A Strategic Guide to Bank Capital Ratios for Bank Executives

Brian's Banking Blog

Bank capital ratios are more than regulatory metrics; they are the definitive measure of your institution's financial resilience and strategic capacity. For executives and board members, a command of these figures is fundamental to navigating risk, seizing growth opportunities, and delivering shareholder value. They are the hard numbers that quantify your ability to absorb shocks, fund expansion, and maintain market confidence.

Why Your Capital Ratios Define Your Strategy

A deep understanding of capital adequacy transcends mere compliance. The core ratios—Common Equity Tier 1 (CET1), Tier 1, and Total Capital—articulate your bank's financial strength to regulators, investors, and competitors. They dictate your capacity to weather economic downturns, which in turn influences every material decision, from mergers and acquisitions to capital return policies.

A robust capital position is not a defensive measure. It is an offensive asset that provides the financial firepower to act decisively when strategic opportunities emerge.

Turning Ratios into Real-World Action

Consider two banks, each with $10 billion in risk-weighted assets (RWA).

Bank A maintains a strong CET1 ratio of 12%, positioning it comfortably above regulatory minimums and its peer group average. Bank B operates with a leaner CET1 ratio of 9.5%. While compliant, its capital buffer is materially thinner.

When a compelling acquisition target appears, Bank A's leadership can approve the transaction with confidence, knowing its capital base can readily absorb the additional risk-weighted assets. Bank B’s management team must hesitate. Pursuing the same opportunity would push its capital ratios toward regulatory thresholds, inviting heightened scrutiny and constraining future strategic options.

This scenario illustrates a critical principle for bank leadership:

Capital is not a static compliance metric; it is a dynamic resource that dictates strategic freedom. A superior capital ratio expands the playbook for growth, innovation, and shareholder returns.

Proactive capital management allows an institution to execute on opportunities that competitors, constrained by their capital position, cannot pursue.

The Visbanking Perspective

This is precisely where precise data intelligence becomes indispensable. Static, quarterly reports offer a rearview-mirror perspective. To make forward-looking strategic decisions, executives require real-time, comparative analysis of their capital ratios against a curated peer group. Identifying a divergence—whether you are lagging or leading in capital efficiency—enables strategic adjustments before market or regulatory pressures force your hand.

At Visbanking, we view capital management as the core of competitive banking strategy. Our platform is engineered to transform raw capital data into actionable intelligence. By benchmarking performance, you gain immediate clarity on whether your capital is a source of strategic advantage or a constraint on your ambitions.

Decoding the Core Capital Ratios for Executives

Effective strategic leadership requires a granular understanding of the entire capital stack. A single ratio provides an incomplete picture. The three primary ratios—CET1, Tier 1, and Total Capital—each offer a distinct perspective on your bank's financial health. Analyzing them collectively reveals not only your regulatory standing but also your true capacity to absorb losses and fund growth.

The framework is built on the concept of capital quality. Not all capital instruments are created equal; the regulatory system prioritizes those that can absorb losses on a going-concern basis.

Common Equity Tier 1 (CET1) Capital

CET1 is the bedrock of a bank's capital structure. Comprising common stock and retained earnings, it represents the highest-quality, most loss-absorbing capital.

This is the ultimate measure of resilience. CET1 capital can absorb losses without triggering insolvency or creating an obligation for repayment. It is the capital that ensures operational continuity during periods of severe stress.

Consider a $2 billion bank with $150 million in CET1 capital against $1.5 billion in risk-weighted assets, yielding a CET1 ratio of 10%. If the bank incurs $30 million in unexpected loan losses, the loss directly reduces retained earnings, lowering CET1 capital to $120 million. The new ratio becomes 8%—still above the regulatory minimum. The bank absorbs the shock and continues operations. This demonstrates the critical function of a strong CET1 position.

Tier 1 Capital

Tier 1 Capital includes CET1 plus additional Tier 1 instruments, such as non-cumulative perpetual preferred stock. This capital is still considered core to a bank's strength but is subordinate in quality to common equity.

While these instruments provide a valuable buffer, they may carry obligations, such as fixed dividend expectations, that are not present with common stock. The Tier 1 ratio offers a broader view of core capital, but CET1 remains the ultimate benchmark of financial strength. For a deeper look, you can explore our detailed analysis of why the Tier 1 capital ratio is essential for bank safety.

Total Capital

Total Capital represents the sum of Tier 1 and Tier 2 capital. Tier 2 consists of supplementary instruments like subordinated debt and certain loan-loss reserves.

Tier 2 is often termed "gone-concern" capital because its primary function is to protect depositors and the financial system in the event of a bank's failure. While essential for regulatory compliance, it does not support day-to-day operations in the same manner as Tier 1 capital.

An executive takeaway: A bank with a high Total Capital ratio but a comparatively weak CET1 ratio may appear well-capitalized on the surface but possesses limited operational flexibility in a crisis. The quality of capital is as critical as the quantity.

The banking industry has significantly bolstered its capital defenses post-crisis. The average CET1 ratio for global banks now stands at approximately 12.8%, substantially exceeding Basel III minimums and representing a stark contrast to pre-2008 levels.

This overview provides a framework for understanding how these ratios interrelate and inform strategic planning.

Overview of Key Bank Capital Ratios

| Capital Ratio | Primary Components | Minimum Requirement (Basel III) | Strategic Implication for Executives |

|---|---|---|---|

| CET1 Ratio | Common Stock, Retained Earnings | 4.5% | Your primary measure of operational resilience. A high CET1 ratio signals strength and flexibility to weather economic storms and pursue growth. |

| Tier 1 Ratio | CET1 + Additional Tier 1 (e.g., preferred stock) | 6.0% | A broader view of your high-quality capital. This ratio indicates your core strength to absorb losses while continuing to operate. |

| Total Capital Ratio | Tier 1 + Tier 2 (e.g., subordinated debt) | 8.0% | The most comprehensive regulatory measure. While important for compliance, a high ratio here with weak CET1 may suggest a less resilient capital structure. |

This table provides a reference, but true strategic insight comes from applying this framework to your bank’s specific competitive context.

Using Data to Drive Your Capital Strategy

Understanding the definitions of these ratios is foundational. The strategic advantage comes from applying this knowledge to your bank's positioning. A robust data intelligence platform moves capital analysis from a compliance exercise to a strategic function.

With a tool like Visbanking, you can benchmark your CET1, Tier 1, and Total Capital ratios against your direct competitors. This is where actionable intelligence is found. For instance, discovering that your bank's CET1 ratio lags peers while your Total Capital is higher may indicate an over-reliance on subordinated debt. This insight drives more informed capital planning, superior M&A positioning, and ultimately, a more resilient institution.

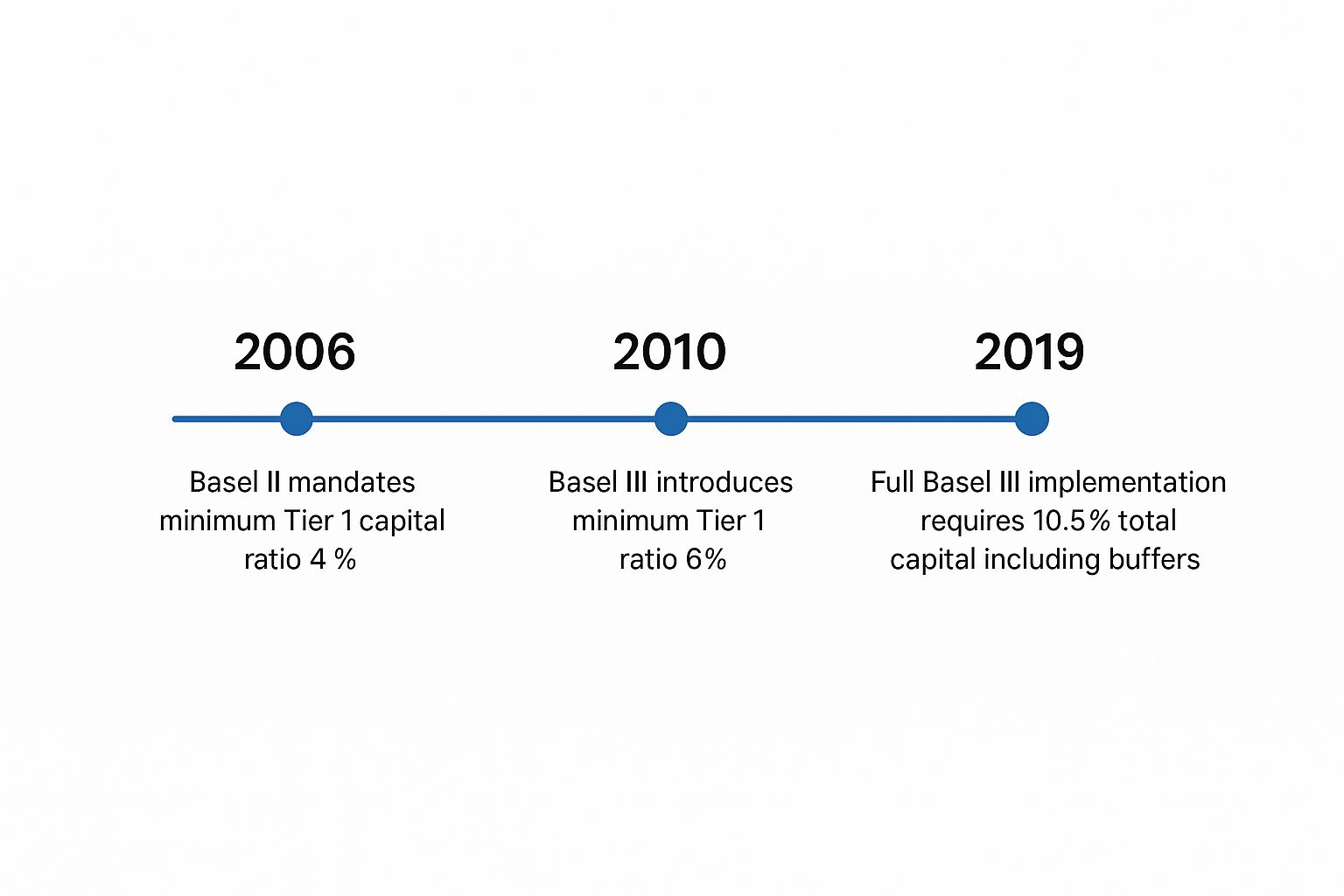

The Regulatory Road from Basel I to Today

Making forward-looking decisions requires an understanding of the regulatory framework governing bank capital. These rules are not arbitrary; they are the direct result of lessons learned from past financial crises. This history provides a roadmap for anticipating future regulatory direction and positioning your bank to stay ahead of evolving standards.

The journey began with Basel I, an initial framework for risk-weighting assets that, while groundbreaking, proved too simplistic. This led to the more risk-sensitive Basel II. However, the 2007-08 Global Financial Crisis exposed fundamental weaknesses in the global banking system.

The Post-Crisis Reckoning

The crisis revealed that many major financial institutions were operating with dangerously thin capital buffers, insufficient to withstand a systemic shock. The existing standards were inadequate.

Regulators responded with decisive action. Prior to the crisis, Tier 1 capital ratios below 5% were common, with some institutions operating near 1.5%. Basel III fundamentally altered this landscape. It established a new minimum CET1 ratio of 4.5% and introduced additional capital buffers, effectively pushing the all-in minimum requirements toward 8%—and higher for systemically important banks.

The regulatory timeline shows a clear and deliberate trend toward higher and higher-quality capital requirements.

This sustained regulatory pressure has been aimed at building a more resilient banking sector by demanding greater capital cushions.

What Really Changed with Basel III

Basel III was not an incremental adjustment but a comprehensive overhaul focused on capital quality and systemic resilience. For bank leadership, understanding its core tenets is essential for strategic planning.

- Focus on High-Quality Capital: The new rules placed unprecedented emphasis on Common Equity Tier 1 (CET1) capital as the most reliable form of loss absorption. This compelled banks to strengthen their core equity base rather than relying on complex, less-dependable instruments.

- The Introduction of Buffers: Basel III introduced mandatory capital cushions. The most significant is the Capital Conservation Buffer (CCB), which requires banks to hold an additional 2.5% of CET1 above the minimum. Breaching this buffer triggers automatic restrictions on capital distributions, such as dividends and share buybacks, creating a powerful incentive to maintain a healthy surplus.

The core message of Basel III is unequivocal: regulators will prioritize systemic resilience over short-term profitability. For executives, this means a capital strategy must not only meet today's minimums but also anticipate the more stringent standards of tomorrow.

Anticipating regulatory trends is a key component of strategic management. Understanding the evolution of capital requirements enables your bank to adapt to future shifts without disrupting its strategic trajectory.

For a complete look at current regulations, check out our guide on the capital requirements for banks in the US. At Visbanking, we provide the peer data and analytics necessary to assess your capital position, ensuring you are not just compliant, but strategically prepared for what's next.

Using Capital Ratios for Strategic Advantage

Meeting minimum regulatory capital requirements is merely the price of entry. Market-leading banks leverage a strong capital position not for compliance, but as a strategic tool to drive growth and outperform competitors. A healthy capital surplus is a direct measure of your bank’s capacity to expand, compete, and generate superior shareholder returns.

Turning this capital strength into a competitive weapon is what separates proactive leaders from reactive managers. Every major strategic decision—from a product launch to a competitor buyout—is ultimately a capital allocation decision.

From Defensive Buffer to Offensive Tool

A bank’s capital position dictates its strategic options. A surplus well above regulatory floors and peer averages represents dry powder, ready for deployment.

Consider two regional banks evaluating the same acquisition target.

Bank A operates with a CET1 ratio of 13%, comfortably above its internal target of 9.5% and the peer average of 11.5%. Its board can confidently approve a $50 million acquisition, knowing the additional risk-weighted assets are easily absorbed. They act swiftly, entering a high-growth market ahead of the competition.

Bank B has a CET1 ratio of 10.5%, just above its internal minimum. The same acquisition would push its ratio into the capital buffer zone, inviting regulatory scrutiny and limiting its ability to withstand future economic stress. Leadership must pass on the opportunity to preserve capital.

This is the reality of capital strategy. The institution with the stronger balance sheet has more options and can execute with greater speed and confidence.

Capital Allocation and Shareholder Returns

Beyond M&A, capital ratios directly influence shareholder returns. Decisions regarding dividends and share buybacks reflect the board's confidence in the bank's capital strength. A robust capital surplus enables a consistent and attractive capital return policy, which in turn builds investor confidence and supports the stock price.

Conversely, a bank with a thin capital buffer may be forced to curtail buybacks or limit dividend growth, signaling weakness to the market.

A strong capital ratio is the prerequisite for a credible capital return strategy, providing the flexibility to reward shareholders while funding strategic investments.

Balancing these priorities is paramount. An overly conservative capital position leads to inefficient deployment and forgone returns. An overly aggressive stance jeopardizes the institution's stability. The objective is to find the optimal balance that supports both growth and resilience.

This table outlines how a bank's capital standing directly shapes its strategic optionality.

Strategic Actions Based on Capital Position

| Capital Position | Potential Strategic Actions | Key Considerations |

|---|---|---|

| Well-Capitalized (Significantly Above Peers) | Pursue strategic acquisitions, increase dividend payouts, initiate or expand share buyback programs, invest heavily in new technology or business lines. | Ensure investments generate returns that exceed the cost of capital. Avoid complacency and maintain discipline in capital deployment. |

| Adequately Capitalized (In Line with Peers) | Focus on organic growth, execute targeted, smaller-scale acquisitions, maintain stable dividend policy, use buybacks opportunistically. | Balance growth initiatives with capital preservation. Monitor peer capital levels closely to avoid falling behind. |

| Minimally Capitalized (Near Regulatory Buffers) | Halt M&A activity, pause or reduce share buybacks, restrict dividend growth, focus on RWA optimization and capital conservation. | Prioritize de-risking the balance sheet and rebuilding capital buffers. Communicate a clear capital restoration plan to regulators and investors. |

Your capital position defines your freedom to operate.

The Power of Data Intelligence

Making these high-stakes capital allocation decisions requires more than internal reporting. It demands an objective, data-driven view of your position relative to your direct competitors. This is where data intelligence provides a decisive advantage.

Platforms like Visbanking move you beyond a static compliance mindset. By providing dynamic, granular benchmarking of capital ratios against a curated peer group, we reveal your precise competitive standing. Are you leading the pack in capital efficiency, or are you falling behind? Answering this question is the first step in transforming capital management from a defensive necessity into your most potent competitive weapon.

Mastering Risk-Weighted Assets to Boost Efficiency

Bank executives are intimately familiar with the numerator of the capital ratio—Tier 1 capital. However, strategic advantage often lies in optimizing the denominator: Risk-Weighted Assets (RWA).

Mastering RWA management is the key to enhancing capital efficiency without raising additional equity. RWA is not a simple measure of total assets; it is a sophisticated calculation that reflects the risk profile of your balance sheet. Each asset is assigned a risk weight based on its perceived credit risk—a U.S. Treasury security carries a different weight than an unsecured commercial loan.

How Your Asset Mix Defines Your Capital Ratio

Consider two banks with identical capital and assets. Both Bank Alpha and Bank Bravo hold $200 million in Tier 1 capital and $2 billion in total assets. Their capital ratios, however, tell vastly different stories.

Bank Alpha has a conservative asset mix: $1 billion in residential mortgages (50% risk weight) and $1 billion in U.S. government securities (0% risk weight). Its RWA is $500 million ($1B * 0.50 + $1B * 0.0). This results in a Tier 1 capital ratio of 40% ($200M / $500M).

Bank Bravo pursues higher yields with a portfolio of $2 billion in corporate loans (100% risk weight). Its RWA is $2 billion ($2B * 1.0), yielding a Tier 1 capital ratio of 10% ($200M / $2B).

The executive takeaway is clear: balance sheet composition directly drives capital adequacy. Every lending and investment decision has a direct impact on your regulatory capital position and strategic flexibility. Enhancing risk management practices—for example, by using advanced analytics to model asset performance—directly improves asset quality and, by extension, your RWA. The use of sophisticated fraud detection methods, such as seeing how Robinhood prevents fraud using graph algorithms, illustrates the level of analytical rigor that can be applied to protect asset quality.

RWA Density as a Performance Metric

A key performance indicator for this analysis is RWA density, calculated as RWA divided by total assets. This metric provides a powerful, comparable snapshot of a balance sheet's risk profile.

Bank Alpha’s RWA density is 25% ($500M / $2B). Bank Bravo’s is 100% ($2B / $2B).

A lower RWA density signals a more capital-efficient balance sheet. It indicates that the bank is generating returns from a less risky asset base, which supports a more sustainable and resilient business model.

It's important to note that risk-weighting methodologies vary globally. An analysis of G7 countries from 2009 to 2021 revealed that while all banks increased their Tier 1 capital ratios, U.S. banks demonstrated particularly strong growth in absolute capital relative to total assets. The Tier 1 capital to total assets ratio for U.S. banks recently hovered near 8.5%, significantly ahead of other G7 nations, underscoring how RWA frameworks can influence reported capital strength.

This global context highlights the importance of mastering the specific regulatory framework in which you operate.

From Analysis to Action with Peer Data

Calculating your bank's RWA density is the first step. The strategic value is unlocked by benchmarking this metric against a curated peer group. Data intelligence platforms provide a decisive edge here. By comparing your RWA density to that of your direct competitors, you can immediately identify strategic opportunities.

A significantly higher RWA density may signal over-concentration in high-risk assets or an opportunity to rebalance the portfolio. Conversely, a much lower density might suggest excessive conservatism and missed opportunities for profitable, well-structured lending. This granular insight enables you to fine-tune your asset mix with precision, optimizing bank capital ratios and enhancing strategic capacity. The objective is not merely compliance, but the construction of a smarter, more efficient balance sheet.

Turning Capital Intelligence into Decisive Action

Bank capital ratios are not a passive regulatory measure; they are a direct reflection of your institution's operational discipline and strategic efficiency. For C-suite leaders and board members, fluency in this language is non-negotiable. It is the clearest signal of your bank's capacity to withstand adversity, fund growth, and maintain market confidence.

In a competitive market, what distinguishes leaders from laggards is the ability to analyze, benchmark, and act on capital intelligence. Stale, retrospective reports are insufficient. Winning requires a forward-looking approach that identifies challenges and seizes opportunities before they become obvious. Awaiting regulatory guidance on capital strategy is a losing proposition.

From Reactive Compliance to Proactive Strategy

The mandate is clear: transition capital management from a compliance function to a source of competitive advantage. This requires dynamic data tools that provide the granular detail and peer benchmarks needed for confident decision-making.

The objective is to wield your capital position as a strategic weapon—to fund an acquisition your competitors cannot, to confidently return capital to shareholders, or to invest in technology that will define the future of banking.

This strategic reorientation is critical. For a review of the foundational rules, our ultimate survival guide to bank capital requirements provides essential context.

Market leadership is built on superior intelligence. At Visbanking, we provide the tools to benchmark your performance and translate complex capital data into your next decisive move. It’s time to see where you stand and begin building your strategic edge.

Capital Ratios: Your Questions, Answered

For executives managing the day-to-day realities of a bank, practical answers are more valuable than textbook theory. Here are responses to common questions from bank leaders and board members regarding capital ratios.

What's the Real Difference Between the Leverage Ratio and a Risk-Based Ratio?

The primary distinction lies in the denominator of the calculation. A risk-based ratio, such as the CET1 ratio, divides capital by risk-weighted assets (RWA). This provides a nuanced view of risk, assigning lower weights to safer assets like government bonds and higher weights to riskier assets like unsecured commercial loans.

The leverage ratio is a non-risk-based measure. It divides Tier 1 capital by the bank's total average assets, without any risk-weighting. It serves as a simple, transparent backstop to prevent excessive leverage, regardless of the perceived risk of the underlying assets.

For leadership, both are critical. Risk-based ratios measure resilience to specific credit and market risks, while the leverage ratio acts as a fundamental guardrail against excessive balance sheet growth.

How Do Stress Tests Actually Impact Our Capital Planning?

Regulatory stress tests, such as the Federal Reserve's DFAST and CCAR, are not simply compliance exercises; they are a direct input into your forward-looking capital plan. These tests simulate the impact of a severe economic downturn on your bank's capital levels.

The results determine your bank's specific Stress Capital Buffer (SCB)—the additional capital you must hold above regulatory minimums to account for your unique risk profile under stress. A poor stress test result can immediately restrict your ability to execute capital actions, such as dividends and share buybacks. Therefore, stress test preparedness must be integrated into year-round capital management to ensure resilience against future shocks, not just to pass an annual exam.

Why Should We Hold Capital Way Above the Minimums?

Maintaining a capital surplus well above the regulatory floor is a strategic imperative, not just a conservative posture. This surplus provides significant advantages:

- A Bigger Cushion: It allows the bank to absorb unexpected losses without approaching regulatory thresholds that trigger restrictions and intensive supervisory oversight.

- Market Bragging Rights: A superior capital position signals strength to depositors, investors, and rating agencies, which can lower the bank's cost of funding.

- Dry Powder for Offense: This is the most critical advantage. Excess capital is the fuel for strategic action—acquiring a competitor, investing in transformative technology, or expanding market share when others are retrenching.

When you have a strong capital buffer, capital stops being a defensive regulatory burden and becomes an offensive strategic weapon. It’s what lets you play offense when everyone else is stuck on defense.

Understanding how your capital ratios compare to your peers is the first step toward strategic action. At Visbanking, we help you transform these complex metrics into clear, actionable intelligence. Check out our platform to see where you stand and identify your next strategic opportunity.

Latest Articles

Brian's Banking Blog

Customer Churn Prediction: A Practical Guide for Banks

Brian's Banking Blog

Social Network Analysis for Banking: A Practical Guide

Brian's Banking Blog

How to Increase ROE: A Data-Driven Playbook for Bank Leaders

Brian's Banking Blog

What Is SEC EDGAR and How Banks Use the Data

Brian's Banking Blog

What Is Value at Risk and Why Bank Leaders Rely on It

Brian's Banking Blog