Campbell and Fetter Framework: Transform Banking Decisions

Brian's Banking Blog

Understanding Campbell and Fetter Framework Foundations

Picture this: you're facing a major banking decision, drowning in endless spreadsheets and conflicting advice. This is where the Campbell and Fetter framework acts as your guide, offering a structured, repeatable method for making important choices. It helps you move past gut feelings and into the world of methodical analysis.

This framework isn't about one single decision; it’s about building a solid process that holds up under pressure. Think of it like a pilot's pre-flight checklist. A pilot doesn’t rely on memory or a "good feeling" to know a plane is ready for takeoff. They follow a precise procedure every single time to ensure all critical systems are checked and safety is certain. The Campbell and Fetter model gives banking leaders a similar checklist for financial decisions, reducing errors and improving results.

From Chaos to Clarity

Traditional decision-making in banking often mixes individual experience, intuition, and disconnected data. While experience is important, this method can be inconsistent and open to cognitive biases. Institutions that adopt the Campbell and Fetter framework see a major change from this reactive state to one of proactive, organized thinking.

This systematic approach is especially vital when dealing with complex regulations or market swings, where one mistake can have huge consequences. It pushes teams to set clear goals, gather the right data, weigh alternatives against specific criteria, and evaluate risks before moving forward.

This diagram shows the general cognitive steps in making a decision, which the framework helps structure and improve.

The main idea is that decision-making has multiple stages, and the Campbell and Fetter approach provides a clear path for each one.

A Tale of Two Approaches

To really see the difference this framework makes, it's helpful to compare the old way of making decisions with the new. Successful banks have found that using a structured process leads to more predictable and defensible outcomes. The core idea is to build your organization's ability to make sound judgments consistently.

To better illustrate this shift, the table below contrasts the informal, traditional style with the methodical approach of the Campbell and Fetter framework.

Traditional Banking Decisions vs Campbell and Fetter Framework

A comparison showing how traditional banking decision-making differs from the structured Campbell and Fetter approach

| Decision Aspect | Traditional Approach | Campbell and Fetter Framework | Key Benefits |

|---|---|---|---|

| Data Usage | Relies on intuition and siloed information | Systematic, driven by predefined criteria | Reduces bias and improves consistency |

| Risk Assessment | Subjective, based on past experience | Formal, follows a specific protocol | Uncovers hidden risks and helps ensure compliance |

| Process | Ad-hoc and inconsistent from one decision to the next | Standardized and repeatable for all major decisions | Creates efficiency and leads to predictable outcomes |

| Accountability | Often unclear or concentrated on one person | Clearly defined and documented for the whole team | Improves transparency and promotes learning |

Ultimately, the table highlights a fundamental change in philosophy. The Campbell and Fetter framework moves banking decisions from a private art form, dependent on individual heroics, to a transparent science that can be learned, repeated, and improved across the entire organization.

The Evolution Story Behind Campbell and Fetter Success

Every great idea has a story, and the Campbell and Fetter framework is no different. It wasn’t dreamed up in a quiet boardroom; it was forged in the fire of real-world banking crises and market swings. The framework was a direct answer to a pressing need for a consistent and dependable way to make banking's most important decisions. Like any major breakthrough, its path from an idea to an industry standard was paved with trial, error, and refinement based on what truly worked under pressure.

To grasp its success, think about a completely different industry. The Campbell Soup Company, founded way back in 1869, originally sold all sorts of canned goods. The company's big moment came in 1897 when a chemist, John T. Dorrance, figured out how to make condensed soup by halving its water content. This one change slashed costs, made shipping easier, and put the product within reach of millions, turning the company into a household name.

The Campbell and Fetter framework followed a similar path by zeroing in on and solving a major weakness: inconsistent decision-making in banking.

This image shows the iconic Campbell's soup can, a perfect symbol of how a standardized, reliable product can define a market. Just as the condensed soup formula gave consumers a trustworthy meal, the framework gives financial leaders a trustworthy process.

From Theory to Battle-Tested Tool

The shift from a theoretical concept to a practical, trusted tool didn't happen overnight. Early versions were put to the test against the harsh realities of the financial world. Skeptical bankers wanted to see proof, not just hear promises. The framework earned its stripes through key moments where its application led to clearly better results.

These moments were crucial in proving its worth:

- Initial Crisis Response: When first used during market downturns, it showed a remarkable ability to bring order to chaos, stopping leaders from making rash, fear-based mistakes.

- Regulatory Scrutiny: As compliance demands intensified, the framework gave banks a documented, defensible process that stood up to the scrutiny of auditors and regulators.

- Performance Metrics: Institutions that adopted its principles saw real, measurable gains in areas like loan performance and risk management, providing solid evidence of its value.

This journey solidified its core parts, turning abstract ideas into the dependable, proven system used by banks today. Understanding this history is key to seeing why the framework is so powerful.

Essential Components That Drive Campbell and Fetter Results

To really get what makes the Campbell and Fetter framework tick, you need to look under the hood. Think of it like a high-performance engine—its power isn't from one single part, but from how multiple, finely-tuned components work in concert. Each piece is designed to patch a specific hole in traditional banking decisions, creating a system that is strong, adaptable, and great at delivering consistent results. By understanding these individual parts, you can see how they build a much stronger whole.

Core Pillars of the Framework

The framework's success rests on a few core pillars that shift decision-making from an unpredictable art to a more reliable science. These aren't just abstract concepts; they are practical tools meant to bring clarity and structure to complex situations. For example, legal advocacy is a key area. A professional association once mobilized its legal team for an amicus brief to protect its standards, showing the value of a structured, expert-led response to big challenges.

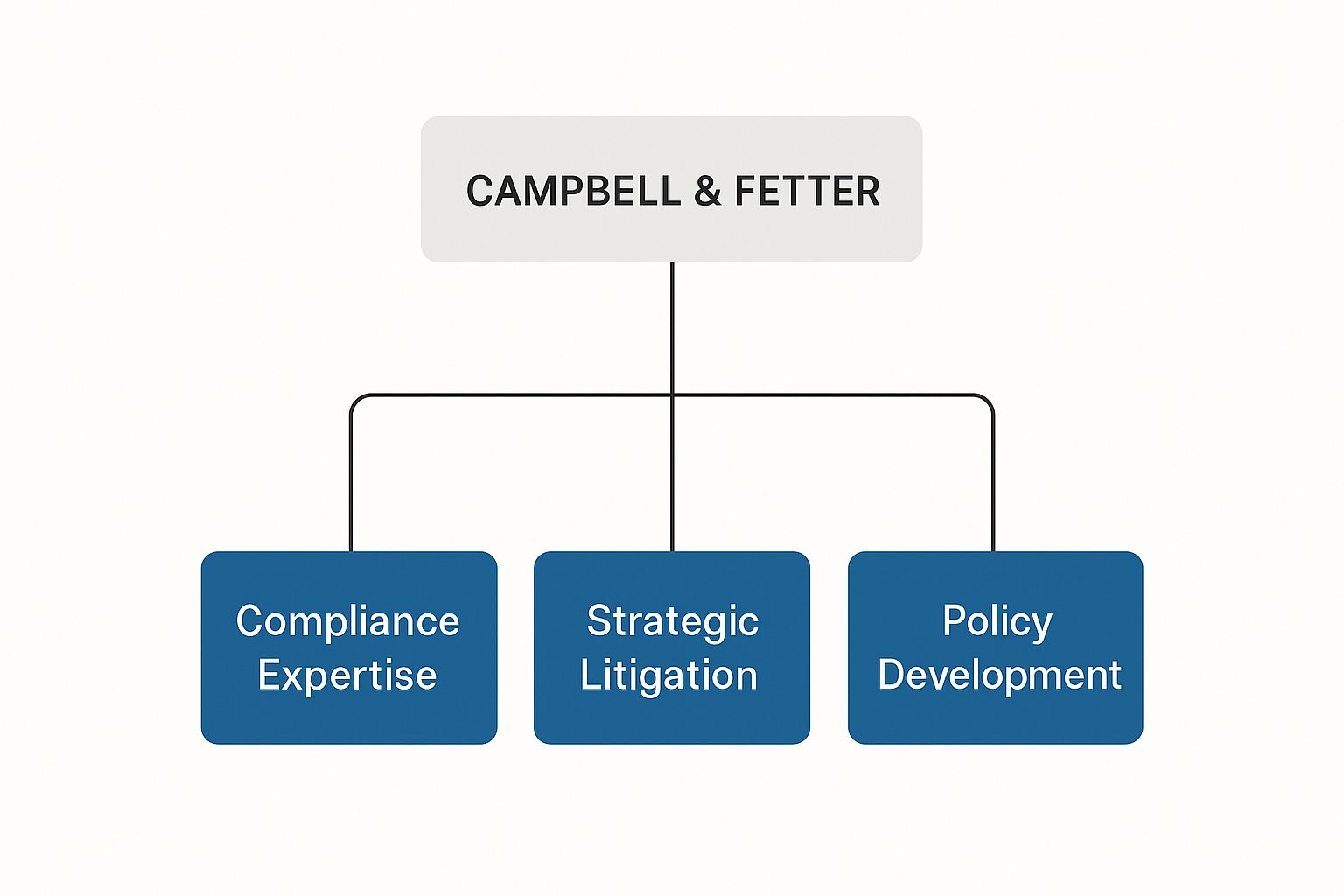

The following infographic shows the main operational areas where the framework adds significant value.

This visual breaks down how the framework’s strengths are built around expertise in compliance, strategic legal action, and policy development. These connected elements help ensure every decision is not just strategically sound but also legally and ethically solid. The model isn't about a single process but a complete way of thinking. This reinforces a core principle of the Campbell and Fetter model: success is born from the dynamic interplay between its parts, not just their individual functions.

The table below breaks down these core components, showing how they function within a banking context and what success looks like for each.

| Component | Primary Function | Banking Application | Success Metrics |

|---|---|---|---|

| Legal Advocacy | To provide expert legal guidance and representation. | Defending against regulatory challenges or lawsuits. | Favorable legal outcomes, reduced litigation costs, minimized regulatory fines. |

| Compliance Expertise | To ensure all operations adhere to current laws and regulations. | Developing and auditing internal policies to meet standards like BSA/AML. | 100% pass rate on internal and external audits, no compliance-related penalties. |

| Strategic Action | To plan and execute proactive measures to achieve long-term goals. | Launching a new digital banking product based on market analysis and risk assessment. | Increased market share, improved profitability, successful product adoption rates. |

| Policy Creation | To establish clear, standardized guidelines for decision-making. | Creating a new loan approval policy to balance risk and growth. | Consistent application of standards, lower default rates, streamlined approval times. |

This table shows how each component has a distinct role but works toward the common goal of strengthening the bank's operational integrity and strategic position.

Key Operational Tools

Within this structure, several operational tools drive day-to-day results. These are the gears that keep the engine running smoothly.

- Decision Matrices: These tools help remove guesswork. They force teams to evaluate options against a standard set of criteria, ensuring objectivity and alignment with the bank's strategic goals.

- Validation Checkpoints: Think of these as quality control gates. They prevent expensive mistakes by requiring review and approval at critical points in the decision-making process. They are designed to spot flaws before they become major problems.

- Feedback Mechanisms: The framework includes structured loops for ongoing improvement. After a decision is put into action, its outcome is analyzed. The lessons learned are then fed back into the system to sharpen future choices. For those curious about how technology can automate these feedback loops, you might find it useful to learn how the BIAS system revolutionizes banking decision-making.

Real Banking Transformations Using Campbell and Fetter

Theoretical frameworks are nice, but their real value shows up on the bottom line. The Campbell and Fetter model truly excels here, producing tangible improvements for financial institutions that adopt its structured approach. From community banks to large investment firms, the stories of its application show a clear pattern: lower risk, better efficiency, and sharper strategic focus. These aren't just feel-good tales; they are real accounts of overcoming tough problems and achieving major breakthroughs.

You can think of it like a major business shift in another industry. Take John T. Dorrance's invention of condensed soup in 1897, which completely changed the game for the Campbell Soup Company. By drastically cutting the water content, the company slashed shipping costs and extended shelf life, making its soup affordable and available to millions. This one change propelled sales past $100 million by 1942, securing its position as a market leader. In a similar way, the Campbell and Fetter framework offers a core process improvement that strengthens a bank's operational health and competitive standing. You can find out more about this historic business shift on Britannica.

Case Study: A Regional Bank's Turnaround

One of the clearest examples comes from a regional bank struggling with high loan default rates and slow approval times. It was losing ground to bigger, faster competitors. By putting the Campbell and Fetter framework into practice, the bank created a clear, data-driven process for evaluating loans that every underwriter had to follow.

The beginning was difficult. Loan officers who were used to relying on their gut feelings pushed back. However, the leadership team stayed the course, offering training and highlighting early successes. Within 18 months, the results were impossible to ignore. The bank saw a 40% reduction in loan default rates and cut its average loan approval time by three days. This turnaround allowed them to win more market share without piling on unnecessary risk.

Here’s a look at the different functions within the banking industry that a structured framework can positively affect.

The image illustrates the wide range of banking activities, from retail and corporate services to investment management, all of which benefit from the systematic decision-making the framework introduces.

Investment Firms and Retail Banking Wins

The framework is flexible enough to work far beyond commercial lending. An investment firm used its principles to standardize its risk assessment for complicated portfolios. This didn't replace human expertise. Instead, it focused it more effectively. Analysts were freed up to concentrate on high-value strategic thinking instead of repetitive data checks. The firm reported a 15% increase in its ability to spot and act on profitable opportunities that it had previously overlooked.

Retail banks have also applied the Campbell and Fetter model to their customer acquisition strategies. By building a structured process to analyze marketing campaign data and customer feedback, they could make smarter, evidence-based choices about where to spend their marketing budget. This led to more successful outreach and stronger client relationships.

Supercharging Campbell and Fetter With Visbanking BIAS

When a proven methodology meets modern technology, something special happens—it reshapes how decisions are made. The integration of the Campbell and Fetter framework with Visbanking's BIAS system is a major step forward, shifting banking strategy from static, manual analysis to smart, adaptive automation. This combination doesn’t just support the framework; it amplifies it, adding speed, depth, and predictive power to its solid foundation.

Think of the original Campbell and Fetter model as a detailed blueprint for building a sturdy ship. It's reliable and based on sound principles. Now, imagine giving that ship an advanced navigation system like BIAS. This system uses real-time data to not only follow the blueprint but also to anticipate storms, find clear passages, and optimize the route for speed and safety. BIAS does for the framework what modern tech does for shipbuilding—it makes an excellent design perform at a much higher level.

From Manual Analysis to Intelligent Action

The biggest advantage of this integration is the shift from slow, work-intensive processes to a smooth, automated workflow. Instead of teams spending weeks collecting data to feed into the Campbell and Fetter process, BIAS delivers the necessary insights almost instantly.

This reflects a broader evolution in banking technology, aimed at supporting more complex operations.

Just as self-service machines automated routine transactions, BIAS automates the intricate data analysis that forms the basis of strategic decisions. The integration is built to preserve the essential human judgment that makes the framework so effective, while using technology to improve accuracy and speed.

Here’s how this combination creates a better approach:

- Advanced Analytics: BIAS processes huge datasets, finding trends and connections that are invisible to the naked eye. This gives every decision a richer, more detailed context.

- Predictive Modeling: The system can forecast the potential results of different strategic moves, letting leaders "test" a decision before they commit resources to it.

- Real-Time Monitoring: Once a decision is made, BIAS tracks its impact as it happens, offering immediate feedback and allowing for quick adjustments if needed. Ensuring the integrity of these AI-driven decisions requires a focus on transparency, and learning about people-centric approaches to algorithmic explainability is key to maintaining fairness.

- Automated Reporting: Stakeholders get clear, simple reports without being overwhelmed by raw data.

The result is a hybrid model that produces faster, more dependable outcomes without giving up quality. For those interested in this evolution, you can learn more about the Bank Intelligence and Action System. This fusion of structured methodology and smart technology points to the future of banking strategy.

Your Campbell and Fetter Implementation Roadmap

Bringing the Campbell and Fetter framework into your bank isn't like flipping a switch; it's a carefully planned journey. To get it right, you need a practical blueprint based on what has worked for other institutions. Success starts with solid groundwork that prepares your organization for lasting change and real results.

Setting the Stage for Success

The first steps are the most critical. This isn't just about announcing a new system. It's about getting the entire organization ready for a new way of thinking and operating. This means deep engagement and clear communication to get everyone, from the executive team to the frontline staff, on the same page.

Key initial activities include:

- Stakeholder Alignment: Gaining buy-in requires more than a single presentation. It's about having ongoing conversations to address worries, explain the benefits, and ensure all leaders are speaking with one voice. Without this unity, even the best plans can fail.

- Team Preparation: Pinpoint the teams that will see the biggest changes and give them the training and tools they need ahead of time. This builds confidence and reduces resistance before it can even start.

- Defining Success: Before you begin, decide what success looks like. Set clear Key Performance Indicators (KPIs), such as faster decision-making, reduced risk exposure, or better compliance scores. This allows you to track your progress and prove the value of the new approach.

Phased Deployment and Overcoming Obstacles

Trying to implement everything at once is a huge risk. A phased deployment approach is a much smarter and safer strategy. You can introduce the framework in one department, learn from that experience, and then expand. This approach minimizes disruption and builds positive momentum as people see the benefits firsthand.

The diagram below shows a well-known model for managing organizational change, which is essential for any framework rollout.

As this image shows, successful change happens in steps. It highlights why you need a structured and well-thought-out plan. You will face challenges—that’s a guarantee. Veterans of these projects always recommend planning for common hurdles, like resistance to new processes or data integration headaches. Keeping communication lines open and celebrating small victories along the way are proven methods for keeping the project moving forward when things get tough.

Measuring Success and Optimizing Campbell and Fetter Performance

Putting a new decision-making system in place is just the first step. The real question is whether it actually delivers value. To track the success of a Campbell and Fetter implementation, you can't just look at one or two data points. Think of it as a complete health check-up for your bank's strategic thinking—you need to check the vital signs (the numbers) and the overall sense of well-being (the human feedback) to see the full picture.

This means setting clear benchmarks and consistent ways to evaluate performance. The goal is to move beyond just doing things differently and start doing things better.

Key Metrics for Evaluation

Success with the Campbell and Fetter framework is measured through a blend of hard numbers and softer, but equally critical, indicators. Together, they tell a complete performance story.

- Quantitative Measures: These are the concrete, data-driven results that show up on a spreadsheet. They often include metrics like lower loan default rates, faster decision-making times, reduced fines related to compliance, and better operational efficiency. These numbers provide solid proof of the framework's financial and operational benefits.

- Qualitative Indicators: These metrics get at the human side of the change. Are leaders more confident in their decisions? Are stakeholders happier? Is team morale up? These are usually measured through surveys and structured feedback sessions.

This diagram shows the general principles of performance measurement, which are essential for checking how well any framework is working.

The visual breaks down how inputs and activities produce outputs and outcomes—a sequence that's key to understanding your framework's real-world impact.

Continuous Refinement and Evolution

The Campbell and Fetter framework isn't a "set it and forget it" tool. The best-performing banks treat it like a living system that needs constant attention and optimization. This means building performance dashboards that give you actionable information and creating feedback loops to keep making improvements. For a deeper dive into what makes measurement effective, looking at principles from related fields, like those discussed in Content Engagement Metrics, can provide useful perspectives.

This flexible approach ensures the framework adapts to new market challenges and changing rules, keeping its core strengths while staying current. By consistently measuring and optimizing, your investment in Campbell and Fetter will continue to pay off long after you first put it in place.

Ready to see how your bank's performance stacks up against the competition? Discover your strategic advantages with Visbanking and turn data into decisive action.

Latest Articles

Brian's Banking Blog

What Is HMDA Data: A 2026 Guide for Banking Success

Brian's Banking Blog

Credit Union Competition: A Bank's Guide to Winning

Brian's Banking Blog

Banks Singer" SEO: Convert Traffic for Your Bank

Brian's Banking Blog

Regulatory Reporting Challenges: Turn Compliance Into A

Brian's Banking Blog

Bank Churn Analysis: Executive Guide 2026

Brian's Banking Blog