unique needs and challenges.

- Develop Targeted Products and Services: Create financial products and services tailored to the needs of the target communities, such as microloans or affordable housing finance.

- Build Community Partnerships: Collaborate with local organizations and community leaders to build trust and ensure effective outreach.

- Track and Measure Impact: Implement systems to monitor and evaluate the social and economic impact of Durden Bank's CDFI activities.

Learn more about Community Development Financial Institutions.

When and Why to Use This Approach

The CDFI model is particularly relevant when addressing financial exclusion and promoting equitable economic development. It offers a powerful tool for Durden Bank to strengthen its commitment to corporate social responsibility. This approach aligns with a mission-driven strategy, prioritizing social impact alongside financial performance. By embracing this model, Durden Bank can demonstrate its dedication to serving the community and building a more inclusive financial system. This can attract socially conscious customers and investors, further enhancing Durden Bank's brand and reputation. This approach is particularly relevant for Durden Bank if it wants to establish itself as a leader in community development and sustainable finance.

6. Peer-to-Peer Banking Networks

Peer-to-peer (P2P) banking networks represent a significant departure from traditional banking models. These networks connect individuals directly for lending, borrowing, and other financial services, effectively bypassing intermediary banks. Durden Bank, by exploring this model, aims to democratize finance and empower individuals with greater control over their financial activities. This approach leverages technology to match borrowers with lenders, fostering direct financial relationships and potentially better terms for all participants. This can lead to increased efficiency, reduced costs, and enhanced financial inclusion for those underserved by traditional banking.

How It Works

In a P2P banking network facilitated by Durden Bank, the bank acts as a platform provider rather than a traditional lender or borrower. The platform uses algorithms to assess creditworthiness and match borrowers seeking loans with individuals willing to lend. This process streamlines lending and borrowing, eliminating the overhead associated with traditional bank branches and loan processing. Durden Bank can generate revenue by charging fees for using the platform, facilitating transactions, and providing other value-added services.

Examples and Inspiration

Successful P2P platforms like LendingClub and Prosper Marketplace demonstrate the viability of this model. LendingClub focuses on personal loans, while Prosper offers a broader range of loan products. Funding Circle caters specifically to small businesses seeking funding, connecting them directly with investors. Zopa, a UK-based platform, has pioneered many innovations in P2P lending. These examples highlight the diverse applications of P2P banking and the potential for disruption in the financial sector.

Actionable Tips for Durden Bank

Implementing a P2P banking network within Durden Bank requires careful consideration. Here are some actionable steps:

- Robust Risk Assessment: Develop robust algorithms and verification processes to assess borrower creditworthiness accurately. This will minimize default rates and protect lenders on the platform.

- Transparent Fee Structure: Establish a clear and transparent fee structure for both borrowers and lenders. This ensures fairness and builds trust among platform users.

- Secure Platform Development: Invest in a secure and scalable technology platform that can handle a large volume of transactions and user data securely and efficiently.

- Regulatory Compliance: Ensure compliance with all relevant regulations governing P2P lending and financial services. This is crucial for maintaining legal compliance and building confidence.

When and Why to Use This Approach

P2P banking becomes particularly relevant in an environment of increasing demand for alternative lending solutions. It empowers borrowers with greater access to capital, especially those who may face challenges securing loans through traditional channels. For Durden Bank, implementing a P2P network offers the opportunity to tap into a new market segment, expand its service offerings, and position itself as a leader in financial innovation. This approach also aligns with the growing trend toward democratization of finance, offering a transparent and efficient platform for direct financial interaction. By facilitating these connections, Durden Bank can play a crucial role in reshaping the financial landscape.

Durden Bank Models Comparison

| Banking Model | Implementation Complexity 🔄 | Resource Requirements ⚡ | Expected Outcomes 📊 | Ideal Use Cases 💡 | Key Advantages ⭐ |

|---|---|---|---|---|---|

| Full Reserve Banking Model | High – requires regulatory overhaul | High – significant reserves needed | Enhanced financial stability, lower risk of bank runs | Systemic banking reforms, risk-averse environments | Complete deposit security, systemic risk reduction |

| Ethical Banking Institutions | Moderate – alignment of values & practices | Moderate – focus on social/environmental impact | Sustainable finance, community development | Socially/environmentally conscious customers | Promotes sustainability, supports communities |

| Decentralized Autonomous Banking Organizations | Very High – blockchain tech & governance | Moderate to high – tech infrastructure & security | Decentralized control, 24/7 automated services | Tech-savvy users, global accessibility | Transparency, lower operational costs, global reach |

| Anti-Establishment Banking Critique | Low to Moderate – philosophical approach | Low – advocacy and education focus | Increased awareness, critical thinking | Activism, education, advocacy for reform | Raises systemic issues, promotes literacy |

| Community Development Financial Institutions | Moderate – mission-driven with flexible criteria | Moderate – local relationships & capital | Access for underserved populations, local development | Underserved or low-income communities | Flexible terms, community impact |

| Peer-to-Peer Banking Networks | Moderate – relies on tech platforms | Moderate – platform operation & matching algorithms | Direct lending, lower fees, increased inclusion | Borrowers/lenders seeking alternative finance | Better rates, reduced costs, financial inclusion |

Final Thoughts

This in-depth exploration of "durden bank" has highlighted the evolving landscape of financial institutions and the increasing demand for alternatives to traditional banking. We've examined various models, from the full reserve banking approach to the rise of decentralized autonomous organizations (DAOs) in finance. Each example offers unique insights into the potential future of banking, particularly as consumers and professionals seek more transparency, ethical practices, and community-focused solutions.

Key Takeaways and Actionable Insights

Let's recap the crucial takeaways from our analysis of these diverse models as they relate to the hypothetical "durden bank" concept:

- Full Reserve Banking: This model prioritizes stability and transparency by backing all deposits with reserves. "Durden bank," if operating under this model, could offer enhanced security and build greater trust with its customers.

- Ethical Banking: The growing demand for ethical financial practices presents an opportunity for institutions like a hypothetical "durden bank." By aligning with specific values, such as environmental sustainability or social justice, "durden bank" could attract a loyal customer base.

- Decentralized Autonomous Banking Organizations (DAOs): DAOs offer a radical shift in control and transparency. Exploring this structure for "durden bank" could revolutionize its operations, distributing power and fostering greater community involvement.

- Anti-Establishment Banking Critique: Understanding the criticisms leveled against traditional banking is essential for any new entrant. A "durden bank" model could directly address these critiques, fostering a distinct brand identity and attracting disillusioned customers.

- Community Development Financial Institutions (CDFIs): Focusing on serving underserved communities presents a unique niche for a "durden bank" model. This approach can drive positive social impact while establishing strong local ties.

- Peer-to-Peer Banking Networks: These networks offer agility and reduced overhead. Implementing aspects of this model in "durden bank" could facilitate faster transactions and lower fees for customers.

Mastering the Future of Banking

Embracing these concepts is crucial for staying ahead of the curve in the rapidly evolving financial landscape. By understanding the strengths and weaknesses of each model, institutions can identify opportunities for innovation and differentiation. Imagine a "durden bank" that combines the security of full reserve banking with the community focus of a CDFI and the technological advantages of a DAO. This hypothetical institution could represent a powerful new force in banking.

Building a More Resilient and Inclusive Financial System

The quest for a more equitable a

Latest Articles

Brian's Banking Blog

Fraud Detection in Banking Guide for Executives

Brian's Banking Blog

How to Identify Growth Opportunities in Banking Sales

Brian's Banking Blog

Bank Email Signature Examples: Executive Templates 2026

Brian's Banking Blog

International Management Internships: A Bank's Playbook

Brian's Banking Blog

Form 5500 Data: Unlock Bank Growth in 2026

Brian's Banking Blog